Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

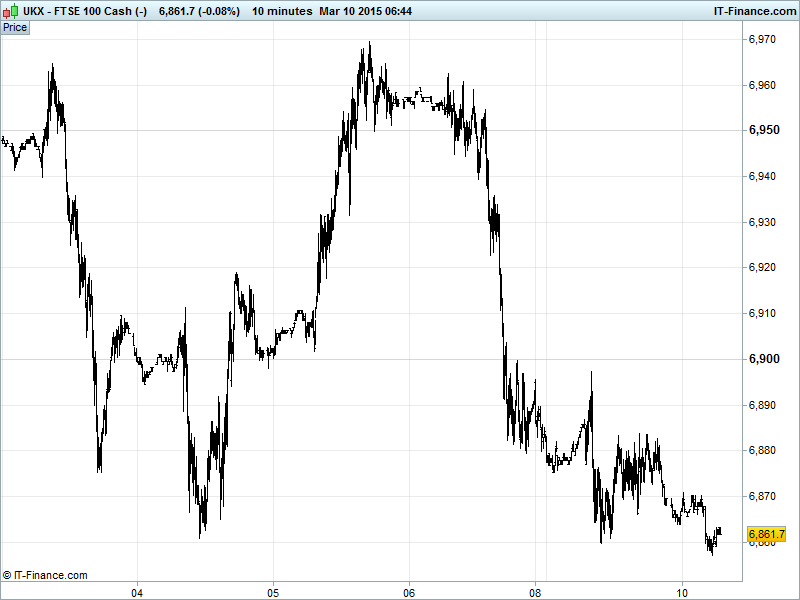

UK 100 called to open -15pts at 6860, making another test of March lows 6860 as the index continues to weaken back from last week’s revisit of recent highs 6970. Potential for retrace to end-Jan lows 6720, keeping the index in a sideways trend since mid/late Jan. Feb rising support abandoned. Watch levels: Bullish 6900, Bearish 6850.

The negative open comes despite US markets closing higher on excitement surrounding Apple’s new smart-watch and the launch of Eurozone QE, with continued focus on Friday’s strong US payrolls data and Fed chatter heightening expectations of a Fed rate rise being just round the corner, sending the USD to 11.5yr highs and remaining a hindrance for commodities-linked securities. Mixed China inflation data overnight (CPI better off 5yr lows, PPI worse) adds to woes about slowing growth in world’s #2 economy, but still likely boosts hopes of more stimulus, however, Eurozone/Greek progress remains pedestrian/tenuous at best.

US markets closed positive Monday, buoyed by Apple shares after the release of its new smart-watch while US treasuries were supported by the rally in European bond markets on the start of the ECB QE programme. Fixed income markets are, however, some way from paring losses after Friday’s strong non-farm payrolls. The Fed’s Mester and Fisher were singing hawkishly, saying a rate lift-off is appropriate in the first half of 2015 and that a gradual rise would be better than a short sharp shock. Both believe the US economy is in a sustainable recovery with inflation reasonably likely to increase.

Asian bourses are mixed this morning. Japan’s Nikkei rose overnight as the yen touched a 3-month low against the USD and Australia’s ASX erased earlier gains as investors/economists overlooked a positive lead from Wall Street and saw China’s better than expected CPI as a Lunar New Year phenomenon - not sufficient to dispel policy makers’ worries over possible deflation. Indeed, Chinese factory prices (PPI) extended their prolonged fall in a slowing economy.

In focus today will be the US wholesale inventories looking for an increased slowdown in trade sales with inventories unchanged. Elsewhere, the EU finance ministers are meeting again to try to take the Greece situation forward, and Mark Carney will be taking to the stage to talk the UK economy. UK challenger bank Aldermore’s £651m IPO is due today at a price of 192p per share, having been delayed since the back end of 2014.

US Light crude ($50) and Brent ($58.2) off Monday’s highs, with the former holding its March rising lows (just) but the latter struggling back to late-Feb lows, held back by an ever-strengthening USD and ever increasing US stockpiles coupled with uncertainty as to what OPEC will do to protect market share, having increased prices to Asian, US and northwest European consumers. Oil bottomed out?

Gold continuing to fall back from Jan highs $1307, with potential for November lows of $1130 to be revisited as a stronger USD hurts safehaven demand and keeps the yellow metal in a declining channel with inflation remaining very much elusive.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Sales Life-for-like Miss, stable

- Aussie NAB Business Confidence Mixed

- China Inflation Mixed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Cairn reports 2014 loss after tax of $381 mln

- Antofagasta says court rules against Los Pelambres unit

- WPP agrees to acquire stake in FlowNetwork, Sweden

- Sales growth picks-up at UK online grocer Ocado

- FCA says to investigate Capita Financial Managers and Blue Gate Capital

- Close Brothers Group H1 adj oper profit up 16 pct

- Grainger says may take legal action against Clifden

- UK lender Aldermore sets IPO offer price at 192p a share

- Grafton FY operating profit up 43 pct , outlook positive

- G4S full – year profits rise, ups provisions for UK work

- G4S sees profits rise but UK contract problems remain

- Igas Energy PLC – UK Shale Farm out Agreement with INEOS Upstream

- SEGRO PLC – SEGRO AGREES TO SELL ENERGY PARK MILAN

- Prudential operating profit of 3,186 million pounds up 14 percent

- Credit Suisse buys some insurance with Prudential CEO

- Sterling Energy says Phil Frank to step down on March 13

- Iron ore languishes at record low as Chinese steel sinks

- John Menzies FY pretax profit 25.7 mln stg

- IP Group to raise about 128 mln stg via firm placing

- Prudential CEO Tidjane Thiam is to step down to join Credit Suisse