Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

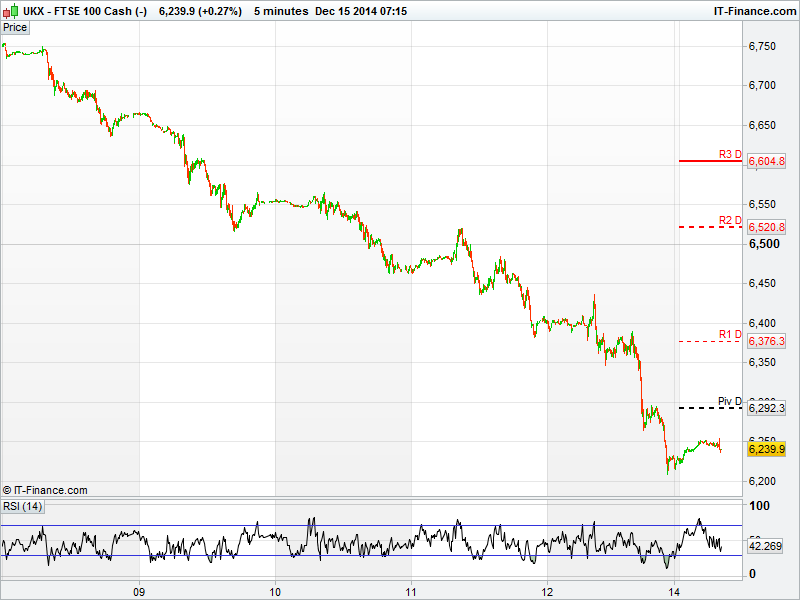

The UK 100 Index is set to open lower by 50pts at 6250pts having traded as low as 6205pts in the small hours.

Friday's spectacular capitulation saw UK equities finally came to rest after 161pts to close at 6300pts - saved by the closing bell - capping the worst week in three years.

A combination of weaker Chinese data, falling oil prices and a struggling Eurozone encouraged traders to continue selling.

Disappointing factory data supported trader's concerns for the world's second largest economy whilst oil prices continued to slump, U.S. light crude now trading at $58, below $60 for the first time in five years.

Eurozone fears were reignited on talks of a Greek exit from Europe (Grexit), prompting the biggest one-day decline on the Athens Stock Exchange since 1987, last week. 10 year government bond yields rocketed to 9%.

Only defensive stocks provided some shelter on Friday, with the likes of United Utilities (UU.L), SSE (SSE.L) and Shire (SHP.L) among the best performers.

Expect more of the same today - equities are set to start on the back foot with few reasons to buy currently.

Looking forward - tomorrow will see the UK government publish the results of the UK banking stress tests meaning the likes of Barclays (BARC.L), Lloyds Banking Group (LLOY.L) and Royal Bank of Scotland (RBS.L) will be in focus for the next 24 hours at least.

US Markets finished with heavy losses, as the Dow Jones was down by over 300pts to 17,280 (-1.8%), and the S&P 500 down 33pts to 2002 (-1.6%), as the slide in oil prices continued with the IEA earlier cutting oil demand forecast. The US posted their biggest weekly fall in 2 -1/2 years similar to the UK markets led by the energy sector and some expecting the Fed to increase rates sooner rather than later.

Asian markets were broadly lower with the Nikkei the worst performer down 270pts to 17,100 (-1.6%) despite PM Abe’s big victory on Sunday. The Hang Seng was down 1% whilst the ASX fared slightly better to finish lower by 0.6% as concerns that a plunging oil price signals weakness for global growth. The recent slump in global markets has caused nearly $2 trillion to be erased from the value of equities.

In commodities the decline in oil was the main factor for the global market sell-off. WTI fell 12% last week alone to hit a 5 year low as OPEC continues to resist from cutting output. Some speculating that even a price of $40 wouldn’t cause OPEC to cut production. Expect a rebound but will this be long lived? Gold remained steady trading at the $1220 handle whilst silver dropped slightly.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Tankan Large Manufacturing Index Worse

- UK Rightmove House Prices (MOM) Decline

- UK New Motor Vehicle Sales (MOM) Improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- IGAS preliminary results at Ellesmere Port well show 1,400 feet of shale

- Leni Gas and Oil's well in Trinidad flows at 1085 bopd

- Greggs says to beat year profit expectations

- UK's Carpetright sees FY profit toward top end of forecasts