Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

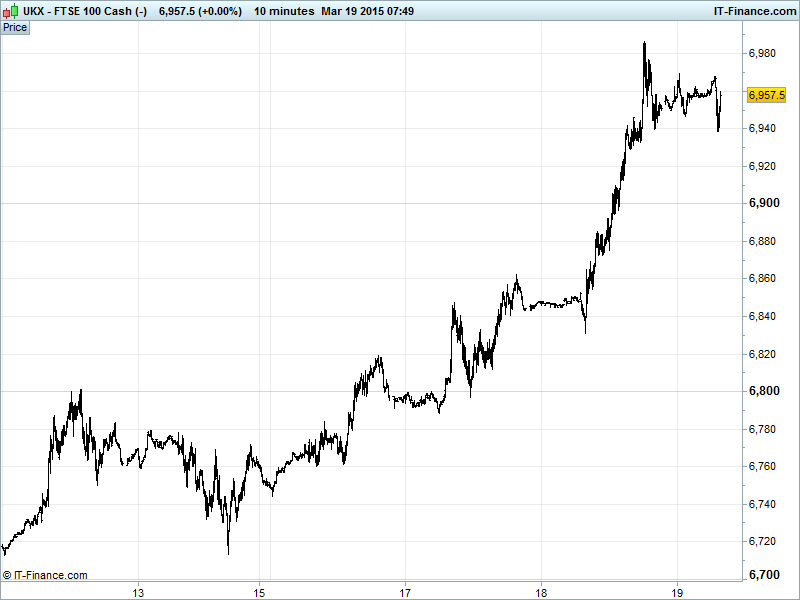

UK 100 called to open +5pts at 6950, trading back a little from a new fresh all-time high in the wake of Fed Chair Yellen’s dovish FOMC speech yesterday evening. Appetite to breach the 7000 mark remains strong although bears will be watching for any chance of another retrace of the recent 295pt bounce. Potential for support around 6950 region. Watch levels: Bullish 6975, Bearish 6925.

The UK index was up at close yesterday in contrast to other European equity markets with George Osborne offering tax breaks to energy companies as part of his populist pre-election budget as well as revising up the UK growth forecast for 2015. UK inflation still off on sliding oil prices though.

The flat opening call comes despite a positive session in Asia as investors priced in a later start and slower pace of US rate rises which hit the dollar hard from recent highs and benefited commodities-linked securities. Fed Chair Yellen’s dropping of the ‘patience’ forward guidance pledge was offset by her reassuring that the Fed would ‘not be impatient’ either due to lower growth/inflation forecasts, keeping up her record of helping markets each time she speaks.

In Europe, Alexis Tsipras heads to Brussels today to meet with a frustrated Angela Merkel, Jean-Claude Juncker, Mario Draghi and Francois Hollande to talk politics after the technical talks concerning Greece’s finances appear to have faltered. The latest talks will no doubt feature Greece’s latest bill, promising free energy and food stamps for poor families which has heightened tensions between Greece and its creditors. Tsipras continues to express his government’s commitment to honour the bailout terms set by the Eurogroup while simultaneously honouring his own pre-election commitments to the Greek people. All the while, Greek bank deposit outflows continue to rise, even spiking on the recent political statements/fears.

US stocks soared after the Fed carified yet again their position on an interest rate hike, encouraging people to concentrate on the data. To that end the effects of US dollar strength, off-target inflation and lacklustre wage rises all point towards a dovish stance on a rate liftoff for the time being. But we pretty much knew that, didn’t we? The Fed kept the emphasis that when a rise does happen, rates are likely to stay below past normal levels for "some time." Yellen emphasised that the decision won’t be based on one single criterion.

Asian bourses are positive this morning with the exception of Japan’s Nikkei which was hit by a less strong USD following the Fed announcement. Elsewhere in the region, however, markets followed Wall St’s cues and rallied, enjoying their best session in 18 months. In Australia the ASX was up, buoyed by its banks as markets expressed confidence that a domestic interest rate cut will happen.

In focus today will US Jobs Data with jobless claims set to go up a bit, and continuing claims looking for a fall. Such forecasts will no doubt have weighed on the Fed’s decision yesterday. Later in the day we have the Philadelphia Fed Business Optimism which is forecast to improve, followed by the Genscape Cushing Estimate – another crude oil stockpile indicator centred on the now well-known Cushing, Oklahoma storage facility oft used as a reference for those shouting about the global supply glut.

US Light crude ($43.5) and Brent ($55.4) both jumped from recent lows thanks to yesterday’s dovish FOMC speech, which saw the USD Dollar drop from highs although it has seen a retrace overnight. The Oils have work to do to break the trend of falling highs dating back to the beginning of the month with further growth in US stockpile data yesterday and global production/demand uncertainty continuing to weigh heavily.

Gold has held firm after making made good progress from recent $1140 lows helped by a weaker USD, however, the yellow metal has still to breakout from the downtrend channel dating back to 20-Jan. Still potential for a revisit of November lows $1130 although with last night’s support in such proximity maybe this is where the gold bugs call the bottom.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan All Industry Activity In-line, rebound

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Ted Baker posts 24 pct rise in profit

- UK gets green light for superfast broadband margin test

- Auto Trader IPO pricing values group at 2.3 bln stg

- Auto Trader prices London listing at 235 pence per share

- Chemring says board's expectations for FY remain unchanged

- Premier Farnell FY revenue 960.1 mln stg vs 968 mln stg

- Savills pretax profit up 21 pct, makes solid start to year

- Next annual profit jumps 12.5 pct

- Ophir Energy says 2015 will not see levels of exploration drilling as last yr

- Travis Perkins announces creation of 4,000 jobs

- Arbuthnot Banking Group FY pretax profit jumps 43 pct

- EnQuest books $335 mln in impairments after oil price plunge

- Lamprell says year-end backlog of $1.2 bln

- AstraZeneca announces collaboration with Japan's Daiichi Sankyo

- Mirada appoints new CFO