Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

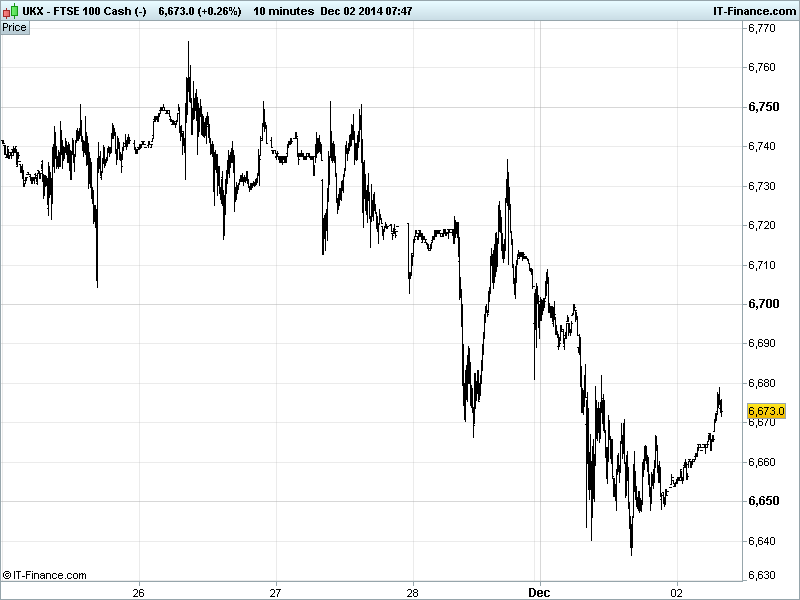

UK 100 Index called to open +20pts at 6675, having found support at late October lows 6640 following a foray south as momentum continued to wane from recent highs on a combination of profit-taking and renewed commodity price weakness. All eyes now on whether this holds as a base for a recovery, or is breached to the downside opening the gates for further falls. Watch levels: Bullish 6740 and Bearish 6630.

The positive opening call stems from US bourses recovering from their lows thanks to a rebound in commodities (short covering, bargain hunting, weaker USD on stateside growth/monetary policy outlook) after a sharp drop in tech favourite Apple (AAPL), a ratings cut for retailer Amazon (AMZN), some weak macro data (PMI Manufacturing, ISM Prices paid at 2yr low) and the Fed’s Dudley suggesting a mid-2015 US rate rise.

Overnight, Asian stocks mostly higher as investors ignore ratings agency Moody’s downgrade for Japan and S&P’s doubts (although traditional safehaven JPY was seeing in demand, weakening USD and thus helping Gold) and are taking heart from the bounce in the oil price and relief rally in commodities as well as speculation that the Chinese Central Bank will increase stimulus.

In Australia, equities benefiting from the rebound in Oil and energy stocks and a weaker AUD despite a stronger current account balance and building approvals (rebound) and the RBA leaving rates unchanged after commodity price declines which are sure to dent the nation’s natural resources exporters.

In focus today, UK PMI Construction is seen stable around 61 in November while Eurozone Producer Prices are expected to be negative in October, highlighting the region’s deflationary risk and potential need for more stimulus (Q-ECB).

In the afternoon, Fed Chair Yellen speaks which could move the USD and thus commodity prices. The reading for ISM New York is also seen stable in November, while US Construction Spending is forecast to have rebounded in October.

In commodities, Gold has delivered its biggest rebound in a year to above $1200 amid a commodity relief rally which saw the metal jump from lows of $1140 to highs of $1220, helped by the USD weakening from highs (makes commodities cheaper) and an element of short covering and bargaining hunting kicked in while investors continue to weigh the outlook for an stronger USD and expectations of Fed rate rises next year.

Oil has recovered some ground with US Light Crude back at $68.5/barrel and Brent at $72 as hopes of continued central bank stimulus and oil production coming more in-line with demand being married up with some interest in the black stuff at these low prices and short-sellers calling it a day.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Current Account Beat, Lower deficit

- AU Building Approvals Beat, Stronger rebound

- AU Interest Rates In-line, unchanged

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Aviva agrees Friends Life Group offer

- Mccoll's year – to – date total sales rise 4.2 pct

- Lufthansa pilot strike extends to long – haul, cargo flights

- Centrica makes Norwegian Sea gas discovery – partners

- Kier Group says new Finance Director to take over from Jan 1

- Genel, partners receive first oil export payments from KRG

- ITE says FY revenue down, results hurt by Ukraine upheaval

- Merlin Entertainments confident after strong post-summer trading

- Fastjet says benefitting from fall in crude oil price

- Kitchen supplier Howden Joinery posts record 1 bln stg UK sales

- Northgate first-half pretax profit rises 70 pct