Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

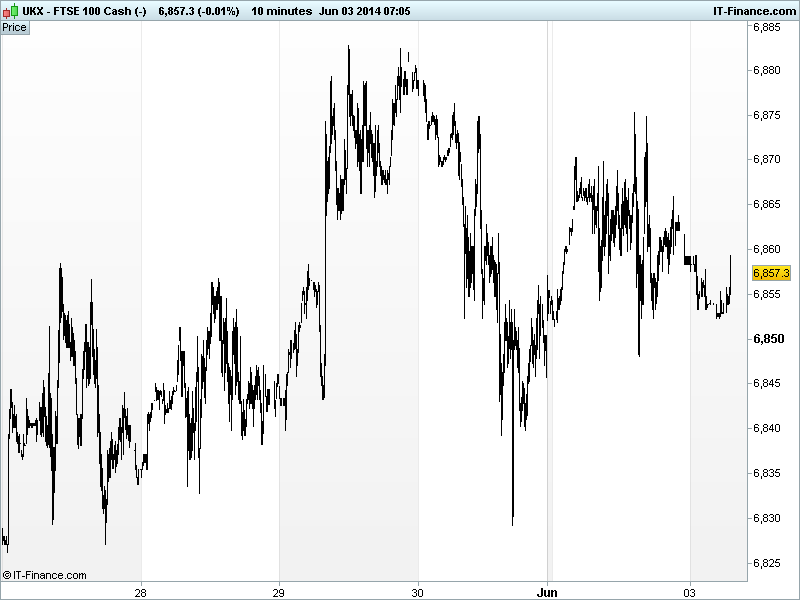

UK 100 called to open -15pts at 6855 after a mixed close in the US and a similar story in Asia despite the release of overall upbeat macro data from China with improvements in both the official Non-Manufacturing PMI and HSBC’s Manufacturing PMI for May, although the latter’s final read was below the flash and remains in contraction territory.

In the US, the S&P500 made a marginally higher new high, the DJIA gained a touch but the Nasdaq finished slightly bloodied. Choppy trading was the order of the day as ISM data was revised multiple times (Miss! No, beat! No, in-line!) although the indices erased losses by the close. Soft German CPI added to calls for the ECB to ease this week, seeing EUR/USD continue test 1.36 support.

Overnight, Asia sees the return of many markets after holidays. Japan’s Nikkei is back above 15,000 for the first time since early April helped by possible Government Pension Inv Fund reforms and a corporate tax cut. Hong Kong’s Hang Seng is also positive however; Australia’s ASX is in the red on a stronger AUD/USD after the RBA left interest rates unchanged (expected), reiterated the most prudent course is a period of stability.

As we get nearer to Thursday and the hoped-for action by the ECB (dare it disappoint markets?) we have lots of ECB speakers piping up, including Linde arguing that an extended period of low inflation isn’t good and the strength of the EUR is damaging, while Nowotny said there has been much discussion over whether a negative deposit rate would have any effect.

In focus this morning, we have Eurozone Unemployment seen unchanged at 11.8%, still off its 12.0% highs of 2013 but stagnant since December. However, this is sure to be overshadowed by CPI figures for the region seen falling back towards their recent lows, adding weight to the argument for stimulus from the ECB, especially after the German deflationary reads yesterday.

In the afternoon, after the data debacle of yesterday, ISM New York will be keenly watched, while US Factory Orders growth is expected to have slowed in April but Economic optimism gained some ground.

After a limited trading range yesterday, the UK 100 remains within its 6830-6885 channel awaiting a significant catalyst to take it one way of the other. Overall the long term uptrend is in-tact with the daily momentum indicator having kicked back up positive.

In commodities, Gold traded as low as $1241/oz near a 4-month low as worries about the US economy eased helping the USD higher and investors learn to live with the threat of geopolitical instability and continue to favour riskier equities. Safehaven demand just isn’t what it was.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN PMI Non-Manufacturing Improved

- CN HSBC PMI Manufacturing Miss, improved

- AU Retail Sales Miss, improved

- AU Interest Rates In-line, unchanged,

- UK House Prices Beat, accelerated

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Profits at UK water utility Pennon rise after tariff increases

- REA says owen wilson appointed CFO

- New Look FY underlying earnings up 5.8 pct

- Wolseley see revenue growth of 4 pct for next 6 months

- Foxtons CEO Michael Brown steps down for personal reasons

- AstraZeneca says antibiotic candidate given U.S. fast track status