Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

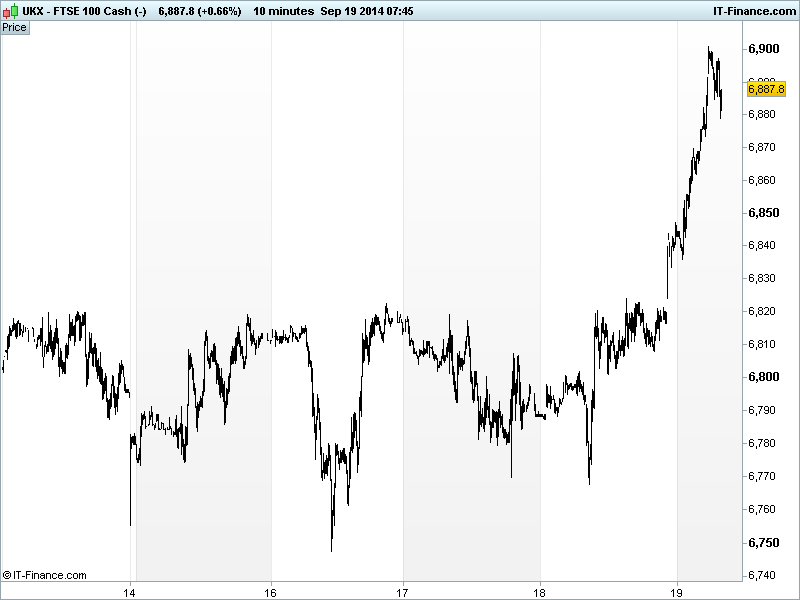

UK 100 called to open +65pts at 6885 thanks to Scotland voting against independence thus removing the dominant uncertainty which had dogged the index lately regarding what would happen vis-a-vis Scottish companies, stocks with exposure north of the border and of course the country’s use of GBP.

This comes on top of already revived risk appetite linked to loose monetary policy for longer from the Fed, ECB and BoJ after their recent communications/action, with the Fed staying dovish, poor TLTRO take-up possibly meaning the ECB has to do more and Japanese PM Abe saying Abenomics part II on its way.

The combined result was index futures rallying hard with Japan’s Nikkei jumping to its highest level since 2007 after the nation revised down its economic assessment for the first time in 5 months (more stimulus?) and a weaker JPY helped exporters.

Elsewhere in Asia, shares benefited from more liquidity boosting measures in China after the PBOC cut a key interest rate to ease banks’ short-term borrowing costs, which follows am already significant injection into 5 major banks and another signal of an easing bias to kick start the world’s #2 economy.

US stocks closed higher with the DJIA and S&P500 closing at new record highs (DJIA >17300, S&P > 2000), with banks performing strongly on sentiment towards central banks, airlines benefiting from the price of oil continuing to fall back and interest in technology names returning.

Note e-commerce giant Alibaba has priced its US IPO today at $68/share, at the top end of the expected range, in which is one of the world’s largest ever public offerings, raising $21.8bn and making the company worth $168bn (more than Amazon’s current $150bn).

In focus today will be the fall-out form the Scottish referendum result, not just in the UK but elsewhere in Europe given the appetite for autonomy from regions such as Flanders in Northern Belgium, Padania in Northern Italy and of course Catalonia in Northern Spain. Relief there too? Data wise the calendar is limited to the US Leading Index in the afternoon.

The UK 100 made a decisive breakout from its September downtrend thanks to the Scottish ‘No’ vote, with the relief rally taking it back just shy of the 4 Sept highs (6901 vs 6905). Off its best levels, this could mean resistance around 6900 after a busy weak, however, with a handful of risk events now out of the way there could also be an argument for further advances thanks to those previously on the side-lines looking to get back involved.

In commodities, Gold remains around its 8-month low as the Fed hiked its interest rate forecasts reducing inflation expectations, the stronger USD makes the metal more expensive and the removal of some prominent risk events saps demand for the safehaven.

In Oil, US Light and Brent crude look headed for their first weekly gain this month on speculation that OPEC is considering cutting its production target next year, despite it being a roller-coaster week with US Light now well off its recent lows but Brent remaining their on depressed sentiment towards economic demand.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- SCO Scottish Independence Vote ‘No’ camp wins: 55% vs 45%

- JP All Industry Activity Index Miss, deteriorated

- JP Leading Index Deteriorated

- JP Coincident Index Stable

- JP Dept Store Sales Weak, but less so

- DE Producer Price Inflation Weak, stable

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Evraz says considering IPO of Evraz North America

- Rockhopper not paying contingent consideration in MOG deal

- Domino Printing Sciences says sales in ten months to August rise 4 pct

- African Minerals sees no material impact of Ebola lockdown in Sierra Leone

- WPP to acquire Creative and Research Agency from MCS Holding in Mongolia

- Just Eat to merge its Brazilain business with iFood