Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

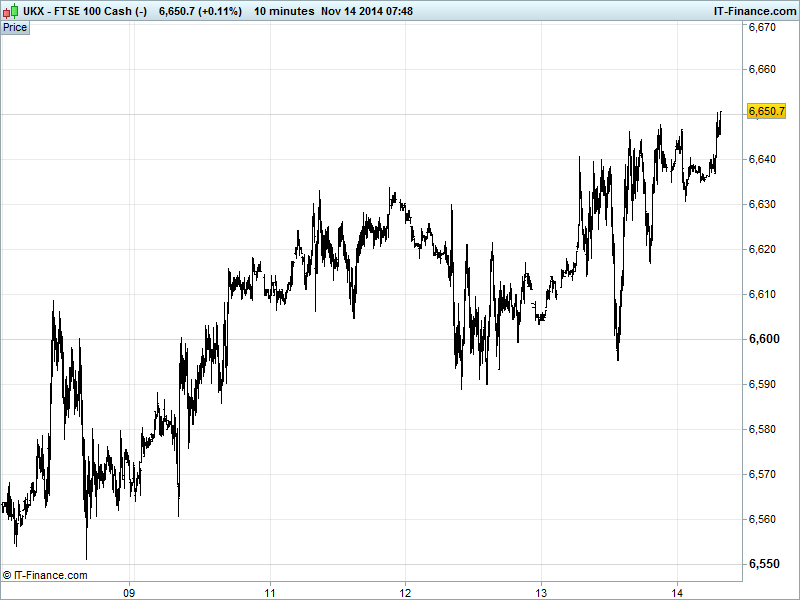

UK 100 Index called to open +10pts at 6645, testing yesterday’s highs thanks to French and German GDP data this morning showing the former rebounding and the latter avoidance technical recession (two consecutive quarters of contraction), providing some relief regarding the woes of the struggling region.

Positive is the UK index still trading above 6600, in a rising recovery trend from October lows even after a test of 6595 yesterday. Nonetheless, the narrowing rising wedge pattern persists which could still break down. Bulls still eyeing September highs 6900. Our watch levels: bullish 6655 and bearish 6615.

US markets again closed positive-to-breakeven after wavering around new record highs as the oil price fell even further despite a drawdown in US inventories. With data limited to Jobless claims/openings (stable), Fed speakers saw Plosser said inflation not going to get much higher in the near-term nor that more QE would help, while ratings agency S&P expects strong US growth through year-end, with Fed rate hike in Q2 2015.

Asian markets positive, taking US lead with USD strength weakening Asian currencies sending the Nikkei to a fresh 7yr high helped also by continued speculation about an election and Finance Minister Aso saying economic indicators improving, but private consumption stalling. Nonetheless, gains muted with a pause ahead of Japanese GDP next week, and after strong Chinese gains before the new trading link goes live.

Geopolitics not something to ignore ahead of the weekend, with reports that thousands of Russian troops have crossed into Eastern Ukraine over the last few days and ahead of the G20 meeting in Australia where Putin will be forced to sit with Western leaders.

In focus today after major contributors France and Germany’s positive start, will be the Eurozone GDP print which could be better than expected, although weakness elsewhere (Italy etc) could still hamper progress. With growth one thing and prices another, all eyes on the accompanying inflation data and whether it continues to flirt with deflation.

In the afternoon, US Retail Sales are expected to have rebounded in October while US equities trading ever higher and reduced fuel prices are expected to be backed up by Uni of Michigan Consumer Confidence showing another advance to another 7yr high, and US Business Inventories are seen printing stable growth.

In commodities, Gold stuck around $1160, equidistant from recent highs and lows as the USD strength hampers buying power while equity gains/energy price falls dent safehaven demand and investors discuss monetary policy direction the world over.

Oil is headed for its longest weekly drop since 1986 on speculation OPEC will refrain from cutting production to counter rising supply and waning demand. US Light Crude down to $73/barrel while Brent Crude is sub-$77.0/barrel. This even after the US bucked a six week trend of rising inventories.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- FR GDP Beat, avoids recession

- DE GDP In-line, avoids recession

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Glencore to shut Australia coal mines for 3 weeks amid glut

- Aggreko reaffirms underlying full year profit guidance

- Genus says trading in line with expectations

- Fastjet in talks over new funding, moves closer to Zambia launch

- Premier Farnell sees FY operating margin slightly below prior year

- Balfour sells some German rail assets

- Egdon buys out minority partner on Yorkshire gas licence

- Gemfields reports small fall in emeralds production

- IMI sees hydronic engineering to deliver H2 organic growth in line with H1

- IMI buys Bopp & Reuther for 152.6 mln euros

- Sainsbury's launches 400 mln stg convertible bond offer

- IGas confirms detail of CEO's arrangement with Energy First

- Rotork says Q3 order intake up 4.3 pct