Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

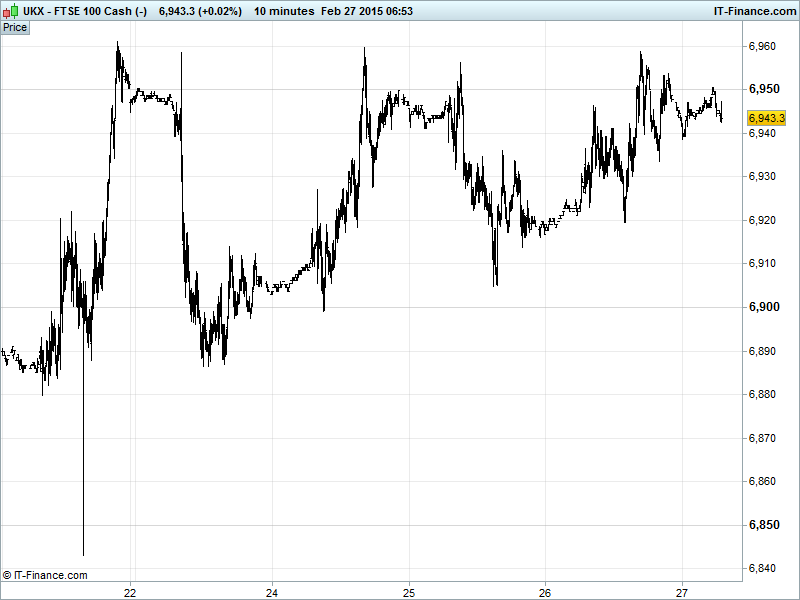

UK 100 called to open -5pts at 6945, back from a third successive test of last Friday’s fresh all-time highs 6961. With rising lows from 19 Feb intact at 6930 and resistance around 6960 this looks increasingly like an ascending triangle/wedge pattern which could break to the upside and allow the index to make a more decisive move into all-time high territory. February uptrend still valid with support at 6885. Watch levels: Bullish 6975, Bearish 6870.

The negative open comes as the BoE’s Shafik gestured towards an imminent gradual and limited rise in interest rates, perhaps taking cues from the US, to smother suspicions of her being the ‘mystery dove’ in the MPC’s Feb minutes. Elsewhere, ever souring relations between Greece and its creditors emerged with a ‘visibly angry’ Wolfgang Schaeuble reacting to Varoufakis’ comments about debt restructuring on Greek national radio. A ‘stunned’ Mr. Schaeuble had been trying to convince German MPs to support the latest bailout extension deal amidst a media storm in which its biggest selling newspaper posted headlines shouting “no more billions for greedy Greeks.” The saga continues.

US markets finished mixed on Thursday as investors digested mixed economic data and oil price declines. US Fed thoughts focussed on the hawkish with Bullard and Yellen saying a rate lift-off is pretty much the median forecast among peers. Fisher commented that the strong USD, in an undoing of the good that came out of Yellen’s prior testimony, will have offsetting effects on the economy which is seeing stout growth while Mester sees a ‘soon and slow’ rate rise being preferable to a ‘slamming on of the brakes’ sometime in the future.

Asian bourses were largely higher, but held back by emerging market indices. In Japan, a bad raft of economic data had quite the opposite effect on the Nikkei, with a weak Yen and investors confident that the figures will encourage further stimulus from Abe’s government. The BoJ’s Kuroda, however, remains confident in the economic recovery and wants to wait and see what happens to oil prices and inflation before making a decision to conduct monetary policy.

The Australian ASX closed up 0.3% after the Westpac said it expected the RBA to either cut its cash rate by 25bps or adopt a QE approach next week, while China’s Hang Seng index was up on a weak Yuan, the result of heavy selling due to a flurry of disappointing economic indicators fuelling growth worries.

In focus in Europe today we have German CPI; in the US a predicted shrinkage in annualised GDP will face off against small improvements in pending home sales. The University of Michigan Confidence index is expected to improve too, while rounding off the day will be the good ol’ Baker Hughes Rig Count…

Oil has dropped back, hindered by sharp gains by the USD which took US light Crude as low as $48 and Brent back to $60 before recovering slightly on overnight Japanese Industrial Production figures. Drivers including US inventory builds and record domestic supply still weighing along with global supply glut fears - the $12 spread between the two is close to its lowest in 13 months. The former’s break back below $50 stifles its recovery from Jan lows (Feb flat), while the latter holds its uptrend (Feb +15%), close to recent highs buoyed by speculation that global demand will recover this year. Watch out for US Rig Count data this evening and Chinese PMI Manufacturing data this weekend.

Gold ($1210) gave up yesterday’s gains to $1220 after the USD strengthened markedly, although it maintains its uptrend from Tues lows of $1190 thanks to a mixed macro-economic picture globally and geopolitical risk still rife. This keeps it above rising support from early Nov and its exit from a restrictive 2-month down channel, with support from rising Chinese demand signals and changing views on US interest rates.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK Consumer Confidence Miss

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Rightmove profits rise as more agents use service

- Britain's Lloyds to pay first dividend since financial crisis

- Redefine International signs shopping centre lease with Primark

- Nikon Corp offers to buy UK – listed Optos for 260 mln stg

- Pearson posts 5 percent rise in 2014 profit as restructuring ends

- IAG upgrades 2015 profit forecast

- Spectris FY adj pretax profit down 6 pct

- Old Mutual 2014 profits rise 16 percent

- Fyffes full – year EPS rises 26.6 pct

- UK says to get at least 100 mln stg from Lloyds payout

- Valve – maker IMI's full – year group revenue falls 3 pct

- Events organiser UBM'S full – year adjusted operating profit falls

- Intu Properties FY net rental rev 397 mln euro

- Rentokil confident on year ahead but warns on Europe

- Old Mutual funds under management rise 6 pct to 319 bln pounds

- Spectris's full – year adjusted pretax profit falls 8 pct as costs rise

- UBM Plc FY rev down 6 pct

- Acromas sells 66 mln shares of Saga Plc - placing agent

- Ireland's Malin seeks up to 325 mln euros in biotech IPO

- Man Group to repurchase $175 mln of its shares