Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

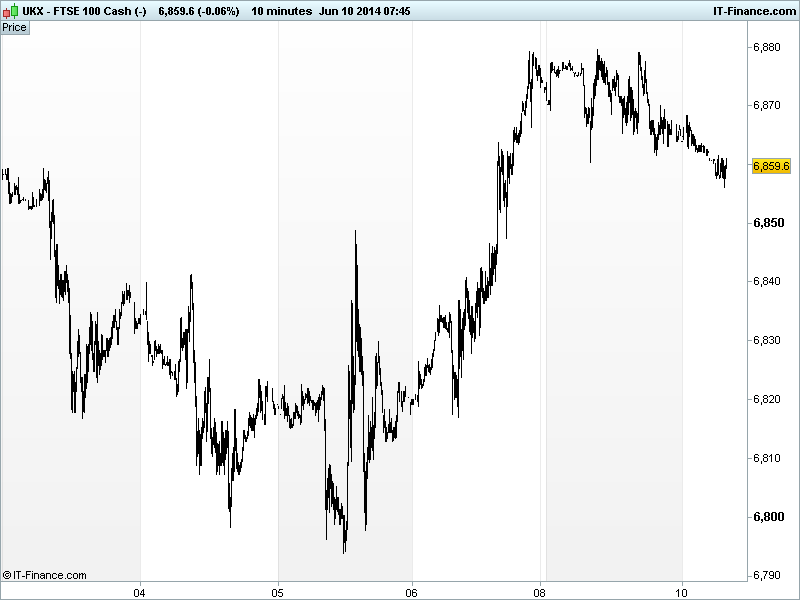

UK 100 called to open -10pts at 6860, back from its best levels of yesterday after it was unable to better recent highs of 6883 as equities inched higher on both sides of the Atlantic. The UK Index ’s 1-month 6773-6897 sideways range is unchanged with initial support/resistance just inside at 6795/6880.

US markets closed positive with the DJIA and S&P500 extending their winning streak helped by fresh M&A activity in the absence of macro data, hawkish Fed comments which maintained economic optimum as well as yesterday’s targeted China RRR cut. Even if gains were muted more record highs were notched up and the tech heavy Nasdaq was the US outperformer.

The Fed’ Bullard helped out slow markets and gave the USD a lift by saying that low unemployment may see him move his rate lift-off view forwards from end-Q1 2015, suggesting economic strength. Peer Rosengren countered this by saying he doesn’t expect a rate hike within a year of full employment and 2% inflation.

Overnight, Asian stocks mostly higher, taking the US lead, although with low volumes and volatility. The Nikkei is, however, down on a stronger JPY and mixed money supply and industry data, while China, Hong Kong and Australia are buoyed by contained Chinese Producer and Consumer Price Inflation as well as yesterday’s reserve requirement ratio (RRR) cut by China’s central bank (PBOC).

Other data overnight includes a slowdown in UK BRC Retail Sales, mixed Australian Business Confidence/Conditions and a stagnation in Australian Home Loans as Aussie banks turn more cautious on lower deposit buyers.

In focus today will be the April UK Industrial & Manufacturing Production data an acceleration of growth expected for industry and manufacturing pretty stable versus March. In the afternoon, consensus sees US Small Business Optimism higher while we get an update on the rolling 3-month UK NIESR GDP estimate. To close the day, US Wholesale Inventory & Sales growth are expected to have slowed in April.

In commodities, Gold continues to trade around the top if its recent $1250-1255 range with market optimism depressing safehaven demand and bargain hunters wary of increasing exposure to the yellow metal given the lack of inflation risk and the asset’s 3-month downtrend.

Oil prices got a boost from recent lows on expectations of stronger demand in the second half of the year. Ahead of Wednesday’s OPEC meeting, speculation is that the cartel would increase production to meet higher demand. The Venezuelan Oil Minister did however say he expected no change to the current 30m barrels/day output ceiling in place since 2011.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Sales Worse, slowed

- CN CPI Beat, accelerated

- CN PPI Beat, improved

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Kentz awarded $125 contract with Qatargas

- Ted Baker first-quarter revenue rises 17.9 pct

- President Energy ups exposure to Paraguay block

- Rolls-Royce wins 50 mln stg deck machinery contract

- Spirit Pub comparable sales rise

- Imperial Tobacco to float logistic unit Logista

- Oxford Instruments full-year profit rises marginally