Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

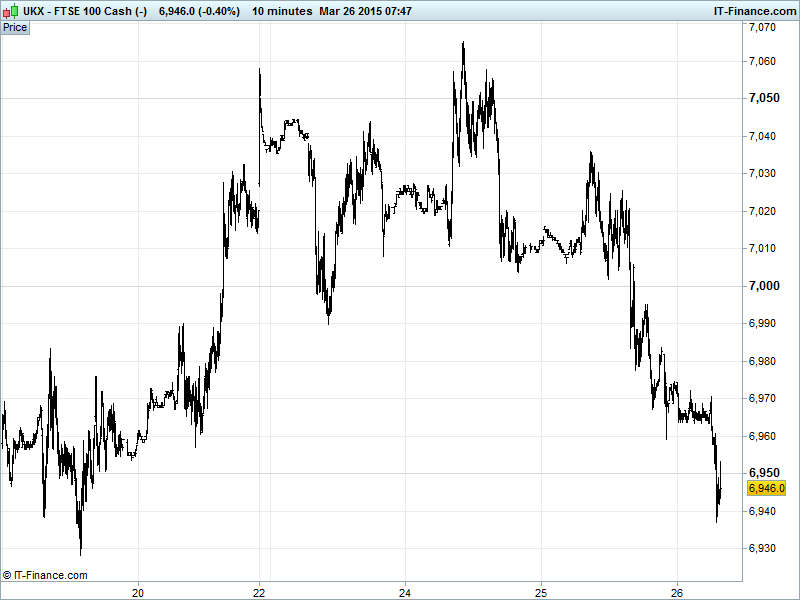

UK 100 called to open -40pts at 6950, still struggling for support after yesterday’s sharp sell-off late in the day saw the index retrace further from all-time highs. With 7000 and 6990 being left behind, we now look to support at 19 Mar lows 6930 unless declines are set to deliver a 5% correction all the way back to the recent rally platform of 6700. Watch levels: Bullish 7005, Bearish 6920.

The negative opening call comes after steep declines for US equities (led by Tech) and a weak Asian session following poor US Durable Goods Orders which added to recent soft US data and jitters about US recovery ahead of Friday’s GDP print and helped USD pull back further on reduced fears of an imminent US rate hike. Heightened geopolitical risk also played its part with an escalation of violence in and airstrikes on Yemen (and the weaker USD) helping send Oil to 2-week highs. Note the Dow Jones Index now negative for 2015 (-0.6%).

With central bank chatter still plentiful, note the Fed’s Lockhart hawkishly saying ready to vote for a September rate hike while Evans countered with a more dovish “no rush” and that he favours a 2016 lift-off. Closer to home, hawkishness dominated with Miles saying the BoE’s next move was likely a hike rather than a cut despite recent data suggesting close to deflation while Forbes said unlikely BoE forced to ease further.

US stocks continued their rout on Wednesday to close sharply lower with tech stocks weighing most heavily on the Dow Jones after durable goods orders missed consensus by some way. A nigh on 10% increase in mortgage applications failed to buck what was a disappointing trend in economic data while the Fed stalemate added little to either side of the debate. Saudi air strikes on Yemeni rebels pushed up the oil price while adding to global uncertainty as a proxy war with Iran sets in around a strategically essential location in the global energy trade. In the UK, BoE dove Miles turned hawkish suggesting a rate rise as more likely than a cut while optimism abounded in the Eurozone where the Greek Central Bank Governor expressed confidence in reaching a deal with creditors.

Asian Bourses again following Wall Street on a southerly migration on worries surrounding US-supported Saudi actions in Yemen where, it is reported, the Yemeni president has fled the country. Japanese stocks are heading for their biggest sell off since mid-Jan, leading peers lower after way off the mark macro data from the US and a stronger Yen hitting exporters. The US tech stock sell off also hit the industry in Japan. A gauge of the tech stocks in the Nikkei was down over 2% according to FactSet – with contributions from the likes of Tokyo Electron (-5%) and TDK Corp. (-2%).

Chinese markets did their own thing as they often do, rising 2% on Thursday as the PBoC reiterated its commitment to keep monetary policy prudent reassure investors that China will prevent and resolve financial risks. Citi cut its 2015 forecast for Australia’s GDP growth to 2.4% and CPI to 1.9%. Citi also expected the RBA to cut rates in May and August by 25bps each.

In focus on a busy Thursday we have French GDP, UK retail sales which will be interesting to watch given zero inflation having been hit on Wednesday. Indeed, MoM forecasts are positive. Kansas City Fed Manufacturing rounds off the afternoon.

US Light crude ($51.1) and Brent ($58.4) have put on up to 10% from yesterday’s mid-afternoon lows and thus close to staging their biggest 5-day rally since 2009 amid a worsening situation in the Middle East as Saudi Arabia and Gulf allies start bombing Houthi targets in Yemen. This offset another bigger than expected rise in US EIA Crude stockpiles and saw both benchmarks break above recent highs. Note talks over Iran’s nuclear program hitting a stumbling block after it stalled a UN probe into whether the country has previously tried to build atomic weapons.

Gold ($1205) has managed to hit three-week highs after the downbeat US economic data weakened the USD and cheapened the yellow metal while safehaven seeking grew on the worsening geopolitical situation the Middle East. Gold’s reversal and rally from $1142 Dec lows continues and the bettering of round number $1200 opens up the possibility of a revisit of $1223 early March highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Germany GFK Consumer Confidence Beat, improved

- France GDP In-line, confirmed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Wizz Air sees FY in line with expectations

- easyJet upgrades first-half forecast on currency boost

- Amec Foster Wheeler posts FY adjusted pretax profit 317 mln stg

- Euromoney Institutional Investor says trading in line

- DFS posts 16.5 pct rise in first half earnings

- RBS says to realise $3.2 bln from Citizens share sale

- Lloyd's of London posts unchanged profit for 2014

- Daily Mail owner says trading in line, maintains outlook

- SuperGroup to start dividend payments in 2015-16 year