Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

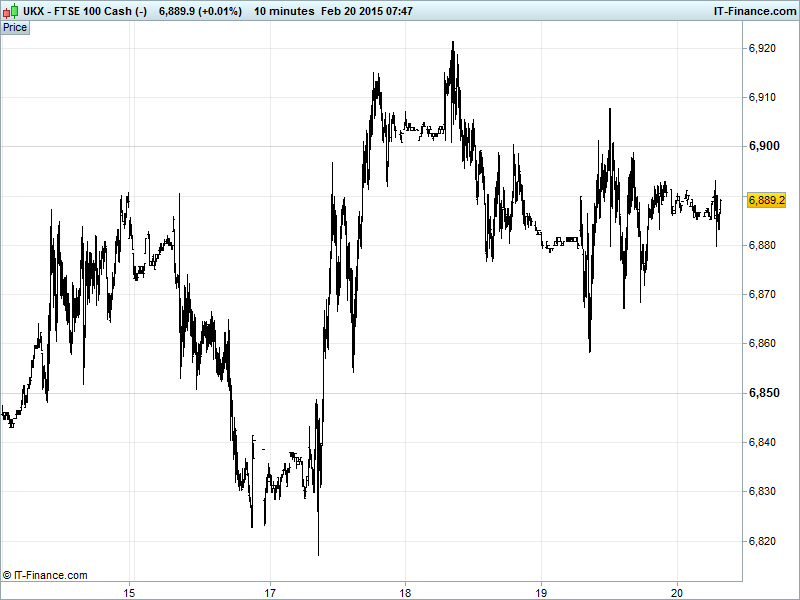

UK 100 Index called to open flat at 6890, still hanging around the 6880 mid-point of recent 15yr highs 6921 and the trend line of Feb rising support at 6850. Potential for Feb uptrend to continue, with completion of double bottom pattern from Oct/Dec lows, but also for progress around 6900 to fail and a correction ensue to Feb lows 6720, possibly even lower. Updated Watch levels Bullish 6930, Bearish 6830.

The flat open comes after confidence turned to despair yesterday when news came of the rejection of the Greek bailout proposal which failed to ‘meet existing requirements’ and was described by German officials as a ‘trojan horse’ that left immense room for interpretation. Contingency plans are reportedly being made for a potential ‘dirty exit’, although a US think tank has said that Greece and the Eurogroup may still strike a short-term deal today.

We note this morning that Germany has tightened the thumbscrews somewhat by recommending no extension of Greek banks’ recapitalisation funds following their survival of a stress test last year while ECB minutes revealed a large number of members were in favour of buying more European government debt.

US bourses closed mixed again (S&P down, Wall St. down, NASDAQ up) on the back of the above news and mixed internal data. The Philadelphia Fed business outlook declined to 5.2 from 6.3 while the January Leading Economic Index rose 0.2% from a revised 0.4% last time around. The Fed’s Bullard commented that ditching the word ‘patient’ at the March meeting could make way for the Fed to increase rates in June, but that even after an increase in rates, they will remain low for the next couple of years.

In Asia markets were again varied, with eyes the world over concentrating on Greece and the Eurogroup and growing fears that an exit from the Eurozone is becoming a distinct possibility. Volumes still thin due to the closure of several markets for Lunar New Year holidays. In Japan, weak PMI data weighed little on bullish rhetoric from BOJ Governor Kuroda who said the central bank has many policy options available to chase the country’s 2% inflation target. Confidence in an economic recovery prevailed to see the Nikkei rise 0.3% in morning trade after closing Wednesday at a 15-year high.

In Australia, markets retreated again with key trading partner China out of the loop for Lunar New Year and falling oil prices (EIA data again showing an increase in US stockpiles, more than expected) impacting energy stocks.

In focus this today will be a raft of European and American PMI data with consensus for manufacturing growth in the US, Eurozone and Germany, while France is expected to lag behind. In the UK public finance data forecasts indicate a reduction in public sector borrowing while retail sales are expected to show contraction for the month and expansion for the year. Rounding off the day will be the Baker Hughes Rig Count which might tell us that the number of US drilling rigs has fallen again. Stranger things have happened…

After falling on bearish API US stocks data on Wednesday which revived global oversupply fears, US Light Crude and Brent Crude found support at $50 and $58 respectively, generating a trend line of rising lows from early Feb. This has seen prices retrace some of their losses from recent recovery highs despite yesterday’s US EIA inventories data showing another weekly build (more than consensus, almost double, stocks at new record) and stronger USD. Investors/speculators already looking to this week’s Baker Hughes US Rig Count, expecting another weekly drop to boost already over-egged hopes of US production declines offsetting OPEC stubbornness.

Gold’s bounce off 3-month rising lows at $1200 is looking increasingly suspect with potential for the falling channel from 22 Jan to continue. A USD bounce is hindering initial progress which had been helped by much uncertainty regarding Greek success in renegotiating its debt situation, with Germany standing firm and rejecting the latest ‘Trojan horse’ extension proposal, increasing the chances of Greece running out of money or even leaving the single currency.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Manufacturing PMI Miss, Deteriorated

- Germany PPI Miss

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Standard Life operating profit jumps 19 pct to $931 mln

- Man Group buys NewSmith's investment management business

- 3i Infrastructure announces investment in two storage terminals with Oil tanking

- Essentra FY revenue at constant currency rises 14 pct

- Standard Life says Non – Executive Director David Grigson to retire