Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

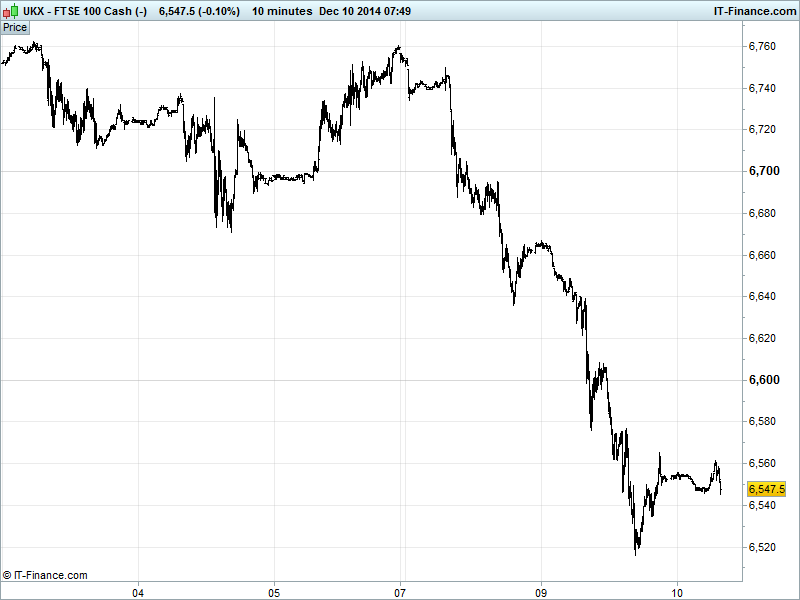

UK 100 Index called to open +20pts at 6550, having regained the 6550 level and 50-day moving average after a near test of 6500 yesterday on global growth concerns. Watch for abandoned support at 6650 for potential resistance to revisiting recent highs of 6750. The possibility for further retracement of Oct/Nov rally remains, with momentum having dropped. Watch levels: Bullish 6590 and Bearish 6510.

The positive opening call stems from a strong recovery by US equities from day-lows thanks to solid US data coupled with overnight Chinese Inflation data (CPI, PPI; multiyear lows) increasing deflationary fears and adding to global growth worries but reviving hopes of more stimulus being forthcoming from the government/PBOC to help kick-start inflation/GDP, offsetting yesterday’s fears of tighter Chinese lending rules crimping growth.

US equities ended the day mixed, pretty much breakeven, recovering from significant weakness, this following a very weak close by European equities (down 2 to 3%) on Greek political unrest (risk of snap elections), volatile oil prices (gains from short covering?) and the wider global growth worry sell-off.

China CPI data helped Shanghai equities overnight, recovering some of the prior day’s significant losses, giving Hong Kong a boost, although Japan’s Nikkei still weighed by recent weak Asia/Europe data denting sentiment, a weaker USD and thus stronger JPY this week, upcoming elections, and its own Consumer Confidence deteriorating for a third straight month to the worst level since April.

Downunder, Australia closed bloodied by 0.5% but outperforming Japan thanks to China stimulus hopes (Miners benefiting) and rebound in Home Loans, but held back by drop in Consumer Sentiment (lowest level since Aug 2011), heightening speculation that the RBA will need to cut rates again next year.

In focus today, we have UK Trade Balance data expected to show minor improvements in deficits, although after Chinese and German numbers this week the focus will likely be more towards exports and imports growth for signals as to global economic health/demand.

In commodities, Gold at month highs of $1238 on increased safehaven demand amid the equity sell-off, and helped by a weaker USD this week. Oil volatile on potential short covering of bearish bets, but continued pressure from global production/demand mis-match and Iran talking of a slump to $40/barrel if there is discord at OPEC.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Home Loans Beat, growth rebounded

- Australia Investment Lending Growth slowed

- China Consumer Price Inflation Miss, growth deteriorated

- Japan Consumer Confidence Miss, deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Hochschild Mining changes chairman's role, board fees

- BG Group agrees sale of Australian pipeline for US$5 billion

- Glencore says will continue to focus on capital return

- PZ Cussons says half-year sales in Nigeria declined due to disruptions

- Plus-size retailer N Brown says trading improves since Sept

- Micro Focus Intl first-half pretax profit dips

- StanChart extends sanctions compliance deal with U.S. authorities

- Serco signs contract with Australia worth A$1.9 bln

- Carillion sees similar revenue growth in 2014

- Kenmare Resources comments on share price movement

- Stagecoach says on track to meet FY expectations

- Ashtead lifts full-year expectations after profit surge

- Fastnet Oil & Gas appoints Carol Law chief executive

- Sirius Minerals promotes Thomas Staley as CFO

- Qatar's bid for Canary Wharf-owner Songbird wins more support

- Rolls-Royce initiates share buyback programme