Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

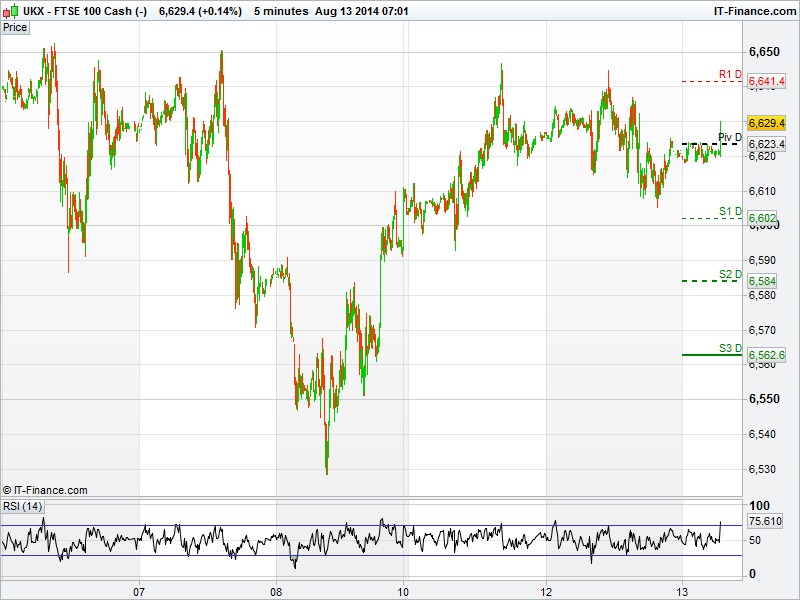

UK 100 called to open down 5pts at 6627, following a lacklustre session yesterday.

Traders were clearly undecided on 'where next' following last week's aggressive decline in equities and Monday's bounce.

There was a near even split in rising and falling stocks with 47 of the UK 100 stocks falling.

At the foot of the table was Hargreaves Lansdown (HL..L) down 2.87%. Swiss bank UBS prompted traders to dispose of the stock after issuing a 'Sell' note and a target price of 850p.

On a brighter note Prudential (PRU.L) attracted traders having reported a jump in first half profit thanks to operations in Asia and the United States. The company increased the interim dividend by 15%, in turn the shares closed higher by 2.20%.

At 10:30 today Bank of England Governor Mark Carney speaks and will deliver the latest quarterly inflation report. Traders will be looking for any indication of an interest rate rise, subsequently keep an eye on house builder stocks around this time.

US markets failed to excite for a second session, the Dow Jones fell just 9pts. The S&P 500 and NASDAQ registered equally uninspiring moves as indecision prevented buying or selling with any real conviction.

At 13:30 GMT monthly retail sales data will be released in the US and perhaps give the market a jump start.

In Asia economic data proved disappointing. Chinese factory output was recorded at 9% versus an expected figure of 9.2%. New local-currency loans of 385.2 billion Yuan were half of projections, while M2 money supply grew a less-than-anticipated 13.5 percent from a year earlier.

As a result the Shanghai Composite Index dropped 0.4 percent. Hong Kong’s benchmark Hang Seng Index fell 0.2 percent.

In Japan GDP data missed the estimated figure of 7% coming in at 6.8% showing the economy shrank the most since 2011.

In commodities, gold traded just below a three week low at $1309 as geopolitical tensions, and a stronger US dollar meant the safe haven was still in demand.

German investor confidence fell to the lowest since 2012, sending the euro to a nine-month low against the dollar.

WTI fell for a second day after an industry report showed crude and gasoline supplies expanded in the U.S., the world’s biggest oil user.

In focus today we have Euro-Zone Industrial Production released at 10:00am, and the BoE Inflation report at 10:30am.

This afternoon sees the US Retail Sales released at 13:30pm expected to show an increase for a sixth month.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP GDP Better

- CH Retail Sales Worse

- CH Industrial Production Worse

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- G4S first-half profit rises on emerging markets demand

- Daisy Group says receives takeover approach

- Michael Page sees 11 pct rise in H1 pretax profits

- Glencore copper production rises 13 percent in H1

- AstraZeneca reports positive results for gout combination therapy

- Car dealer Lookers sees 2014 ahead after H1 profits jump

- Car insurer Admiral names new CFO, posts 2 pct rise in profit

- Russia's Evraz signs $425 mln syndicated loan

- EnQuest earnings rise on higher oil production

- Land Securities sells Bristol Partnership stake to Axa