Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

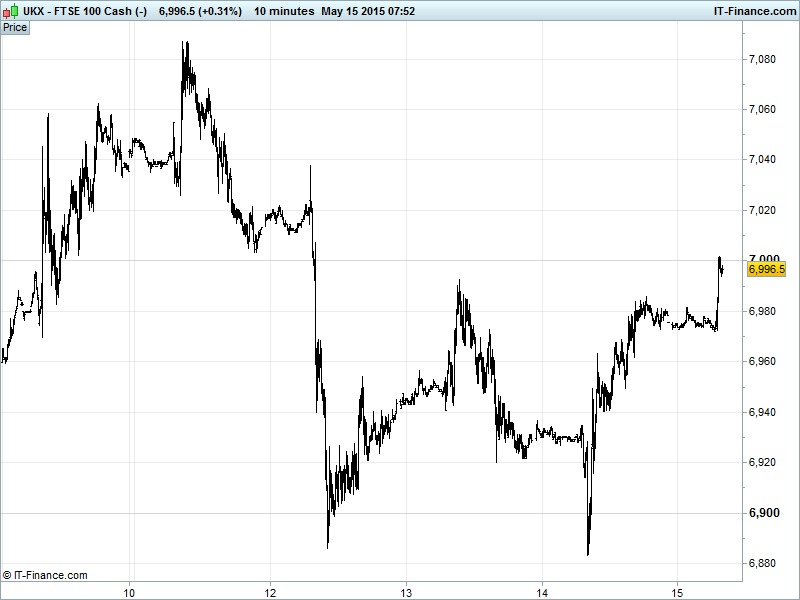

UK 100 Index called to open +20pts at 6995, having recovered from yet another test below 6900 to revisit 7000 as we write. The index continues to hold above its 100-day moving average (6915) with Bulls remaining optimistic of a revisit of 7127 highs while the bears refuse to ignore falling highs from mid-April hoping for another drop back towards 6900, or lower. Watch levels: Bullish 7010, Bearish 6950.

The positive opening call comes after the UK 100 gained 3.4% in Thursday trading as US Fed member commentary appeared to take a June interest rate rise off the cards. In Europe, Mario Draghi indicated yesterday that the Eurozone’s QE programme would continue until the 2% inflation target is reached and deemed sustainable. The comments buoyed both bonds and equities in the Euro Area and contributed to rebounds and record closes in the US overnight.

US stocks staged a recovery yesterday afternoon leading to the good performances mentioned above, with the Dow Jones index popping back up to trade above 18200 and the S&P500 hitting fresh all-time highs on a weak but supported dollar – weak on disappointing recent macro prints but supported now by Draghi’s comments - amid shrinking prospects of an imminent US interest rate hike.

Asian stock indices largely positive overnight, echoing stateside gains driven by calmer bond markets, weak US data further cooling US rate rise expectations and ECB President Draghi’s dovish ‘QE for as long as necessary’ speech appeasing global monetary stimulus addicts. Japan’s Nikkei benefiting from a weaker JPY, poor PPI data supporting continued BoJ stimulus and share buy-back plans by major corporates.

In Focus today we have the UK’s construction output with forecasts for a big improvement – if you live or work in London you may well agree with consensus on this one. This afternoon sees US Empire Manufacturing, Industrial Production and University of Michigan Consumer Confidence looking to buck a generally weak trend in recent prints. The Baker Hughes Rig Count rounds off the week data-wise.

China stocks the red, giving up some of the week’s rate-cut inspired gains, despite data showing a rebound in Foreign Direct Investment, with liquidity concerns revived ahead of a raft of IPOs next week and a jump in fiscal spending showing the extent to which Beijing is obliged to bolster the slowing economy.

Brent ($66) and US Light Crude ($59) continuing to pull back from 6 May highs and beginning to really test those 2015 uptrends as both OPEC and US shale producers look to expand production this year while falling rig counts and a fall in US stockpiles (still near their highest levels since 1930 though) appear to be doing little to raise prices amid a continuing global supply glut.

Gold holding above $1215 following yesterday’s breakout on weaker US data denting the USD by throwing back US rate rise timing while Draghi’s speech revived optimism and inflation hopes. Nonetheless, improved highs of $1127 were unable to deliver much headway on prior 3-month highs of $1224. Speculation that European uncertainty and Greek default fears are inspiring Germans to increase safehaven buying. Support $1212, Resistance $1227.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Foreign Direct Investment Beat, jumped

- Japan Producer Price Inflation In-line, deteriorated

- Japan Consumer Confidence Miss, deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Tyman sees UK market to return to growth in second half of year

- Tyman says year to date operating profit ahead of 2014

- Hornby names new finance director

- Saga appoints Jonathan Hill as CFO

- HSS Hire sales and marketing director resigns from board

- William Sinclair says Finance Director Peter Williams has stepped down

- John Menzies says Jan – April trading in line with plan

- EnQuest reiterates FY15 production guidance

- SAB looks to fast – growing craft beer with Meantime acquisition

- SABMiller to enter UK craft beer market with Meantime acquisition

- Intertek Group reaffirms full year revenue expectations