Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

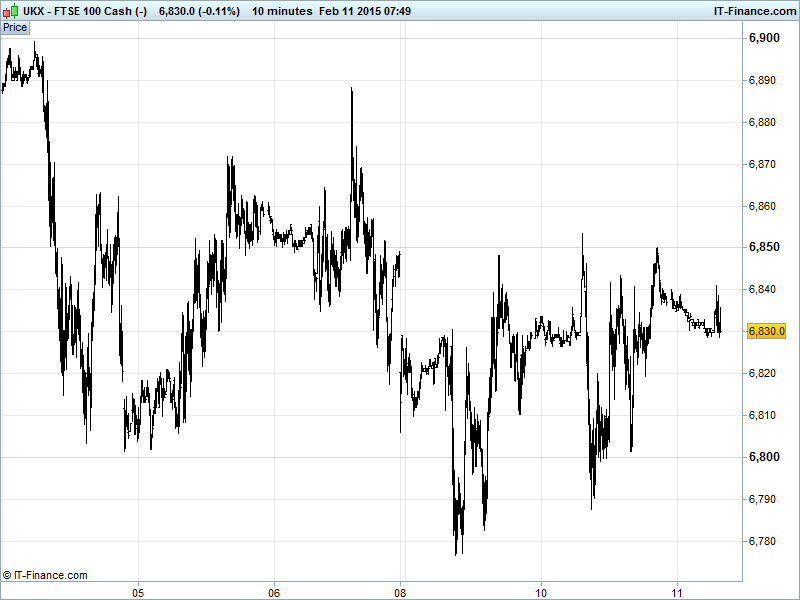

UK 100 Index called to open flat at 6835, holding above 6800 despite another test yesterday, but failing to make progress on this week’s resistance around 6850. Still in the upper half of the 6720-6905 sideways channel from mid-Jan but with a narrowing range. The uptrend from December lows is intact with Bulls eyeing a retest of recent highs 6905 while Bears hopeful of a drop to the channel base. Updated Watch levels remain Bullish 6860, Bearish 6770.

Another muted open comes from persistent uncertainty about Greek debt negotiations with the new government rejecting any increase in debt load and new PM Tsipras easily surviving a parliamentary confidence vote after pledging to never allow Greece to return to the era of austerity and bailouts.

The China Securities Journal suggests the possibility of more PBOC easing while geopolitical risk is rising with fighting intensifying in Ukraine at the same time as ceasefire talks take place and US president Obama warns Russian counterpart Putin about continued aggression towards Ukraine.

US stocks closed higher on optimism about a Greek debt renegotiation (despite mixed signals from Greek and Eurozone politicians, notably Germany) as well as some upbeat corporate updates and in spite of oil giving up ground on concerns of market oversupply and a stronger USD on hawkish Fed chatter.

Asian stocks mostly lower again, despite a positive lead form Wall Street and after initial gains as concerns about the chances of a Greek debt crisis rose and the fall back in the price of Crude weighed on sentiment. Australia’s ASX pared gains to close lower, with corporate earnings worries offsetting Consumer Confidence going positive after the recent rate cut and a rebound in Home Loans. Note Japan’s Nikkei closed for holiday.

In focus today we have a rather quiet line-up comprising a Greek 3-month bond auction which will be eyed for likely eye-watering interest rates it will have to pay based on the current Greece-Eurozone/troika standoff. US Crude Stocks will be watched for clues as to the direction of the price of oil, while Eurogroup Finance Ministers meet to discuss the Greek situation towards the end of the day.

Gold ($1235) is trending slightly higher this morning, after its falls of yesterday, with any significant progress stifled by conflicting drivers - most notably a strong USD and ongoing Eurozone worries. The short term possibility of a Grexit and war in Ukraine are providing safe haven support while a healthy US economy is keeping a significant rally largely at bay. The yellow metal remains in a falling channel from Jan-22 highs having found support for the time being around $1230 and likely resistance around $1252.

Oil also off its worst levels of the last few days, WTI and Brent finding support around $50 and $56 respectively following the API reporting a smaller than expected expansion in US stockpiles ahead of the EIA stocks report this afternoon and despite Iraq and Iran joining the Saudis cutting export prices to Asia (to the lowest in a decade), suggesting the OPEC market share battle intensifying. Both prices for a barrel see Feb rising lows intact.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Consumer Confidence Improved

- Australia Home Loans Beat, Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Redrow confident after first – half profit near doubles

- Chip designer ARM beats Q4 expectations on strong licensing

- Reckitt Benckiser forecasts 2015 similar to 2014

- Speedy Hire sees FY results in line with its expectations

- Aquarius Platinum H1 group mine EBITDA rises helped by higher production

- Glencore to divest Lonmin stake, cut expenditure to counter to weak prices

- Lonmin notes Glencore's proposal, says constructive way forward

- WS Atkins to achieve improved operating margin through second half of year

- Thomas Cook Q1 loss narrows, on track for growth in 2015

- Cobham to take 15 mln stg one – off hit on 2014 results

- Interxion and TelecityGroup reach non – binding agreement on all – share merger

- Warburg Pincus cuts Poundland stake to 16.4 pct

- Electrocomponents underlying sales for 4 months to Jan. 31 rises 5 pct

- Tullow Oil makes first loss in 15 years, scraps dividend