Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

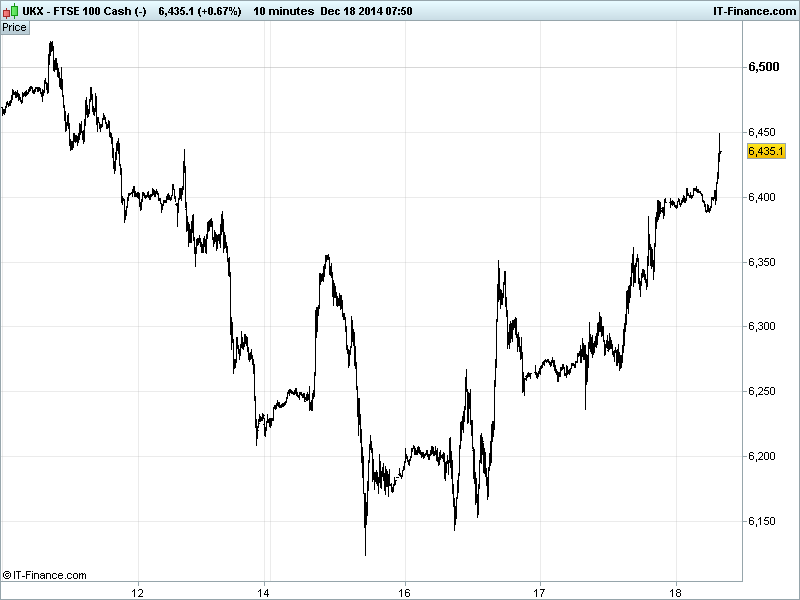

UK 100 Index called to open +90pts at 6425 having broken above the key 6350 level overnight, adding to our theory that a bottom may have been reached following the recent sell-off/correction, supported by rising lows for the index and daily RSI recovering from oversold. Some more progress north of 6400 would be welcome from those hoping Santa is back on track with his end-of year Rally to help regain 6750 or even 6900. Watch levels: Bullish 6450 and Bearish 6340.

The positive opening call comes thanks to US stocks closing sharply higher as markets reacted positively to the latest Fed statement and a recovery in the price of oil from recent lows after US data showed a drop in crude inventories. More negative China property data overnight may have slowed up the overnight rally, but not given it a knock, likely from renewed hopes of China stimulus.

Investors appeased by the Fed retaining its ‘considerable time’ reference to rates staying low and adding a new pledge to be ‘patient’ while normalising policy. But emphasis still made that rates set to rise in 2015, possibly earlier than expected, but unlikely within the first few meetings of the year. So, April/May vs mid-year? Or Fed still just as uncertain and simply updating its ‘rate hike threat’ to curb market enthusiasm?

An upgrade to the Fed’s Labour market assessment added to its optimistic economic picture warranting a 2015 rate hike, although the statement came hot on the heels of disappointing US Consumer Price Inflation (CPI) data which was more negative than expected in November due to the significant drop in oil price, bringing the annual rate further down from the Fed’s 2.0% target.

In Europe, in the first of three votes, only 160 Greek MP’s backed the government presidential candidate dealing a blow to the current administration’s confidence which offsets to some extent the ECB’s Coeure giving one of the clearest signals yet that sovereign bond buying (QE) was on its way next year.

Asian equities in the green overnight, taking the US’ lead with a stronger USD from the Fed statement leading to a weaker JPY, helping Japan’s Nikkei exporters and a recovery in the oil price buoying risk sentiment anew. Note Hong Kong stocks unaffected by China property data delivering extended declines in November, marking it a third straight month of contraction. Are stimulus hopes helping out?

Equities down-under making gains thanks to a weaker AUD following the Fed statement, further progress by resources sector stocks on the back of increases in commodity prices and maybe the weak China property data boosting hopes of stimulus again. Watch the usual London listed mining/oil suspects.

In focus today, we have German IFO Business Surveys seen edging higher and most importantly the Expectations component getting back above 100. UK Retail Sales are expected to show slower growth in November, still hindered by mild weather, but could get a boost from early Christmas shopping.

In the US, Jobless Claims are seen largely flat on the prior week, although continuing claims are seen improving more. US PMI Services is seen edging higher although the Philadelphia Fed Business Outlook is forecast to give up quite a bit of ground in December and the Leading Index to have slowed up its growth in November.

In commodities, Gold still held back by the $1200 level with the Fed statement seeing the USD rally in anticipation of a 2015 rate hike, making the metal more expensive to buy, and disappointing US inflation data (blame the oil price plunge) showing no need for a hedge. The equity rally also negates safehaven demand while risk sentiment gets a boost.

Oil given a boost by a drop US Oil inventories helping the commodity find a bottom after the recent sell-off on supply (US vs OPEC/Russia) and demand concerns (global growth questions). US Light Crude and Brent trading $56 and $61/barrel, respectively, after a spike higher.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Property Prices Deteriorated further

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Balfour completes acquisition of 160 mln stg offshore project

- London Stock Exchange says made good progress in 2014

- Galliford Try wins estates contract with UK ministry of defence

- Riverstone Energy increases stake in Castex

- Lender IPF says Dan O'Connor to succeed retiring chairman

- Crawshaw appoints Noel Collett as chief executive

- Drax appoints new chairman designate

- Astrazeneca's Lynparza gets EU approval

- Synthomer says finance director to retire

- McBride names Rik De Vos as new CEO

- Severfield signs six contracts worth 43 mln stg

- ITM Power sigs second contract with Amec and National Grid

- Hansteen sells 11 UK property assets for 43.9 mln stg

- UK sold Royal Mail too cheaply, but not by much - official report