Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

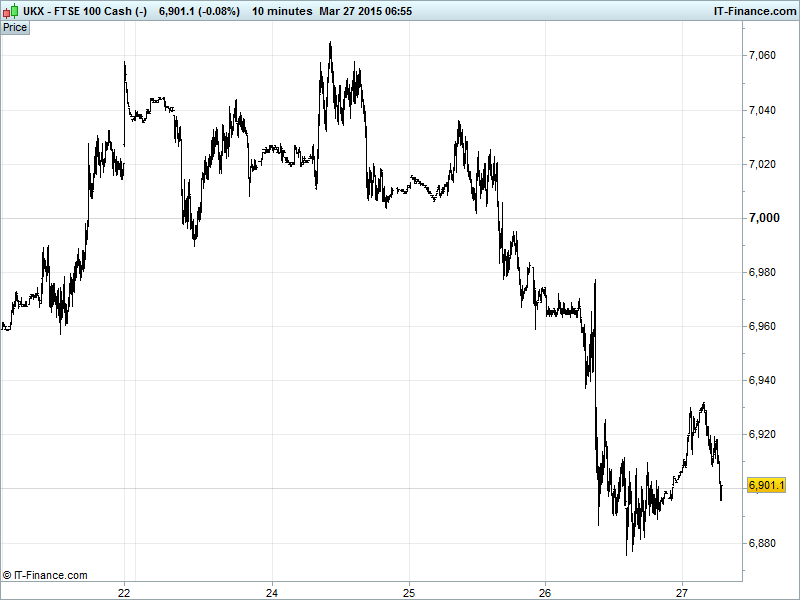

UK 100 called to open flat at 6895, back down below the key 6900 support level around which we traded so much yesterday despite an overnight recovery of sorts which took the index back as high as 6932. Potential now for yesterday’s lows of 6880 to be tested and, after the pause, recent declines to see a second wind down towards mid-month lows of 6700. Watch levels: Bullish 6940, Bearish 6870.

The flat opening call comes after further weak sessions in the US and Asia, although the former did manage a recovery from an earlier move to the downside, as caution prevails in light of geopolitical uncertainty linked to intervention in Yemen, digestion of mixed macro data from both the US (ahead of GDP today) and Japan (inflation + retail trade overnight) as well as unrelenting Fed chatter (Lockhart, Evans).

Beware adoption of week-end risk-off as we approach Monday’s deadline for Greece to present economic reforms needed to unlock funding and avoid further deterioration of already its dire straits as depositors continue to withdraw funds from Hellenic banks. Note recent weakness seeing the S&P500 join the Dow Jones in trading negative for 2015.

US stocks closed off yesterday’s lows. However, both the Dow Jones Industrial Average and S&P500 are now in the negative for the year to date (DJ -0.8%, S&P -0.1%). Stocks have fallen every day this week as investors grappled with disappointing US economic data and concerns about overvaluation in tech and other important sectors in the American markets. Oil prices made their biggest gains after Saudi intervention in Yemen but are trading back from those highs this morning as the dollar basket made gains. Fed news: Lockhart said that June, July and September are all good times for rate lift-off while Evans preferred to rule out a summer hike in favour of a cooler autumn.

Asian Bourses mixed it up overnight with wary investors creeping about amongst geopolitical worries and mixed Japanese economic data indicating a drift back towards deflation for the Japanese economy after 2 years of Shinzo Abe’s super-QE. Nonetheless, BoJ Governor Kuroda continues to exude confidence in a recovery whose timetable is changing somewhat. The Nikkei rose overnight as investors, though nervous, went on the bargain hunt after yesterday’s tech rout. Panasonic was the star of the show with shares rising 4% after the company announced it would spend up to 1 trillion yen on M&A over the next 4 years.

China’s Shanghai Composite Index is hovering near its seven-year closing high of 3,691, hit on Tuesday when the index completed 10 straight sessions of gains. Investors are racing to get involved in the ever burgeoning Chinese markets, which many fear is leading towards a bubble. The Shanghai Composite is up 13% YTD making it the best performing Asian market thus far in 2015, though some way off it’s 53% 2014 gains.

In focus today we have US GDP with mixed forecasts. University of Michigan Sentiment looking for an increase, and the Baker Hughes Rig Count.

US Light crude ($50.6) and Brent ($58.3) may be back from yesterday’s highs as the USD found some support and regained a 97 handle and some quick profit taking kicked in, however, both benchmarks appear to have found support around $50 and $58 respectively, helped by geopolitical uncertainty in the Middle East (Yemen, Iran) and potential impact on supply levels and despite recent US stockpile gains.

Gold ($1205) is holding around the same levels of yesterday with support kicking in at round number $1200 overnight as the USD rallied back thanks to uncertainty from both a geopolitical (Middle-East) and growth standpoint (US GDP this afternoon). Gold’s reversal and rally from $1142 Dec lows continues with a pause after the test of the of $1223 early March highs as investors shied away from riskier assets. Pause before resumption, or is that it?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Industrial Profits Less weak

- Germany Imports Price Index Beat, improved

- UK Nationwide House Prices Miss, growth slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Homeserve says overall group trading in line with expectations

- Kromek Group says chairman to step down

- Judges Scientific FY rev £40.6m

- IP Group says to raise £128m from placing

- Vodafone in Botswana partner agreement

- Corac signs ten-year commercial agreement with UK's Spirax-Sarco

- Antofagasta suspends operations at three Chilean mines due to rains

- Housebuilder Barratt names FD David Thomas as new CEO

- Trinidad regulator approves Cable & Wireless' Columbus purchase

- Redrow says sells some London rent portfolios for £10.2m