Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

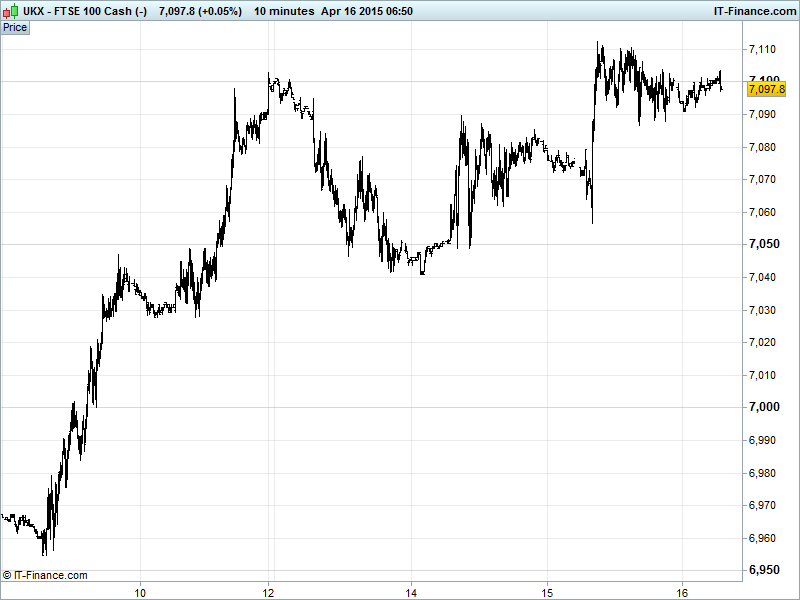

UK 100 called to open-10pts at 7065, continuing to bed in above 7000 but failing to make meaningful further progress amid the ongoing Greek bailout talks. Updated watch levels: Bullish 7130, bearish 6950.

The lackluster open comes as the Eurogroup is due to meet on April 24 to talk about further aid in return for Greek economic reforms, but members such as German Finance Minister Schaeuble remain skeptical the meeting can yield results despite Greek PM Tsipras remaining ‘firmly optimistic’ about the whole thing. But what else can he do?

US stocks lost momentum towards the end of play Thursday to close mildly negative. Fed chat roundup: Lockhart downplayed recent disappointing US economic data and suggested growth of up to 3% this year with inflation rising towards the back end of 2015. Mester suggested the benefits of an early rate hike will outweigh those of a delay and that a gradual increase is key so as to not derail the recovery.

Rosengren was dovish, saying conditions have still not been met for a rate rise and that data has yet to improve to warrant it – going against Lockhart in taking notice of a poor employment report and a significant reduction in growth on last quarter. He also pointed to inflation being ‘stubbornly’ below the 2% target. Finally, vice chair Fischer said that there are signs of a recovery but inflation is likely to take years to reach 2%, rather than months.

Doves leading the flock?

Asian markets closed mixed with the Shanghai Composite outperforming, posting gains north of 2%, a 6th straight week of positive performance, on hopes of imminent monetary easing from the People’s Government.

In focus today we have UK jobless claims and employment data, Eurozone CPI at 10:00 and US CPI around lunchtime. University of Michigan Sentiment and the Baker Hughes Rig count round off the week’s economic data.

Oil prices posted negative performance early on Friday, with both benchmarks hitting YTD highs in Thursday’s session. WTI (US Light) declined 0.90% to $56, and futures for Brent fell to $63. Crude continues in an intraday uptrend with key support levels currently $54 for WTI and $62 for Brent. Conflict in Yemen, including the involvement of Al Qaeda, and burgeoning OPEC supplies are pushing and pulling the oil price this week .

Gold ($1200) is still trading around....$1200, as it has been all week, and failing to remain either above or below for any great length of time. Inflation is a key driver for the gold price at the moment, with expectations of higher inflation bolstering demand for the non-interest bearing asset. However, disappointing data from the US has stifled hopes of its 2% inflation target being reached any time soon, keeping demand low for the yellow metal which won’t appreciate much in value without that all important inflation.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Consumer Confidence Index Beat, Improved

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Acal announces intended appointment of Nick Salmon as non – executive chairman

- TSB says Sabadell takeover docs posted, offer closes May 8

- Astrazeneca gets orphan drug status for uveal melanoma treatment

- Sirius Minerals says SBC recommends approval of York Potash planning application

- Serco announces 94.7% take up of rights issue shares

- Optimal Payments to admit 272,495,506 new shares on AIM

- Alliance Trust urges investors to back its strategy at AGM