Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

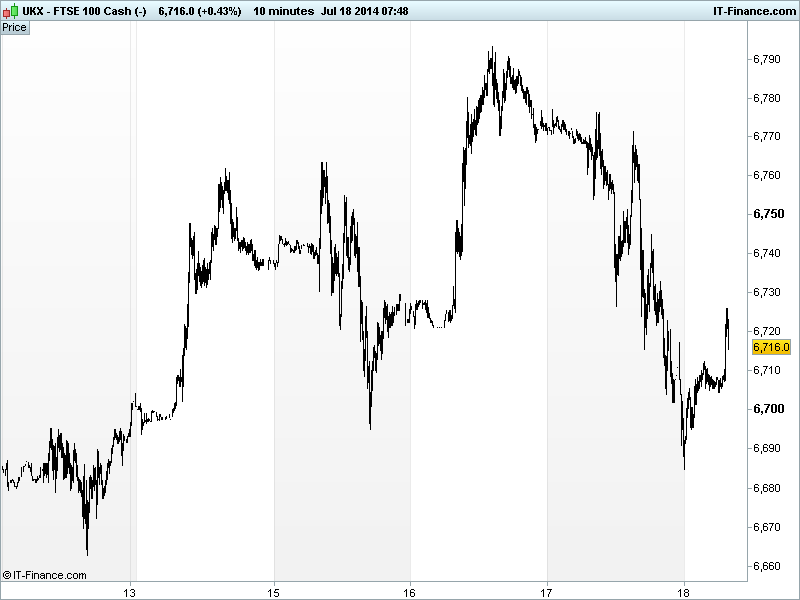

UK 100 called to open -20pts at 6715, having recovered from overnight lows of 6686 after US stocks fell sharply in response to the heightened geopolitical concerns following the air disaster in Eastern Ukraine, compounded by the Israeli ground offensive of Gaza and a White House lock-down due to a suspicious package.

Clam albeit a nervous one has dominated Asian trading with most stocks lower, following the European and US lead but, like the UK Index futures, stocks are off their worst levels. The latest is that Malaysian Airlines flight MH17 was shot down by Russian separatists who themselves blame the Ukrainian army.

Fed chatter included Bullard saying the Fed may need to reduce accommodative stance sooner than expected if the economy keeps improving at its current pace. He put the timing of the first US rate hike at end-Q115, based on jobs and inflation improvement. Results from Google and IBM beat expectations.

BoJ minutes for June state QE is having its intended effects and will continue for as long as necessary to hit the 2% inflation target. After the Chinese data of late, Premier Li reiterated economic growth of around 7.5% for 2014 and inflation around 3.5%, this while China’s MNI Business indicator improved but Chinese Property Prices fell for a second straight month adding to concerns about the nation’s debt burden.

While the market response to the unfortunate air incident was not as bad as many might have expected, with this being week-end and geopolitical risk such an unknown quantity, be prepared for some risk aversion on this, sadly, less-than-happy Friday.

In focus today will surely be the continued investigation into the Malaysian Airlines disaster, especially with major macro data being absent until US Uni of Michigan and US Leading index around 3pm, with readings almost unchanged from the prior month.

Before the US market opens we expect Q2 results from Honeywell International and General Electric, both good barometers for economic growth, while Bank of New York-Mellon has a tough act to follow from sector peers.

In commodities, Gold rallied back to $1320 as safehaven demand increased, but it has fallen back towards $1300 overnight as things calmed.

In Oil, WTI rose to almost $104/barrel on the combination of US stockpile drop and geopolitical unrest, while cousin Brent almost made it as high as $109/barrel.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN Property Prices Growth slowed again

- CN MNI Business Indicator Improved

- JP Nationwide Dept Store Sales Deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Spire Healthcare says London float priced at 210 pence/shr

- SIG buys France-based flat roofing products distributor

- UK watchdog plans full retail bank competition probe