Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

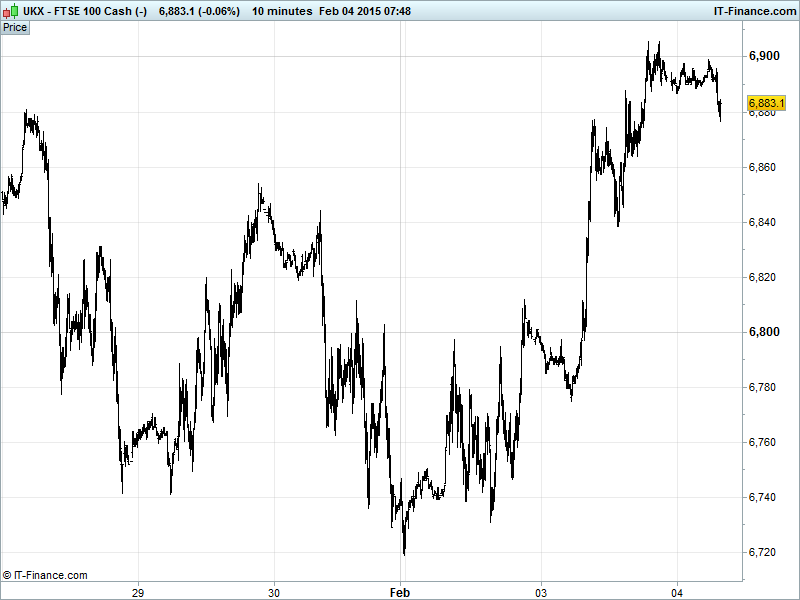

UK 100 Index called to open +10pts at 6880, having tested 2014 highs of 6905 overnight following a strong rally yesterday, however, the level could be resistance near-term keeping us within the sideways channel 6730-6900 from 21 Jan. The bulls are still hopeful of 6950 all-time highs being challenged with the bullish flag pattern highlighted yesterday working out nicely. Updated Watch levels: Bullish 6915, Bearish 6830.

The positive open follows a strong finish yesterday and gains in the US and Asia overnight helped by assurances to European taxpayers from new Greek PM Tispras, further gains in the oil price and despite ratings agency S&P taking negative action on a number of European banks (incl. BARC, HSBC, LLOY, Credit Suisse and Deutsche Bank) and China HSBC PMI Services deteriorating to 6-month low in January.

US bourses closed higher yesterday with more gains for the oil price helping out energy stocks and dovish Fed rhetoric (2015 rate rise would delay slow inflation recovery) helping offset macro data disappointments (ISM New York, Factory Orders). After the close, Disney Q4 results beat expectations helped by blockbuster film Frozen.

Asian bourses higher, taking the baton from Wall Street, helped by the higher oil price. Japan’s Nikkei benefiting from BoJ Governor Kuroda saying the bank will do its utmost to hit its 2% inflation target and solid PMI Services. Note Australia’s ASX buoyed by higher commodity prices and weak China data raising stimulus hopes, but stocks in China and Hong Kong hindered.

China HSBC PMI Services remained in growth territory but adds to negative official readings over the weekend with new orders slowing and output prices down, along with evidence of struggles in other sectors notably manufacturing and real estate which will heighten fears of slowing growth but add to expectations of more government/PBOC intervention/stimulus.

In focus today will be the final January European PMI Services updates with France seeing confirmed dropping into contraction but Germany and the Eurozone as a whole accelerating their expansion. The UK reading is also seen accelerating its very strong growth. Eurozone Retail Sales expected flat adding to regional growth woes and vindicating ECB intervention.

In the afternoon, the US ADP Employment change will be eyed for any clues as to the strength of Friday’s Non-Farm Payrolls. The US Services PMI is expected confirmed growing faster in January and the ISM Non-Manufacturing composite flat.

Gold teased us with a break above the trend of falling highs from Jan 23, before meeting resistance at Jan 30 highs $1285 and resuming its 2-week downtrend. It is now back within the $1250-1275 range hindered by receding fears about Greece in Europe and competition from other safehavens and despite a softer dollar following dovish Fed rhetoric.

Oil continues to make progress off its multi-year lows (WTI $52/barrel and Brent $57.7) amid hopes that prices may have found a bottom in January and that cutbacks in sector investment may help restrict supply, however, both are off their highs and fears remain that the recent up move is merely a short squeeze.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop Price Index Beat, Improved

- Japan Services PMI Deteriorated

- China Services PMI Deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- HSS Hire Group sets IPO offer price at 210p/share; bottom of range

- Synergy Health third-quarter underlying revenue up 9.6 pct

- Strong British and German demand drives maiden Sky results

- Victrex posts 14 pct rise in first-quarter revenue

- Anglo Pacific plans to buy royalty interest in New South Wales coal project

- Anglo Pacific Group revises dividend policy

- Hargreaves Lansdown assets under administration rise to record 49 bln stg

- Ryanair January traffic up 30 pct to over 5.89 mln customers