Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

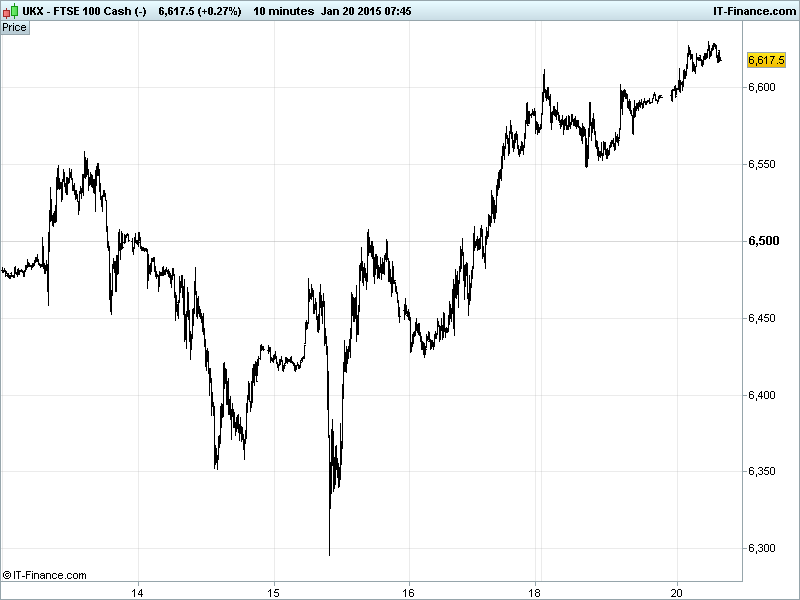

UK 100 Index called to open +35pts at 6620 making further progress following its break above 6530 and the trend of falling highs from December. This opens the door for potential completion of a bullish flag pattern around Nov/Dec highs 6765, however, the 200-day MA at 6650 and falling highs from September at 6685 still need bettering. Watch levels: Bullish 6655, Bearish 6590.

The positive open comes after China Q4 GDP surprised to the upside suggesting its economic slowdown isn’t as severe as feared, reviving optimism in global growth even if it does cool hopes/delay likelihood of further China stimulus being forthcoming. Retail Sales and Industrial Production growth also impressed in the face of a slowing trend for growth in the world’s #2 economy.

With US markets closed, Asian bourses took their cues from European gains on continued expectations that the ECB will ride to the ‘resQE’ on Thursday, with China data helping maintain the rebound in Chinese stocks after their steep declines. Japan’s Nikkei helped by stronger USD/weaker JPY boosting exporter names although Australia’s ASX in the red despite better China growth, possibly dented by prospect of less stimulus.

Overnight, the IMF cut global growth forecasts by the most in 3yrs following the World Bank last week, but with more optimistic predictions and downgrades to emerging markets (China cut) rather than advanced economies (US upped), warning monetary policy needs to stay accommodative to fight deflation risks and a lower oil price not being the only answer to boost expansion.

This morning’s German Producer Price Inflation reading (17th consecutive annual decline) adds to deflationary pressure on the Eurozone and to the weight of argument in favour of the ECB announcing sovereign bond buying on Thursday in order to help rekindle growth/hope and boost sentiment/confidence in the region.

In focus today, amid another light data line-up, we have German ZEW Surveys which are expected to show improvements in current situation and expectations. Thereafter it’s quiet until the latest US NAHB Housing Market Index reading mid-afternoon with forecasts for a small increase.

Gold remains around recent four-month highs of $1280 held back by the opposing forces of a strong USD and safehaven demand from uncertainty surrounding global growth (IMF cuts) what the ECB may or may not announce on Thursday. All eyes on further progress after the metal broke above falling highs from October 2012, the 200-day moving average and completed a bullish flag pattern. Note Daily RSI now overbought after recent rally suggesting potential for a reversal.

Oil has weakened, with Brent back below $50/barrel and US Light <$48 as the US signalled that it will not intervene in the market even as prices decline, China data confirmed the slowest annual economic growth in almost 25 years and the IMF cut global growth forecasts The US-OPEC game of Chicken continues, with Iran saying it can withstand a deeper slump to $25 and OPEC has no plans to slash output. Brent has already broken below its trend of rising support from mid-Jan. Strong USD from ECB QE expectations also hurting.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China GDP Beat, stable

- China Industrial Production Beat, accelerated

- China Retail Sales Beat, accelerated

- Germany Producer Price Inflation Miss, deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Rio Tinto says Q4 global iron ore production (100 percent basis) 79.1 MT, up 12 pct

- Rio Tinto meets 2014 iron ore target, aluminium brightens

- Aggreko appoints WS Atkins CEO to the board

- Dairy Crest says retains Morrisons milk contract

- IQE sees full-year EBITDA 8 pct higher

- Russia's Etalon says Q4 new contract sales up 41 pct

- IG Group says H1 pretax profit up 2.8 pct

- Stock Spirits sees FY results at lower end of forecast

- Balfour Beatty appoints Philip Harrison as chief financial officer