Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

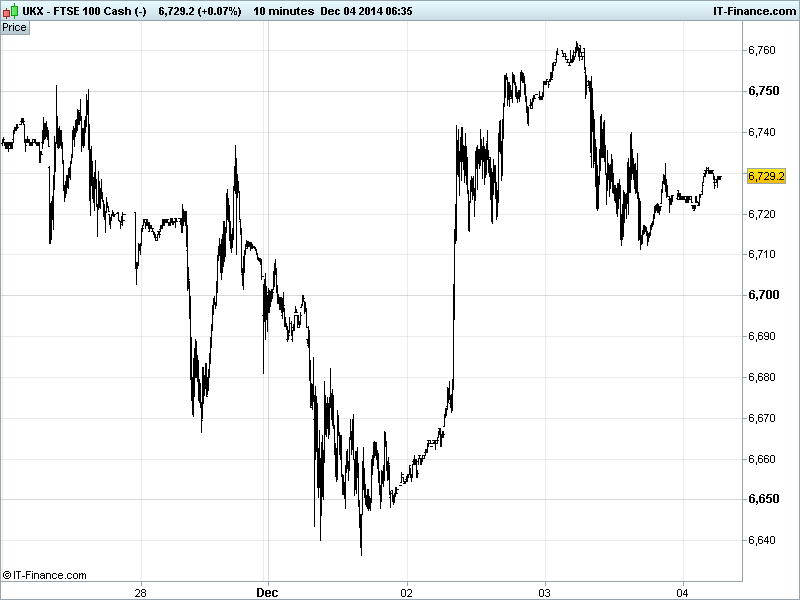

UK 100 Index called to open +10pts at 6735, with momentum having cooled as suggested yesterday ahead of the ECB Policy update this afternoon (prep for QE? Expectations are highs) and US Jobs report on Friday. It was healthy to see that 6700 wasn’t revisited with support emerging around 6710/20, however, there is still a risk of markets being disappointed by ECB inaction/delay today. Watch levels: Bullish 6780 and Bearish 6690.

Positive opening call comes courtesy of US bourses posting gains, maintaining December uptrend (S&P 500 back near highs, Dow Jones there already), after the Fed’s Beige book economic assessment suggested activity continuing to expand in October and November with widespread job gains across the US, even if price and wage growth was subdued and the lower oil price was a concern for the industry.

Data-wise, US ADP job adds (Non-Farms warm-up) disappointed, however, US PMI Services was solid, US ISM Non-Manufacturing beat (although jobs component fell) and US Crude inventories fell, tempering concerns that a global supply glut would worsen after OPEC held output

Hawkish rhetoric from the Fed’s Plosser helped the USD even higher (strongest since 2007), saying rates near zero, inflation close to target and almost full unemployment was unprecedented and risky waiting too long to raise rates, while colleague Fischer said rate rise depends on jobs and inflation and Fed should start trimming balance sheet while removal of ‘considerable’ time language is next logical step and closer to rate rise than expected.

Stocks in Asia positive overnight with Japan’s Nikkei still getting a boost from a weak JPY (combination of USD strength and Sales tax delay/election announcement) and the BoJ’s Sato changing his mind and now in favour of more QE, saying that lower oil price will exert positive economic effects. Downunder, Australia’s ASX helped by a weak AUD despite better than expected retail sales data and a smaller trade deficit. Hong Kong’s Hang Seng benefiting from Chinese shares surging for a third day

The main events today will be policy updates from the BoE and ECB and while no changes are expected, there will be much focus on ECB President Draghi’s press conference as it may - many hope - include stronger hints/commitment for further stimulus (QE) in 2015 to combat deflationary/recessionary risk. If not, markets may be disappointed. As for the BoE, we’ll have to wait for MPC minutes later in the month to find out today’s updated voting split on a rate rise.

In commodities, Gold is holding around $1200, held back from recent $1220 highs by the prospect of a solid US jobs report boosting the case for a US rate rise and thus strengthening the USD, curbing demand for the metal just before the ECB meets to consider more stimulus (potentially weakening the EUR and adding to existing USD strength).

After Oil’s rebound soured, and the USD resumed its upward march, the WSJ reported that Saudi Arabia believe oil prices could stabilize around $60/barrel, according to people familiar with the situation, with Gulf states having to adapt to the rapid fall. This implies more downside from current levels of $68 for US Light Crude and $70 for Brent. Note little weakness from yesterday, with Support emerging thanks to news of drop in US inventories

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Retail Sales Beat, Not as slow

- AU Trade Balance Beat, Smaller deficit

- FR Unemployment Miss, grew

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Mulberry sees signs of improvement after first half loss

- UK pub firm Greene King sees first half profits fall

- Russia's Polymetal declares special dividend of $0.20 per share

- Carillion wins Heathrow, Barts contracts worth 80 mln stg

- Sky sells controlling stake in Sky Bet to CVC for $1.3 bln

- Robert Walters sees FY profit ahead of market expectations

- Nighthawk Energy announces new hedging program

- Numis full – year profit jumps 22 percent on London IPO surge

- DS Smith H1 reported revenue falls 5 pct

- Easyjet passengers up 3.1 percent in November

- AG Barr says on track for full year expectations

- Pets at Home pays first dividend after earnings rise in first half

- TUI Travel annual profit rises 11 pct, beating forecasts

- BTG to acquire Pneumrx for up to $245 mln, funded by placing

- Asset managers to invest 9 billion pounds in UK private placements