Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

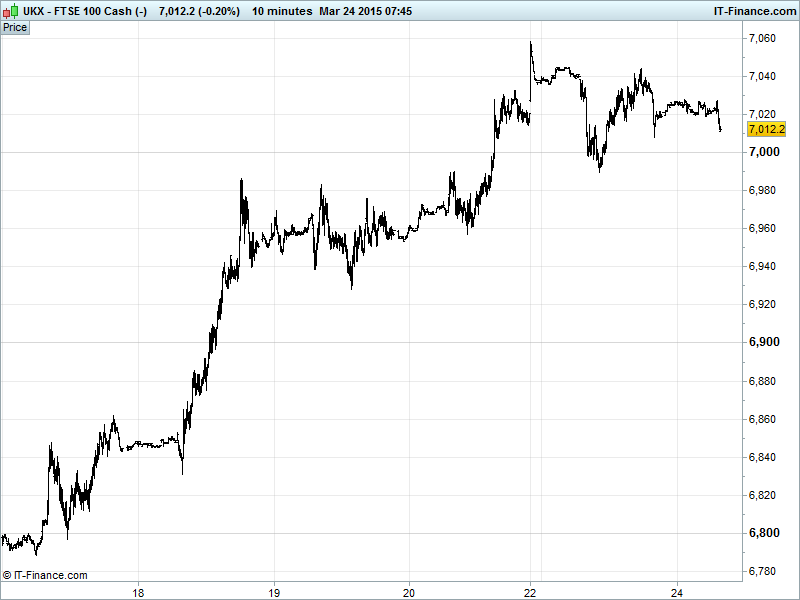

UK 100 called to open -20pts at 7015, back from yesterday’s highs of 7045 and Sunday night’s all-time high of 7058 but still holding above the key 7000 mark. Note the index testing an intersecting trendline of resistance-turned-support from last Monday at 7020 and whether Friday’s breakout (and yesterday’s lows) 6695 hold. Our watch levels are unchanged at: Bullish 7065, Bearish 6980.

The negative opening call comes courtesy of a soft US close despite a weaker USD and oil price rally as uncertainty persists about monetary policy outlook via much Fed chatter. Nothing tangible came from the Tsipras-Merkel crisis meeting and risk appetite was tempered in Asia overnight after disappointing PMI Manufacturing reads from China and Japan with HSBC’s China flash estimate missing consensus, falling to an 11-month low and into contraction highlighting its economic slowdown and need for more stimulus.

In Europe, Alexis Tsipras had no need for the begging bowl – everyone knows what he’s after by now - as he met with Angela Merkel where they talked to eachother rather than about eachother. The saga continues.

US stocks had retreated at close despite an oil price rally and the US Dollar pulling back on the dovish Fed rhetoric put out by Mester, Bullard and Fischer. Nonetheless, both doves and hawks found support overnight as US existing home sales climbed while the central bank downgraded its growth and inflation forecasts for the year.

Asian bourses are down this morning following the weak cues from Wall Street and after disappointing Chinese manufacturing data, with PMI dipping below 50, pointed towards economic slowdown in the world’s #2 economy. Meanwhile in Japan, its own PMI hit its lowest level in 10 months at 50.4. The Japanese economy is limping but hasn’t stopped moving forwards as the Nikkei continues to pull back from Monday’s 15 year highs with a range bound Yen and a general lack of confidence in the region. China’s Shanghai Composite contracted on the PMI reading. Will we see a recovery as investors start to expect some much needed economic stimulus?

In a knock-on effect, Australia’s ASX trimmed its own gains to add 0.1% as the AUD/USD pair retreated. The index was helped, however, by the resources sector which was itself bolstered by a stabilization of commodities prices overnight. Market bellwether BHP Billiton gained 0.2% while news came out of China that Beijing is due to close all of its coal fired power plants making the mining stock an interesting one to peruse this week.

In focus today will be additional PMI data for France, Germany and the Eurozone all looking to indicate improving economic health, while that for the US showing a slowdown. UK and US CPI data are expected to show UK inflation struggling to make headway and its US counterpart in a similar situation.

US Light crude ($46.8) and Brent ($55.6) both benefiting from a Fed chatter-induced weaker USD, taking the price of a barrel back up towards the highs of last week. While in an uptrend from 18 Mar (rising lows), prices off their best levels after comments over Saudi Arabia’s output (nearing all time high 10m barrels/day; above Fed daily guidance; no sign of giving up market shares), reports of a potential deal to lift Iranian sanctions and China’s factory gauge reading disappointed.

Gold ($1188) still in uptrend recovery mode, touching $1191 overnight thanks to the USD retrace from recent highs, uncertainty regarding monetary policy outlook, what becomes of the Greek cash crisis situation and of course the China factory output contraction print overnight. The break out from the Jan-Mar falling channel continues although gains have slowed overnight as highs correspond with the late Feb lows which could limit progress in the short-term. Note Silver trading 2015 highs and testing $17.00 overnight.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan PMI Manufacturing Miss, deteriorated

- China HSBC PMI Manufacturing Miss, deteriorated

- China Conf Board Lead Econ Index Growth accelerated

- Japan Small Business Confidence Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Faroe Petroleum sees 2015 production of 8,000 – 10,000 boepd

- SkyePharma full-year revenue +18%

- Game Digital says CFO to step down

- 888 sees profits jump, announces special dividend

- Gulf Marine Services FY adj net profit +13%

- IQE full-year operating profit +21%

- Wolseley sees full year in line after first-half profit rise

- Land Securities sells London office building to Blackstone

- NCC Group agrees to buy Accumuli for £55m