Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

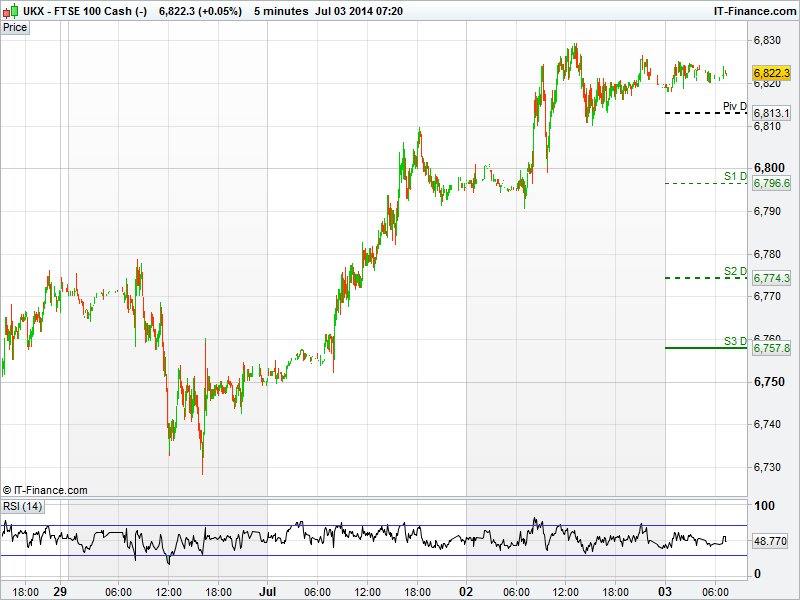

UK 100 called to open up 5pts at 6824, having advanced a modest 13pts yesterday.

European trading had been largely subdued as traders awaited ADP employment data from the US, looking for an insight into today's Non-Farm Payroll figures due at 13:30 GMT.

ADP data yesterday showed U.S. employment rose in June by the most since 2012, with more workers hired than economists projected, ensuring the UK Index recorded a positive days trading.

UK 100 equity price moves were shallow. The best performer, Standard Chartered (STAN.L) up 2.5% and the worst performer, Royal Mail Group (RMG.L) down 2.5%.

Buyers moved into Standard Chartered on rumours the company was looking to dispose of private equity investments. The raising of capital perhaps going someway to plugging the shortfall in profit announced just last week.

Commodity focussed stocks continued to rise. Rio Tinto (RIO.L), Antofagasta (ANTO.L) and Glencore (GLEN.L) up around 1% - the strong Chinese PMI data of earlier in the week still secreting positivity in the sector.

Royal Mail Group fell by 12.1p per share having gone ex-dividend to the tune of 13.3p per share.

Other notable underperformers include easyJet (EZJ.L) and International Consolidated Air (IAG.L) down 1.8% and 2.3% respectively. The companies still reeling from the damning Bank of America Merrill Lynch downgrade of on easyJet, issued on Monday.

U.S. stocks paused for breath having registered record highs the previous session. The Dow Jones added just 20pts, the S&P500 just 1.3pts. Traders are likely to scrutinise the employment data at 13:30 today before deciding to buy or sell.

Asian equity markets, having risen to a six year high on Tuesday, also came off the boil with shallow losses or gains registered across the region.

NON-FARM PAYROLLS AT 13:30 GMT - DO NOT MISS IT!

In focus today we have a raft of macro-data from Europe, kicking off with French PMI released at 8:50am, followed by German PMI at 8:55am and Euro-zone PMI at 9:00am. In the afternoon we have ECB rate decision expected to remain unchanged. However the focal point will be US Non-Farm Payrolls released at 13:30pm. Change in Non-Farms is expected to come in at 215k versus 217k previously with unemployment rate in line at 6.3%

In commodities, Gold retreated a touch to $1322, ahead of US Non-Farm Payroll figures released today at 13:30pm as traders remained undecided which direction to take. Having traded within a tight range for the last two-weeks this could help gold break this and either push towards $1380 or back down to $1300. WTI fell for the sixth day, down to $103.95, its longest losing streak since May 2012 amid speculation crude supplies will increase after Libyan rebels reached an agreement.

In FX, the US dollar rose from an eight-week low following better than expected ADP released yesterday, which showed optimism got todays data release. Meanwhile the Aussie dollar continued to slide following comments from Reserve Bank Governor Steven’s who said the currency was “overvalued” by most measures.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Poundland Q1 sales up 18 pct, confident outlook

- Accenture to provide application management services to Shell for engineering, production and process control

- Cineworld group 26 week box office revenues up 1.5 pct

- Ultra Electronics wins extra 64.4 mln stg contract with MOD

- Thorntons expects FY profit in line with market expectation of 7.1 mln stg

- Greene King says FY underlying retail sales rise

- Balfour says trading in mechanical and electrical engineering worsened

- Genel ramps up Iraqi Kurdistan oil output as exports increase

- Serco to write down value of contracts, could hit profits

- UK's SIG acquires Netherlands-based Inatherm BV