Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

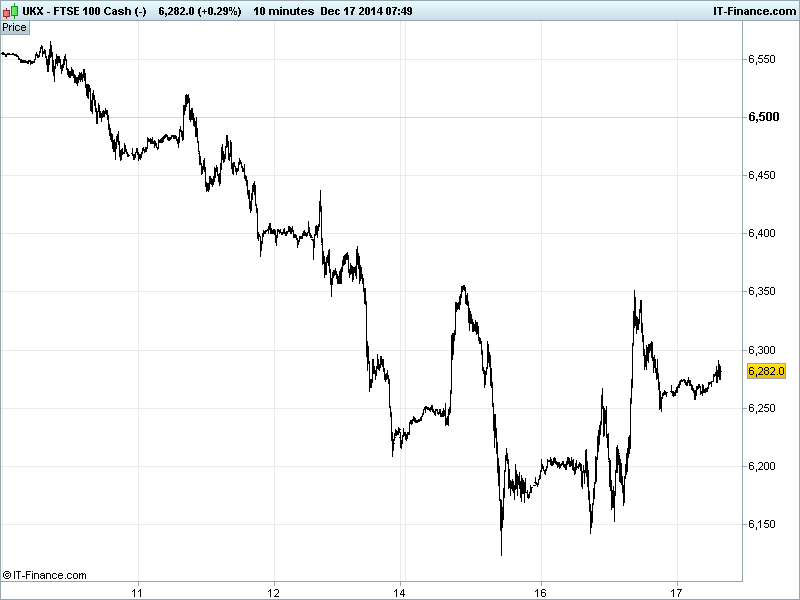

UK 100 Index called to open -50pts at 6280, with resistance around Friday’s highs resulting in a sell-off post the European close, leaving the index well off yesterday’s highs (6355) but also well off its lows (6120) thanks to support around yesterday’s mid-morning highs (6250-60).

Trading activity around 6200 suggests a bottom may have been reached, backed up by rising lows, the daily RSI recovering from oversold (just) and other shorter interval charts showing more RSI progress. It’s still volatile, however, given the myriad concerns the markets face in the run-up to year-end. Updated Watch levels: Bullish 6355 and Bearish 6160.

The negative opening call is courtesy of a weak US close and with much volatility following a strong European finish. This was in reaction to significant moves in the price of oil and ahead of the Fed’s last meeting of 2014 this evening (change of language? ‘Considerable’ to be no more?).

Add to this pre-existing worries related to global growth, Eurozone/Greece, central bank policy uncertainty/divergence, a collapsing oil price (Kuwaiti oil minister says OPEC has no need for another meeting before June) and its effects on the likes of Russia (market turmoil, Rouble plunging, high food process) on which Obama is set to implement new sanctions related to Ukraine.

Major Asian equity indices mixed overnight with some support thanks to the bargain/value hunters following recent weakness, although caution still prominent after the weak US close and ahead of the Fed statement and after Oil suffered from another rise in US inventories (API).

Japan underperforming thanks to worsening in Trade data (exports slowed, imports went negative) weakening the JPY and helping exporters. In Hong Kong, equities down despite a slight improvement in the China MNI Business Indicator, failing to offset the weak manufacturing data yesterday.

Equities down-under posting small gains (ending a six-session losing streak) thanks to recovery in Energy stocks and bargain hunting of heavily resources-focused stocks. As usual, watch those with listing in London (RIO, BLT, AAL).

In focus today, we have UK Employment data for Oct/Nov with the claimant count seen edging the right way along with jobless claims the key unemployment rate and most importantly wages growth remaining above recent inflation for the second month. Has a golden cross of sorts been had after 5 years of struggle?

BoE minutes will be interesting for voting and views on growth worries and inflation given the drop in oil price as will Greece’s vote on a new President which could result in political turmoil (on top of market turmoil) for the recovering nation. In the Eurozone, Consumer Price Inflation (CPI) is expected to be confirmed at 0.3% in November, positive at least although still low enough to see calls for more ECB action soon.

In the US, CPI is seen edging back from the Fed’s 2% target in November, likely due to the drop in Oil price. Whether the Fed statement in the evening sees the FOMC looks through the recent oil price moves remains to be seen. Although it does add to arguments against an earlier rate hike even if employment/growth progress has been made.

In commodities, Gold back holding below $1200 on fears of a hawkish Fed statement which would see the USD rally and make the metal more expensive to buy. Still also hindered by USD resilience, uncertainty towards global central bank policy direction and inflation being missing in action.

Oil not far from its levels of yesterday morning but key is both US Light Crude and Brent below $60/barrel) after Kuwaiti oil minister said no reason for another OPEC meeting before June suggesting no need for intervention.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Merchandise Trade Date Deteriorated

- China MNI Business Indicator Growth accelerated

- Japan Machine Tool Orders Strong growth unchanged

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Babcock confirms acquisition of MoD unit for 140 mln stg

- Monitise says signs deal with business process outsourcing provider

- Saga says trading in line with FY expectations

- Jiasen says knows no reason for share price fall

- Dixons Carphone on track as first half profit jumps 30 pct

- WPP names Quarta as Chairman-designate

- IMI says Roberto Quarta to step down as non-executive chairman

- Man Group to buy Silvermine Capital

- Man Group to buy U.S. leveraged loan manager for up to $70 mln

- Xaar sees FY profit ahead of consensus, keeps 2015 forecast

- Connect announces close of 2 for 7 rights issue