Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

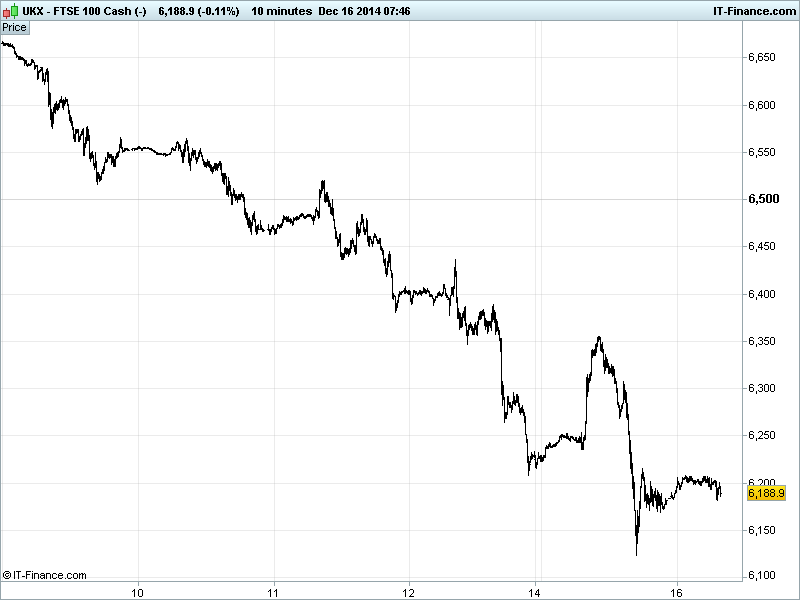

UK 100 Index called to open +8pts at 6190 having recovered from lows of 6124 overnight but demonstrating the volatility still in play and potential for a full retracement of the October/November rally as we have repeatedly highlighted amid recent global growth worries, Eurozone/Greek uncertainty, central bank policy divergence and collapsing oil prices. Updated Watch levels: Bullish 6255 and Bearish 6120.

The tepid opening call comes after a negative close for both European and US equities (blame weak US data) yesterday as the global rout continues amid much uncertainty including disappointing overnight China PMI Manufacturing (worse contraction), apprehension ahead of the Fed meeting this week and the oil price sinking further to fresh 5yr lows.

Note little boost for/from UK banks (well, all but the Co-op) getting a clean bill of health from the BoE stress test results this morning, apparently able to withstand a sharp fall in house prices. RBS and LLOY only scraped through thanks to taking measures to boost their balance sheet in advance. Still, another hurdle out of the way.

Major Asian equity indices in the red overnight after taking the lead from the US close but also weighed by further heavy losses by commodities and commodity-focused stocks after Chinese PMI Manufacturing fell to a 7-month low and posted worse contraction than expected adding to calls for more stimulus on fears of global growth faltering. No solace sought in a rebound in Chinese Foreign Direct Investment.

Japan underperforming in the region after the USD gave up some ground and resultant stronger JPY hurt exporters, with little help from a slight improvement in the nation’s PMI Manufacturing. Equities down-under in the red, but outperforming despite commodities hurting with Energy and Mining weighing. Watch those with a London dual-listing at the open (RIO, BLT, AAL).

In focus today, we have the fall-out from the BoE UK Bank stress tests results. Later watch out for PMI Manufacturing & Services from France and Germany, with the former seen staying in contraction but the latter recovering some ground to the benefit of the Eurozone as a whole, keeping its head above water at this difficult time.

UK Consumer Price Inflation (CPI) is expected flat in November, highlighting difficult decision for the BoE in terms of timing a rate hike in 2015. Will inflation recover with Oil having fallen so low? Germany’s ZEW Surveys are seen improving in December adding some year0end hope to the region’s industrial drivetrain.

In the afternoon, while US PMI Manufacturing is expected to edge higher, Housing Starts and Building Permits are seen at odds in November, both recovering and dropping after respective weakness and strength in October.

In commodities, Gold off its lows of $1190 but remains held back by the round $1200 marker, hindered by USD resilience, uncertainty towards central bank policy trajectory (Fed meeting this week) and absent inflation it usually hedges against as well as some questioning whether or not the yellow metal still represents safehaven port in a storm.

Oil at fresh 5yr lows (US Light Crude down to $55/barrel; Brent to $60/barrel) after the UAE Oil minister said his country was not targeting a specific oil price and that OPEC will not hold an emergency meeting unless something drastic happens.

Hold onto your hats? Worse to come? Could Oil fall below $40/barrel as it did in late 2008/early 2009 amid the sharper financial crisis correction? Russia’s obviously worried OPEC producers hold their ground hence its hike in interest rates (to 17% from 10.5%) to combat the 13% slump in the Rouble.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan PMI Manufacturing Growth Improved slightly

- China PMI Manufacturing Miss, Contraction worsened

- China Foreign Direct Investment Beat, Bigger rebound

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Vodafone to get C$850 mln Canada finance, mainly for BlackBerry

- Barclays above threshold in BoE stress test

- Lloyds Banking Group - GROUP EXCEEDS PRA STRESS TEST THRESHOLD

- Optimal Payments sees FY results at least in line with expectations

- Domino Printing Sciences says remain cautious about 2015

- UK regulator approves funding for SSE's Scottish subsea link

- Hargreaves Services initiates share buyback

- Rockhopper delays Falklands oil project sanction to mid-2016

- RBS says still work to be done on balance sheet

- 888 confident of meeting FY adjusted core profit expectations

- Gulf Keystone says on target for production increase at Shaikan oil field

- IHG agrees $430 mln acquisition of boutique Kimpton Hotels

- Imagination Tech sees better H2 after interim profit fall