Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

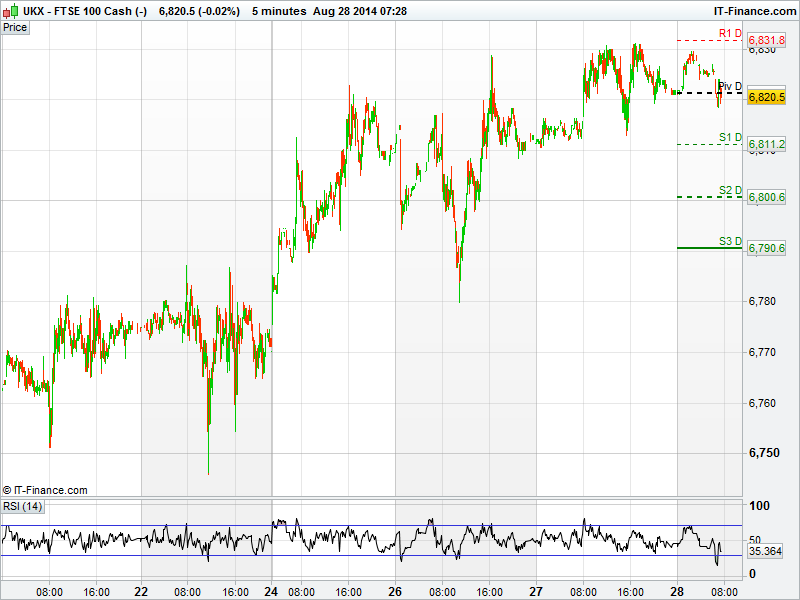

The UK 100 Index is called to open lower by 5pts at 6823, as the market plateaus close to 2014 highs.

The UK 100 tentatively added 8pts yesterday as traders pause for breath having fully recovered the 300pt 'mini-crash' of three weeks ago. More impressively the U.S. indices, namely the Dow Jones and S&P 500, have recovered and gone on to reach the highest levels ever recorded.

The best performing stocks of the day included Petrofac (PFC.L), shares closed higher by 2.32% on a trading update. The first half saw profits decline 44% but the company maintained its full year profit forecast which went some way to reassuring traders.

Fresnillo (FRES.L) and Randgold Resources (RRS.L) gained 1.75% and 0.73% as the price of gold firmed to $1286.

International Consolidated Airlines (IAG.L) and EasyJet (EZJ.L) continued to climb, shares up 1.54% and 1.18%. In the just three weeks the shares have risen 18% and 14% respectively.

Supermarkets came into focus as market research company Kantar published its latest findings. WM Morrison (MRW.L) jumped 1.43% as data confirmed the company had lost market share but to a lesser extent than expected, while Tesco (TSCO.L) shares fell 1.11% and Sainsbury's (SBRY.L) plunged 2.59% (the worst performer on the UK 100 ) as discounters Aldi and Lidl pinched some of their customers.

U.S. markets followed Europe's lead in registering a lacklustre session. The Dow Jones closed higher by just 15pts while the S&P 500 closed a fraction higher on the day at 2000pts. With record highs recently registered in both cases, traders are reluctant to sell in fear of missing out on further gains, yet are apprehensive to buy 'at the top'.

Economic data from the world's largest economy could provide the catalyst for a move either way - U.S. Preliminary GDP data is due today at 13:30 GMT along with weekly unemployment claims and pending home sales data at 15:00 GMT. Tomorrow will also see PMI and personal income data published. Watch this space.

Asian markets registered shallow losses as a stronger Yen impacted the share prices of Japanese exporters, while the MSCI Asia Pacific Index triggered profit taking after closing in on a six year high.

In commodities, with tensions in Ukraine still the focal point, gold picked up slightly to $1287 as traders were weary of escalating violence in Donetsk. In industrial metals copper fell to week lows after Chinese industrial profit growth slowed to 13.5% from 17.9%.

WTI fell for the first time in three days to $93.50 a barrel as crude stockpiles increased in the US. Brent remained steady. In FX the euro recovered from lowest levels in a year after German finance minister Schaeuble said Draghi’s comments on Friday were “over-interpreted”.

In focus today we have German unemployment rate released at 8:55am and German CPI at 13:00 both expected to come in unchanged. In the US we have GDP data released at 13:30, expected to decline slightly to 3.9%, followed by pending home sales at 15:00.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU HIA New Home Sales Declined

- CH Industrial Profits Declined

- AU Private Capital Expenditure Declined

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Glencore in talks to mine huge Australian bauxite deposit

- Eurasia Drilling warns of sanctions impact in Russia, profit declines

- Gulf of Mexico drilling activity drives Hunting's first – half profit

- Lamprell churns bigger profit as projects complete ahead of budget

- Russia's Petropavlovsk says H1 net loss narrowed y/y

- BP says Whiting refinery still in production after fire

- Oxford Biomedica H1 rev 4.7 mln pounds