Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

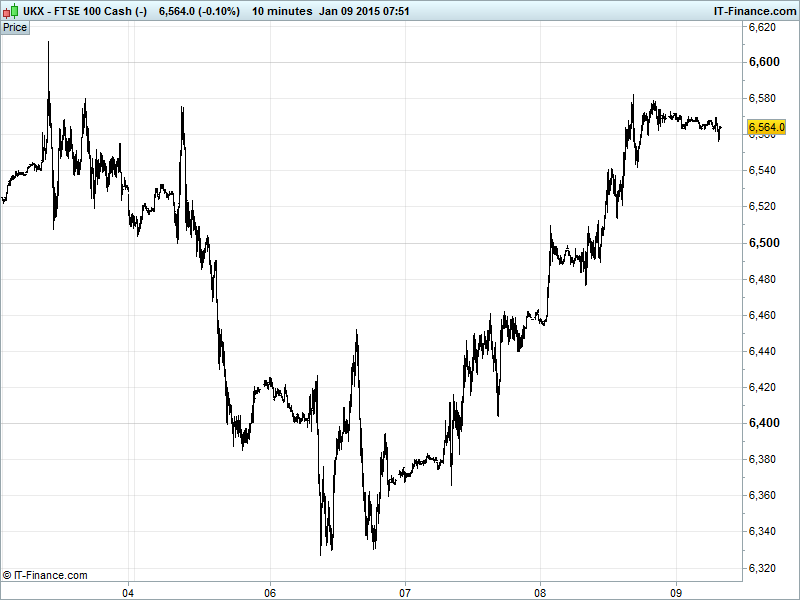

UK 100 Index called to open -5pts at 6565, having paused following completion of the double-bottom reversal pattern highlighted over the last two days, from lows of 6330 and after the breakout at 6450. While good to see more progress falling resistance from early-Dec still a hurdle at week-end, especially if macro data fails to inspire today. Nonetheless, weakness likely to find support at Jan lows 6330 before any full retrace to Oct/Dec lows 6100. Our Watch levels: Bullish 6605, Bearish 6525

The muted opening call comes despite US and European bourses delivering strong gains yesterday following dovish comments from the Fed’s Evans and more supportive comments from the ECB President Draghi regarding possible QE from the central bank, as well as disappointing overnight inflation data from China adding to stimulus hopes for the world’s second largest economy.

Asian bourses positive, but less so than EU/US despite Chinese PPI contraction and CPI improving but still well below target fueling hopes of more stimulus, hindered by a stabilisation/rise in oil price which Japanese economy minister says is good for economy at its current level (net importer) even if it weighs on inflation. More dovish comments from the Fed’s Kocherlakota failed to add to colleague Evans’ boost yesterday.

Japan’s Nikkei hindered by USD/JPY resistance at 120 from more cautious Fed talk about rate rises with exporters failing to build on gains. Australia’s ASX outperforming thanks to Chinese data giving a boost to sentiment with expectations that stimulus will lead to a rise in demand for its raw materials exports.

This morning’s data shows German Industrial Production weaker than expected, adding to the weak Factory Orders yesterday and adding to Eurozone struggles and calls for ECB QE, while the nation’s Trade Balance fell after exports fell and imports rose.

In focus this morning we have UK Industrial and Manufacturing Production seen improving in November. Thereafter it’s all eyes on the first US Jobs report of 2015 with expectations of a normalisation of November’s spike (320K) in Non-Farm payrolls, and reported figure more in-line with Wednesday’s ADP (240K). The unemployment rate is seen falling further adding to jobs progress, and wages growing further, but with inflation still too low it may not be enough to add to expectations of an earlier US rate rise.

Gold settled around $1210, hindered by recent equity market gains (less safehaven demand) and the strong USD (US rate rise expectations, less petro-dollar pressure, global central bank policy divergence), but possibility that merely a pause within technical bullish flag pattern from $1170 lows with upside to $1260.

Oil has found some support off recent lows with US Light Crude $49/barrel and Brent $51 which has helped equities grind higher. Worries still abound on global supply glut fears and hindrance from strong USD. Far from a bear market reversal but some welcome respite helped by hopes of more central bank stimulus (ECB QE PBOC intervention, Fed & BoE rates lower for longer).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Retail Sales Miss, growth slowed

- China Consumer Price Inflation In-line, improved

- China Producer Price Inflation Miss, deteriorated

- Germany Industrial Production Miss, contraction

- Germany Trade Balance Miss, surplus fell

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- XP Power full-year revenue rises 5 pct

- Hilton Food says performed in line with co's expectations

- Speedy Hire names Russell Down as new Finance Director

- Laird says expectations for 2014 remain on track

- SSP Group says Q1 trading in line with expectations

- Restaurant Group FY sales rise, upbeat on outlook

- Fastjet gets Zambia authority nod for phase 1 of AOC application

- Shanta Gold says fire incident at New Luika gold mine

- JKX says successful test results in Elizavetovskoye field well

- Kenya's Centum says to sell insurance firm stake to Old Mutual