Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

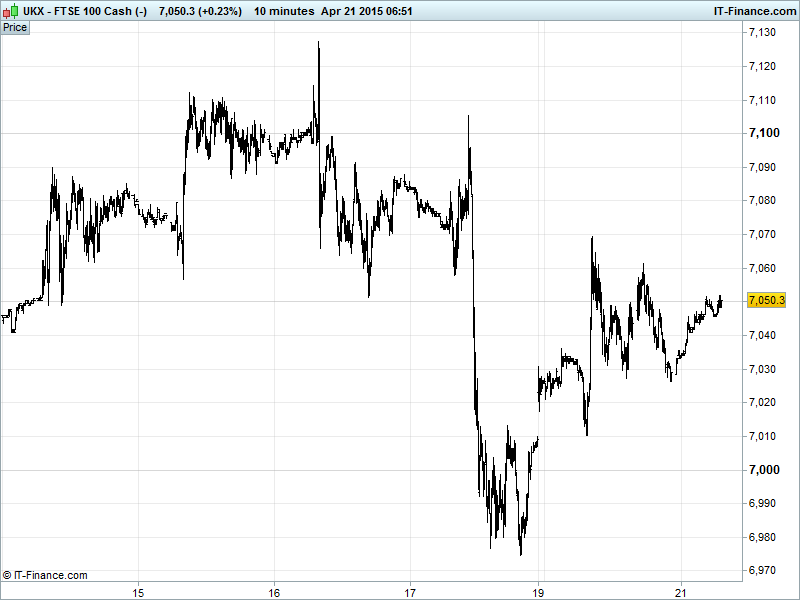

UK 100 called to open +10pts at 7064 after stabilising yesterday as global markets recovered with positive news from China taking the sting out of Greek uncertainty. The index currently moving into the apex of a rising pennant pattern - typical of a bear market rally - indicating potential for a sharp breakout in the coming week. Updated watch levels: Bullish 7200, Bearish 6900.

The warmish open comes as neither good nor bad news has managed to sway sentiment overnight and into this morning. Greece continues to weigh on investors’ minds with unease surrounding Russia’s role in the situation. Could Putin afford to extend his hand to the troubled nation? Some think not, which is seen as a good thing while others are genuinely worried that he can and will. According to reports, The Kremlin is willing to offer up to €4.5B to Athens as an advance for a planned natural gas pipeline through the country.

The Euro Area finance ministers are due to talk on 22 April to try to lay out a road map to a May agreement on how to take cash strapped Greece forward before the cash runs out completely, which will involve……….the submission by the Greek government of a list of reforms!

US markets performed best in Monday trading, posting the most impressive recoveries with Wall St. surging back into the upper half of its 1-month sideways trading channel and a 3- week uptrend. The NASDAQ and S&P500 duly followed suit. The US Dollar staged a comeback against the Yen with currency traders selling off the Japanese safe haven to take advantage of the rally in equities. Upside was capped around Y119.5.

In Fed news, New York Fed Boss Dudley is committed to ‘caring for the world’ with policy normalisation, indicating that hard and swift action would cause considerable problems for those holding large dollar denominated debt outside the US. The comments came in response to the IMF which warned of said problems last week.

Worries of another ‘taper tantrum’ have evolved into worries of a ‘super taper tantrum’ with research by Deutsche suggesting 5 separate episodes since 1994 when 10-year US Treasury yields spiked in anticipation of Fed policy changes.

Asian stocks followed Wall St higher yesterday with the Nikkei and ASX closing in posituive territory. The AUD/USD continued to pull back with the RBA minutes presenting the case for further monetary easing after the responsiveness of borrowers / savers to changes in interest rates had been highly uncertain in the current climate of already-low rates and high house prices – meaning greater leverage available to those owning homes. The minutes also alluded to the benefits of having an even weaker AUD, namely assisting in the achievement of more balanced growth. Non-mining investment is still subdued in Australia, which is trying to move away from its economic dependency on raw materials amid commodity price doldrums.

Oil prices are flat this morning but remain in a 1-month uptrend with both benchmarks trading around a positive trend line. Cautious investors are beginning to see opportunities in commodities, whose prices have been low for some time, as the global economy appears to be on the mend. US Light Crude currently at $59 while Brent trading around $63.

Gold ($1195) trading sideways, still spending equal amounts of time above and below $1200 which is somewhat of a magnet for the price of late with the potential for consolidation into a shallow rising channel with support at April rising lows.

In focus today we have Eurozone Zew Surveys and the weekly API Oil data from the US.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Informa says Q1 organic revenue falls 0.5%

- APR Energy sees FY net income "at or slightly below" market expectations

- Carpetright sees FY pretax profit ahead of market expectations

- Sky posts 20% jump in profit on broad demand

- IQE says got long term purchase orders worth up to $3mn in Q1

- Chip designer ARM on track for year after encouraging Q1

- AB Foods profit falls on sugar weakness

- Tate & Lyle alters European joint venture, Splenda business