Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to open -10pts at 6640, making it a 5th cautious opening call in a row, as London equities ignore the US rally and positive finish on Friday and following the negative lead from Asia-Pacific which has been dented by pro-democracy protests in Hong Kong and soft industrial profits growth data from China over the weekend – keeping geopolitical risk and slowing global growth to the fore for the new week.

US markets closed sharply higher on Friday after upward US Q2 GDP revisions and solid Uni Of Michigan Consumer Confidence offered signs of the US economy gaining steam, seeing the USD maintain its uptrend and potentially justifying the Fed increase in borrowing costs that looms large on the horizon.

Overnight, Asian equities in the red with risk sentiment hampered by an escalation in pro-democracy protests in Hong Kong seeing the Hang Seng erase gains, while banks and miners in Australia are suffering on the back of disappointing data out of China. The standout performer is the Nikkei which has the strong USD to thank for weakening the JPY and helping its exporters.

After Friday’s big news that Bill Gross was leaving PIMCO after 40yrs, note the Bond house seeing China’s GDP growth slowing to 6.5% from 7.5% and sees Australia’s GDP growth 2.5% to 3%, with downside risks. It also sees China rate cuts and continued Japanese easing. Note the China Securities journal reporting China may have targeted measures amid slower growth, while the PBOC said 6.7% growth can meet 2020 goal.

In focus today we have a decent slate of data with UK Consumer Borrowing and Mortgage Approvals, both seen a touch lower in August in-line with seasonality and recent property market surveys. Eurozone Confidence surveys are also seen a little weaker in September which supports recent uncertainty about growth in the region and the plans of the ECB to kick-start growth and stave off deflation.

In the afternoon, Eurozone powerhouse Germany’s Consumer Price Inflation is seen going negative again in September which may be regarded as putting the ECB under more pressure to look at something more akin to QE. After the positive US data of Friday, US Personal Income is seen posting more growth in August while Spending (70% GDP) is seen rebounding. After Existing Home sales disappointed last week while New Home Sales surprised to the upside, US Pending Home Sales are seen dropping in August.

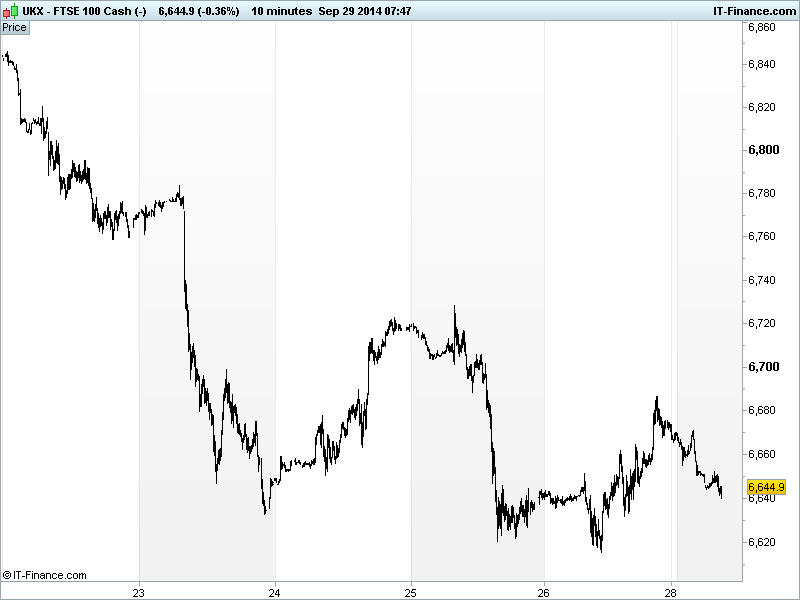

The UK 100 index has fallen back to 6650 overnight, after a brief Friday rally alongside US bourses failed to regain 6700 and soft Chinese data sapped risk appetite. This maintains the downtrend from highs of 6900 on 19 Sept and suggests, as discussed last week, that further declines could materialise leading to a revisit of the lows of 6500-6550 from August, completing the second half of what is known as a bearish flagpole pattern. Watch levels: a break below last week’s support at 6615 and a break above falling resistance at 6680.

In commodities, Gold has settled around $1218, after its Thursday rally to $1225 was wiped out on Friday when equities rallied on positive US data which is supportive of higher borrowing costs, the prospect of which has brought the metal near 4yr lows. The stronger USD (on improving US economy) is also making the safehaven relatively more expensive. The metal looks set for its first quarterly loss this year.

In Oil, US Light Crude has fallen back from highs of near $94 (highest in 7 days) following a Friday boost from US data, as concerns eased over supply disruption in the Middle East. Note its discount to Brent Crude is at its smallest in a year as ample supply offsets the global market from military intervention against the Islamic state (note UK parliament voting in favour of participation in airstrikes).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN Industrial Profits growth Dropped negative

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Quindell confirms that it knows no reason for recent share price falls

- Borders and Southern Petroleum posts H1 loss of $0.9 mln

- Workspace sells industrial estates for 44 mln stg

- London Mining says in talks with potential strategic investor

- Diploma expects 6 pct rise in full-year revenue

- JKX Oil & Gas says awarded 20-year production licence for Elizavetovskoye field

- Construction losses force Balfour Beatty to warn on profit again

- Morgan Advanced Materials CEO to step down

- BAE Systems says 2014 outlook unchanged

- Aberdeen Asset Management gets asset boost, sees outflows slow

- SSE continues to expect 2014/15 earnings to be slightly more than last yr