Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

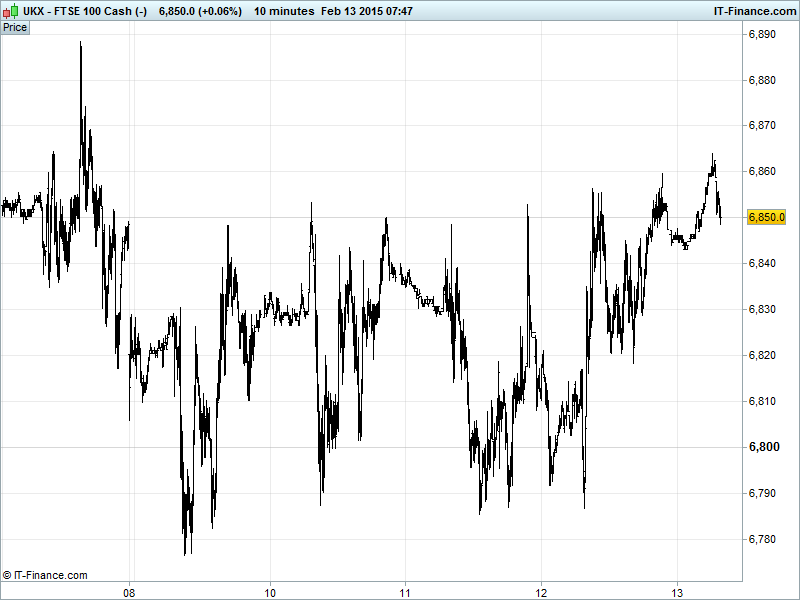

UK 100 Index called to open +25pts at 6850, still trying to break above the recent 6850 4-day bugbear level of resistance allowing for a return to recent highs 6905 and the top of the sideways channel since 22 Jan. 6790 support still holding after multiple tests corresponding with rising lows from mid-December. Watch levels Bullish 6860, Bearish 6780.

The positive opening call stems from continued optimism that Greece will (eventually) reach a deal with its creditors or that the situation will be defused (ECB accorded Greek banks more emergency money - ELA) and supported by the Russia-Ukraine ceasefire starting Sunday even if fighting continues and the Ukrainian President said implementation of the agreement could be difficult suggesting a fragile accord.

US stocks closed moderately higher buoyed by geopolitical confidence and an oil price rebound despite a raft of disappointing US macro data (Jobs, Retail Sales, Bus Inventories) suggesting hopes that this goes towards delaying the Fed in its plan to raise rates this year, even if offset by persistently hawkish Fed chatter (Plosser + Fisher).

After the US close, AIG reported a 67% fall in Q4 profits, missing estimates due to low rates, financing, debt repayments and bolstering of reserves while Cisco reported strong Q2 results on robust switching sales. Note German Jan Wholesale Prices this morning remained under pressure in January, vindicating ECB action, but German Q4 GDP growth surprised to the upside, accelerating, and the French reading was in-line.

Asian stocks cautiously optimistic into the week-end taking the baton from Wall Street amid hopefulness over developments on Ukraine and Greece even if concrete signs (an actual RU-UKR ceasefire and an actual Greek deal) are unlikely confirmable until early next week.

Japan’s Nikkei hindered by stronger JPY while Hong Kong’s Hang Seng buoyed by China equities higher in spite of slower growth in the China Jan Leading Index? Note Australia’s ASX outperforming thanks to Rio Tinto (RIO) results and share buyback, the higher oil price and dovish RBA comments on growth (below trend for longer) supporting calls for more rate cuts/policy easing, even if policy easing may become less effective.

In focus today we have the advance reading for Eurozone Q4 GDP which, after the beat by Germany this morning, could prove better than consensus 0.2% growth which is the same as in Q3 while the afternoon is focused on a likely acceleration in falling US Import Prices and US Uni of Michigan Consumer Sentiment being confirmed at its 7yr high of 98.1. Watch the Baker Hughes Rig count update for its potential to alter perception on oil supply and move the price of a barrel.

Gold ($1224) continues to recover this morning from late $1220 lows helped by a weaker USD (poor macro data) and drawn out talks between Greece and the Troika. Tire eyes also try to focus on Ukraine where violence appears to be escalating ahead of Sunday’s planned ceasefire, with the resultant selection of uncertainty increasing demand for the safe haven metal. Gold, having bounced off February lows this week, remains in the lower half of a downwards channel from January highs.

Brent ($60) and US Light crude ($52) remain in their respectively chaotic uptrends around March futures expiry as the balance again shifted in a continuing tug of war between economic drivers. A weakening USD and more news of capex cuts by both oil majors and US frackers encouraged buyers back to the market yesterday and recent highs, as we head off a week that has seen price volatility hit its highest level since the 2008 crash.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Conference Board Econ Index Growth, but slowed

- France GDP In-line, stable

- Germany Wholesale Price Index Still weak

- Germany GDP Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Virgin Media and Liberty Global announce largest investment in UK's internet infrastructure

- Anglo American takes $3.9 bln writedown after commodity price slide

- Quintain Estates says performance of Wembley Park assets continues to improve

- Trinity Mirror raises provision for civil phone hacking claims

- Fresnillo sees adverse impact on FY gross profit of about $20 mln

- British Land starts development of Paddington site

- JLT says Ardian to buy co's stake in Siaci St Honoré's holding firm Milestone

- RPS Group acquires Klotz Associates for $24.1 mln

- Rolls-Royce downgrades 2015 profit forecasts