Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

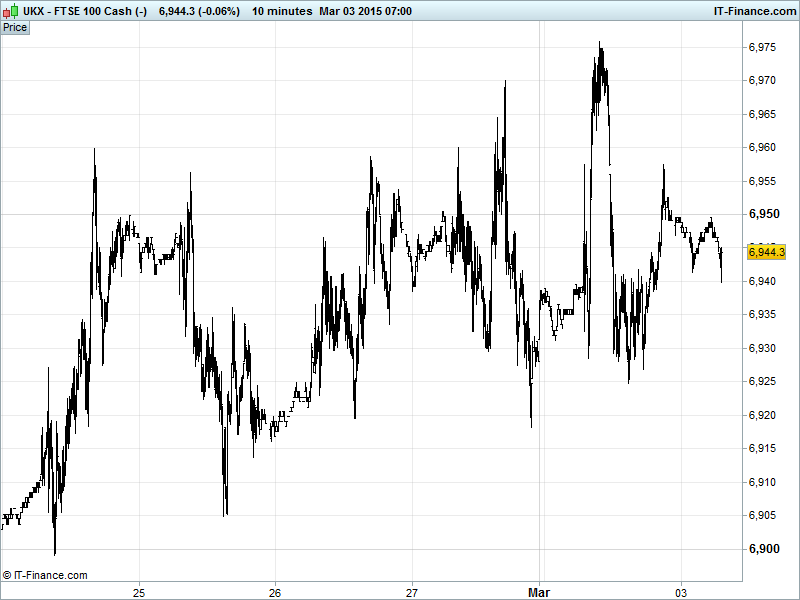

UK 100 called to open +10pts at 6950, still hanging around 6950, failing to make a decisive break to the upside as momentum wanes a little seeing the index moving sideways over the last 3 sessions. However, that didn’t stop it from testing higher and registering a fresh all-time high yesterday. The February trend of rising support still holds as does the uptrend from mid-December. Still potential for bullish ascending triangle (imperfect) to break to the upside. Watch levels: Bullish 6990, Bearish 6880.

The mildly positive opening call comes opens despite the RBA unexpectedly deciding against a rate cut disappointing markets and seeing the Aussie ASX in the red overnight, even if the central bank left the door open for further monetary stimulus at forthcoming meetings to foster growth and inflation. Strong German Retail Sales this morning show a big rebound, offsetting concerns yesterday about discussions of a third Greek bailout (denied of course) although the nation faces a cash crunch in coming weeks if revised austerity can’t be agreed and passed into law, releasing much-needed cash from Eurozone creditors and the IMF. Markets cautiously optimistic ahead of Thursday’s updated China growth target and Friday's update on the US labour market.

US bourses closed with modest gains with the Nasdaq above the key 5000 level for the first time since the dot.com bust nearly 15 years ago and DJIA making a new intraday high despite mixed macro data (ISM manufacturing miss, PMI manufacturing beat, Construction Spending miss, Personal Income & Spending miss, Core spending in-line). Sentiment buoyed by the weekend’s China PBOC rate cut news flowing through.

Asian bourses in the red with a stronger AUD following the RBA’s rate decision weighing on Aussie equities (ASX), offsetting strong macro data (Building Approvals rebound, lower current account deficit, higher net exports of GDP) and recent optimism about stimulus from Beijing boosting growth from the big trade partner. Japan’s Nikkei hindered by slightly weaker USD (following AUD strengthening) and thus stronger JPY. Stocks failing to be buoyed by the positive Wall street close, with focus returning to slowing China growth as the nation gets set to release its updated growth target on Thursday.

In focus today we have Eurozone PPI which is expected to remain deflationary, although slightly less than in December. Canadian GDP seen rebounding in December with a slight improvement in raw material/industrial product price declines although the annualised quarterly rate of GDP is seen slower. US ISM New York and US IDB/TIPP Economic Optimism will be looked to for an update on business sentiment.

US Light Crude ($49) turned upwards overnight following a spike on Monday, after closely followed data service Genscape Inc. reported supplies in a key storage hub grew by a smaller-than-expected amount last week. The EIA will report its inventory data for the week-ending Feb 27 on Wednesday, with further burgeoning US stockpiles expected to add to global supply glut worries as many traders forecast another sharp dive in prices. The US benchmark has recovered slightly from its late Feb downtrend while Brent Crude ($60) remains supported by rising lows from 12 Feb.

Gold ($1208) sunk below $1200 overnight with a heavy dollar basket holding up around recent highs but has since recovered as both Greek and Russian uncertainty prevail – rumors of a third Greek bailout, while being denied by the EU’s Juncker, will no doubt remain on the grapevine while other worries dig in surrounding a possible cash crunch, tax confusion and missed deadlines. Post Lunar New Year demand in Asia also helped the yellow metal, which is edging back into its uptrend from 24 Feb.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Aussie Building Approvals Beat, Improved

- Japan Labor Cash Earnings Beat, Maintained

- Swiss GDP Beat, maintained

- Germany Retail Sales Beat, Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- BAT offers to buy out Souza Cruz stake

- Stagecoach says on track to meet annual expectations

- Ashtead raises full year expectations after strong Q3

- Barclays takes extra 750 mln stg FX provision as profits rise 12 pct

- Barclays 2014 bonus pool down 22 percent to 1.86 bln stg

- Travis Perkins says expects to outperform market as year earnings jump

- Housebuilder Taylor Wimpey seeing strong spring demand

- Glencore 2014 profit in line, takes $1.1 bln charge on commodity prices

- Set – top box maker Pace expects growth in 2015

- Pace sees FY 2015 revenue about $2.75 bln

- Tullett Prebon says FY pretax profit declines to 86.6 mln stg

- Punch Taverns names Duncan Garrood as chief executive

- Regus full-year revenue rises

- Laird says FY revenue in sterling rises 5 pct

- Moneysupermarket.com says year has started well

- Rotork says chairman Lockwood to retire in April

- Sausage-skin maker Devro's full-year profit declines

- Vesuvius full-year revenue falls