Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

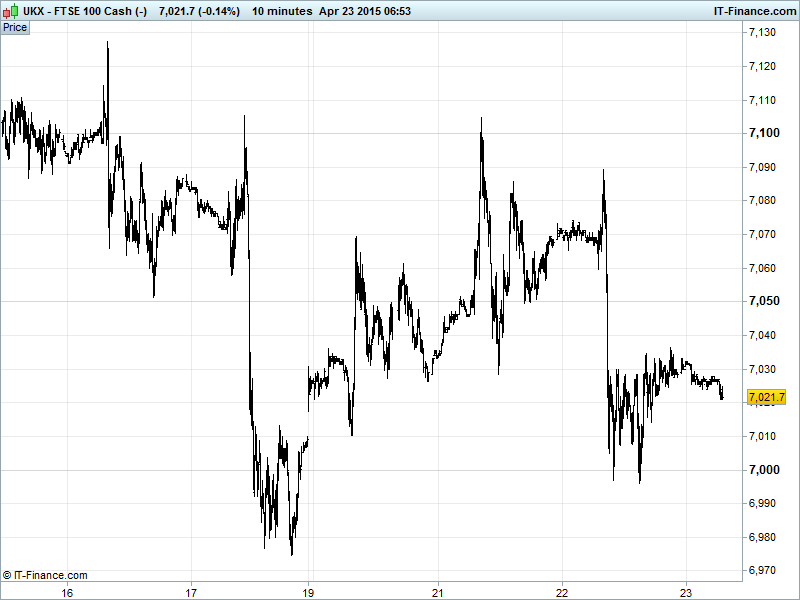

UK 100 called to open flat at 7022, range bound within a shallow rising channel after pulling back on Wednesday but quickly recovering to close back above 7000 with solid support holding just below. A break out of resistance at falling highs would please bulls still looking to 7200 and beyond, while bears looking for a pullback to rising support just below 6900.

The positive, yet lackluster open comes as the newswires appear to be filling space with Greece in the absence of much else in the way of meaningful economic drivers for the UK benchmark index.

A conference call with Eurozone officials on Wednesday concluded that much more work needs to be done before a deal can be reached with the country’s creditors (yawn) while Greece’s representative in its Paris based talks, Nikos Theoharakis said that an agreement must be made on a “political level”, whatever that means. Tsipras meets with Merkel today in Brussels where the expected outcome is the German Chancellor reiterating the importance of a deal being reached on a ‘technical level.’

US markets closed positive Wednesday as the NASDAQ continues to besiege all time record highs after a string of good US company earnings reports.

Asian bourses are also in the green, apart from the Aussie ASX which is down 0.1%. Weak Chinese manufacturing data (12-month low) took the Shanghai composite lower, but it later rebounded. Meanwhile, Japanese stocks rose for a third consecutive day led by brokerages and energy shares as a weaker Yen boosted exports.

Data wise, we kick off with the Swiss trade balance, followed by Services, Manufacturing and composite PMI for France, Germany and the Eurozone. Later in the morning will be UK public finances and retail sales. Speakers include the ECB’s Praet, the EU’s Moscovici and The German Chancellor Merkel, discussing all things Europe.

Oil prices continue to travel North in a volatile uptrend, just off April highs this morning and seemingly supported by a 1-month rising trend line. Impatient Genel Oil (and former BP) chief Tony Hayward yesterday tried to help prices on their way by saying he expected $80 crude to arrive imminently. Nice try, Tony! US light crude and Brent trading at $58 and $62 respectively this morning.

Gold ($1187) sank below $1190 overnight, just about remaining in the sideways range so much a feature of April. 7-day falling highs not improving the outlook for the metal as risk sentiment improves in the Eurozone after the ECB approved more ELA for Greek banks ahead of Friday’s Eurogroup meeting.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Manufacturing PMI Miss, deteriorated

- China Manufacturing PMI Miss, deteriorated

- Swiss Trade Balance Beat, Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Taylor Wimpey says on track towards medium term targets

- Anglo American cuts diamond output forecast on weaker market

- Acacia Mining's Q1 core profit falls due to low gold prices

- WPP says on track for FY net sales growth

- Senior reaffirms FY 2015 profit expectations

- Gemfields rakes up revenues of $16mn from Jaipur ruby auction

- Pace says Arris Group offer "great fit for both

- Meggitt says on track to meet 2015 revenue guidance

- Cobham on track for to meet FY organic revenue growth target

- Computacenter Q1 revenue falls 2