Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

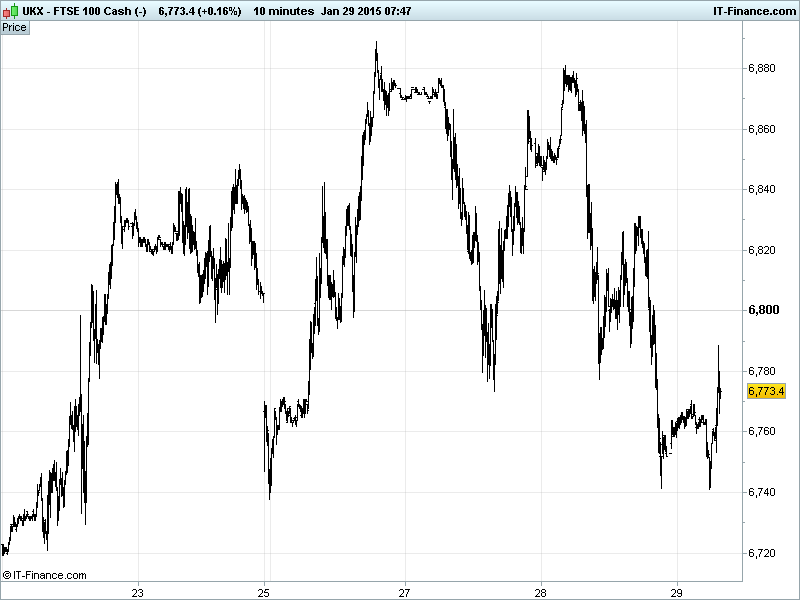

UK 100 Index called to open -55pts at 6570, having made an overnight break below 6775 support and the trend-line of rising support dating back to 19 January. While this puts the January uptrend in jeopardy, opening up the possibility of a correction with the rising trend-line reverting to resistance around 6800, we note support around 6750 which could provide bullish assistance. Updated Watch levels: Bullish 6820, Bearish 6720.

Drivers for the negative open include the US FOMC Statement which saw the Fed boost its economic assessment, while playing down low inflation and maintaining its pledge of patience in raising rates this year, offsetting some of the recent hopes of a rate rise being delayed into 2016, even if monitoring of ‘international developments’ (other central bank action?) gives them flexibility to hold off.

The resulting stronger USD has dented Asian stocks and taken Oil to an almost 6yr low $44. Note Chinese stocks suffering as regulators increase scrutiny on margin loans. Given the uncertainty surrounding Greece’s negotiations with international creditors, it is no surprise to see ratings agency S&P put the nation’s debt rating on watch for downgrade.

Note corporate results helping buoy sentiment this morning include, Deutsche Bank (DBK; profit versus forecast loss, lower litigation costs and provisions), Nokia (NOK1V; back to profit) and Nomura (Q3 profit unexpectedly surged) even if Diageo (DGE) missed expectations and Royal Dutch Shell (RDSB) was in-line making big cuts to capex plans. After the US close, Facebook (FBK) beat expectations with solid Q4 revenue and earnings growth but Qualcomm fell 8% after hours as it cut chip guidance for H2.

US bourses closed lower, hurt by the Fed statement and potential for of a rate rise this year, as well as continued uncertainty regarding how Greece will deal with its debt situation which saw Greek stocks, banks especially, hammered further.

Overnight, Asian bourses took negative lead from the US, with the fall in oil price and disappointing Japanese Retail data adding to the gloom coupled with Chinese equities falling yet further as regulators step up scrutiny on margin accounts.

In focus today we have German Unemployment seen stable while Eurozone Confidence indicators should improve a touch, although German Consumer Price inflation is likely to be supportive of recent ECB action to fight deflation with QE.

In the afternoon, US Pending Home Sales are expected to deliver similar December growth as in November while we have results from Ford (F) which will be of interest given other corporates struggles with the strong USD and outlook. After the US close, results from Google (GOOG) and Amazon (AMZN).

Gold has extended its declines from near $1300, as investors weigh up the outlook for higher US interest rates following the Fed Statement which saw the FOMC boost its assessment of the world’s #1 economy and its labour market, and downplayed low inflation. The declines have seen the trendline of 2015 rising support tested and key will be whether 2-week lows of $1270 hold up via safehaven demand on Greek concerns, US corporate results disappointments and global growth worries.

US Light Crude under pressure from rise in US stocks (oversupply likely to persist) and stronger USD following the Fed statement, with the price of a barrel down near a 6yr low of $44. Note Brent Crude more resilient at $48.5, off 2-day highs but still well within recent 9-day sideways channel.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Retail Sales/trade Miss, deteriorated

- Australia Export Prices Beat, flat

- Australia Import Prices Miss, didn’t rebound as much

- UK Nationwide House Prices In-line

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- National Grid starts share buyback programme

- Trial finds GSK Ebola shot is safe and provokes immune response

- Russia's Polymetal Q4 revenue up 4 pct

- AstraZeneca bets on gene editing for broad range of new drugs

- Ocado in deal for fourth UK distribution centre

- PayPoint sees FY results "within range" of market expectations

- Shell to cut spending by $15 bln over next 3 years

- Shell says organic capital investment to be lower in 2015

- Diageo posts lower-than-expected sales

- Great Portland Estates sees higher rates of rental growth

- Galliford Try secures extra care contracts worth 72 mln stg

- John Laing eyes market cap of up to 865.5 mln stg with float

- Pub firm M&B sees sales rise over Christmas period

- ITE sees FY Russia volume sales about 20 pct lower than last year

- Royal Mail Chairman Brydon to step down

- 3i Group's net asset value up 5 pct in last quarter

- Soco cuts 2015 investment budget to focus on Vietnam, Africa

- Renishaw H1 rev 223.8 mln stg

- RPC Group says adjusted operating profit in line with expectations

- De La Rue finance chief to step down in July

- Platinum producer Lonmin maintains output target, cuts spending

- Cranswick posts 3 pct decline in Q3 underlying revenue

- Kaz Minerals hits annual copper output target