Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

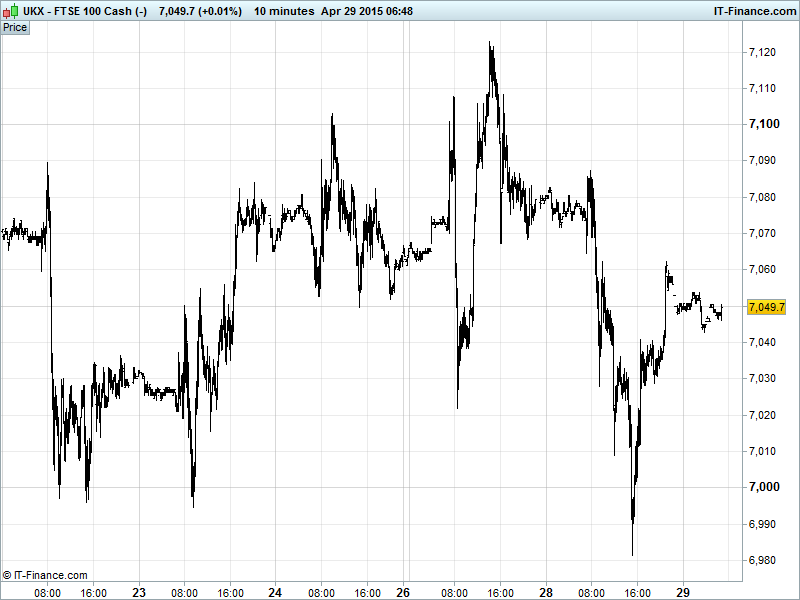

UK 100 called to open +20pts at 7039 after recovering from another sharp selloff yesterday afternoon as global markets reacted to the storming of a merchant vessel in the Persian Gulf by Iranian forces and the speculation that followed. Support holding around 6980 as the index continues to trade sideways, mostly between 7000 and 7100 but with two breakout attempts either side since 16 April. Updated watch levels: Bullish 7150, Bearish 6950

The positive open comes as a result of the aforementioned recovery with drivers (or a lack thereof) closer to home taking the form of market anticipation of today’s US GDP data and the FOMC minutes due out this evening, both of which investors will be watching closely for some form of comfort after the UK’s own GDP disappointed yesterday.

US bourses closed positive on Tuesday with the FOMC meeting very much a feature of expectation on the other side of the pond. The US economy is still in recovery mode with recent data and lacklustre inflation leading most to expect that the Fed will do the right thing and delay a rate hike until September at the earliest. Economists are citing too much uncertainty in the current climate to warrant specific clarity from the minutes this evening, indicating that the Fed will want to leave themselves as much maneuvering room as possible until a clear way forward presents itself.

Asian equities retreated Wednesday as investors there braced themselves for weak US economic growth following a string of disappointing macro data from the world’s #1 economy. The negative performance came amid conflicting reports about the PBoC apparently readying itself for its most aggressive round of economic easing since 2008.

The big underperformer in the region was Australia’s ASX index which shed 1.5% after Goldman Sachs saw its credit rating, currently AAA, at risk of a downgrade. The commodity price doldrums, weak economic growth and political stalemate surrounding the passing of legislation have all weighed on the nation’s finances of late leading S&P to place its rating on negative outlook.

In focus today we have the much awaited US GDP data followed this evening by the FOMC meeting minutes, both of which have been keeping markets subdued this week. Expectations are that US interest rates will be kept as is at near-zero following a deterioration in GDP.

US Light crude ($57) and Brent ($64) both crawling up rising support, essentially sideways but with the potential for a bounce back up through resistance (around $66 for Brent and $59 for WTI) and onwards into their respective rising channels. Investors have again been waiting for macro data and the Fed. US stockpiles continue to rise with confirmation of this expected later today as the EIA reports its weekly oil stocks numbers.

Gold ($1209) received a boost yesterday as the US Dollar basket weakened considerably having experienced a sharp pullback from 23 April, breaching 2-month support on Tuesday this week. The dollar basket found new support not far below, however, and Gold is off yesterday’s high $1215 this morning.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Consumer Sentiment Deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Devro says outlook for 2015 remains unchanged

- Weir Group sees continued fall in orders from oil and gas business

- Weir Group Q1 order input down 9%

- Alent says Q1 in line with expectations, 2015 outlook unchanged

- Copper miner Antofagasta cuts annual production forecast

- Standard Life assets under administration up 5% to £312bn

- Barclays takes another $1.2bn hit to cover past problems

- Russia's Petropavlovsk 2014 net loss narrows to $348mn

- UK house price growth hits 10-month high in April –Nationwide

- Smiths Group says closes €600mn bond offering

- LSE Q1 revenue boosted by Russell Investment Management deal

- Miner ARMS posts FY operating profit of $28mn

- Countrywide posts fall in Q1 income on UK election uncertainty

- Next Q1 full price sales up 3.2%

- TSB Banking Group Q1 pretax profit jumps 153.3% from Q4

- British lender TSB's Q1 current accounts top target

- Greggs announces special dividend, strong sales

- Thorntons says remains cautious about outlook for full year

- Spirit Pub pretax profit rises to £25mn 28 weeks to March 7

- Home Retail profits rise, cautious on first half outlook