Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

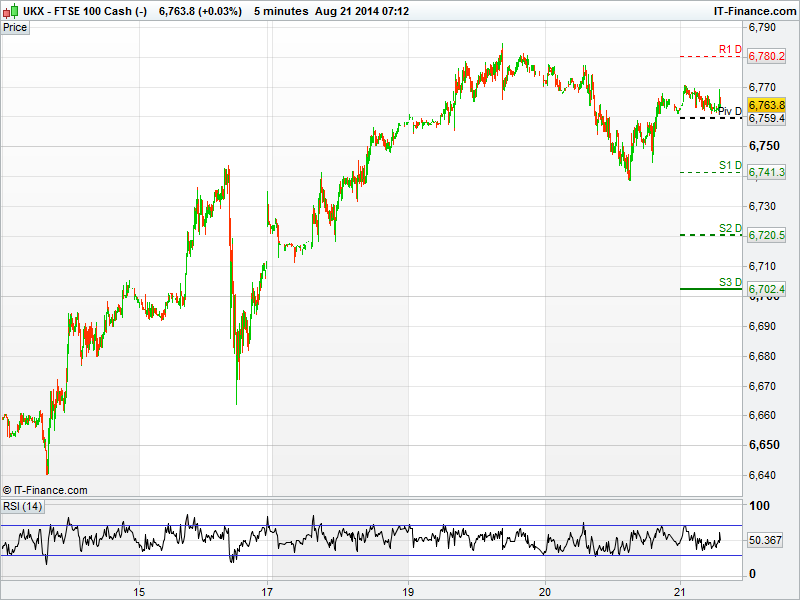

UK 100 Index is called to open lower by 8pts at 6763, after declining 24pts yesterday ending a five day winning streak.

Traders took risk off the table ahead of Bank of England minutes which showed two members of the monetary policy committee voted for an increase in interest rates.

House builders were among the heaviest declining stocks yesterday as traders feared an increase in the cost of borrowing. Barratt Developments (BDEV.L) lost 2.44% to 359.60p and Persimmon (PSN.L) fell 2.00%.

Supplier to the building industry CRH (CRH.L) fell the most, down 3.85%. In addition to the BoE comments that spooked the house builder sector, the company released its first half trading statement detailing a 4% increase in sales that failed to impress.

Stocks with defensive qualities were favourable among traders with United Utilities (UU..L), SSE (SSE.L), National Grid (NG..L), Centrica (CNA.L) and Severn Trent (SVT.L) up as much as 1.5%.

AstraZeneca (AZN.L) closed higher by 1.10% as traders tentatively moved in ahead of August 26th, when under UK takeover rules, U.S. drug giant Pfizer can make the first steps toward a renewed bid.

U.S. stocks advanced for a third day, the S&P 500 Index came within 2pts of a record level while the Dow Jones closed higher by 60pts having peaked at 16,995pts as minutes indicated the Federal Reserve will continue to support the economy.

Asian Markets endured a mixed session. Gains in Japan and Australia were offset by losses in China as after manufacturing data from the world's second largest economy fell short of expectations - 50.3 versus 51.5 for August bringing into question the strength of the Chinese economy.

In commodities, gold fell for a fifth day trading as low as $1280, on course for its longest slump since June, as minutes from the Fed showed borrowing cost may increase earlier than expected. Platinum meanwhile was headed for its longest losing run in 27 years. Brent Crude fell back to $102 and WTI down to $93.20 a barrel as Chinese manufacturing gauge trailed all estimates and the US pledged to continue to stop Islamic radicals in Iraq.

In FX, the dollar rose to an 11-month high against the euro amid speculation from trades that the Fed would raise rates from early next year. The Aussie dollar fell the most in two weeks as Chinese HSBC PMI data came in lower than expected.

In focus today we have a raft of manufacturing PMI data from the Eurozone starting with Germany from 8:30am, followed by UK Retail Sales at 9:30am. This afternoon from the US we have Markit PMI at 14:45pm and US Existing Home Sales and Philly Fed data released at 15:00pm

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP MARKIT/JMMA Manufacturing PMI Better

- CH HSBC Manufacturing PMI Worse

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- WH Smith says on track to meet full-year market forecasts

- Illumina announces strategic partnerships with Astrazeneca, Janssen and Sanofi for oncology

- Interserve, Shanks jv win 950 mln stg Derby waste treatment contract

- Quindell says H1 pretax profit rises 292 pct

- London Mining posts H1 core loss

- Premier Oil profits rise on higher-than-expected production

- Kazakhmys posts fall in first half core profit