Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

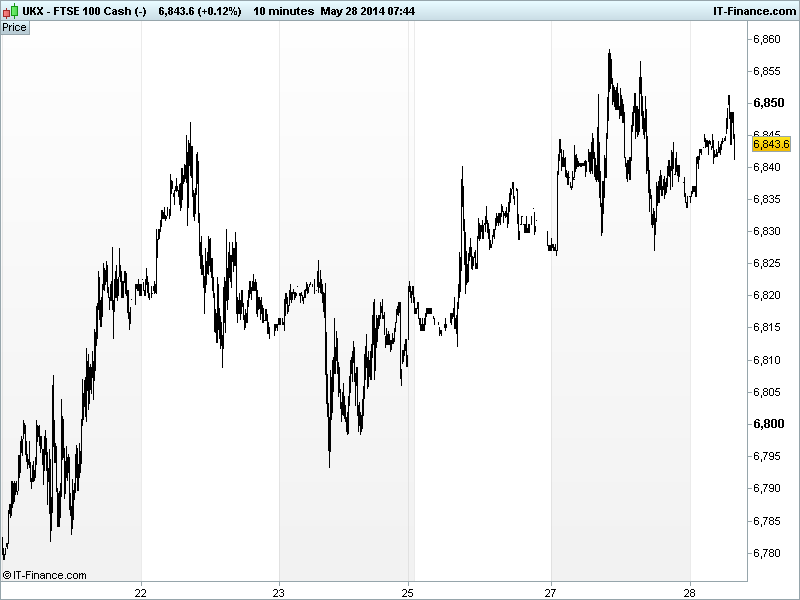

UK 100 called to open +5pts at 6845, having recovered from lows of 6830 but still struggling to overcome 6850 decisively. The uptrend from 20 May is still valid and the breakout of the falling channel from mid-month allows for possibility of a revisit of 6897, with belief in continued/new monetary stimulus the driver.

US equities closed higher after upbeat economic data (Durable Goods Orders, Housing, PMI Services, Consumer Confidence) reinforced optimism in the world’s #1 economy, with the S&P500 hitting a fresh record high before the close and the Nasdaq easily outperforming as investors return to smaller companies and tech which have borne the brunt of the recent sell-off.

Asian bourses also positive, helped by Chinese Industrial Profits growth holding steady in double digits in April, China Westpac-MNI Consumer Sentiment improving in May and Samsung announcing net sales in China surpassing those of South Korea for the first time in 2013, easing some of the recent concerns about a slowing of the world’s #2 economy.

The Fed’s Lockhart also helped sentiment by dovishly saying the central bank should not rush to raise rates before H2 2015 and that US GDP should rebound to 3% over the next few quarters. There were also reports in the Securities Journal that China may loosen monetary policy slightly in some areas, however, Xinhua reported that a fully-fledged RRR cut for banks is unlikely.

Note Marketwatch/WSJ reporting that China’s property slump is deepening despite government efforts to give home sales a lift, while Bloomberg suggests China’s biggest banks are set to report the highest bad debt ratios since 2009 indicating borrowers struggling amid an economic slowdown.

Other data overnight included Australia’s Westpac Leading Index which deteriorated in contrast to the rebound by Construction Work done. EU leaders will warn Russia today that, even following the Ukranian presidential election, they are still looking at possible further sanctions given the risk of energy supply disruption.

In focus today we have German Unemployment seen falling again in May, although not by as much as in April and the rate is expected to be flat. Eurozone Confidence (Econ/Ind/Cons/Servs/Bus) readings are seen pretty much unchanged in May, while UK CBI Sales are seen improving.

Gold trades at a 15-week low of $1260 after signs of improvement in the U.S. economy drover the USD higher versus peers and hopes that the Ukrainian presidential election result will reduce tensions with Russia dented demand for the safehaven metal. Even a revisit of Feb lows hasn’t enticed bargain hunters. Copper moved towards an 11-week high of $6932/ton on optimism regarding the US and China.

WTI and Brent steady around recent levels of $104/bl and $110/bl, respectively, ahead of US inventory data this afternoon and the latter supported by speculation that escalating violence in Ukraine may disrupt supplies to Europe from Russia.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Westpac Leading Index Deteriorated

- AU Construction Work Done Beat, rebound

- CN Industrial Profits Stable

- CN Westpac-MNI Consumer Sentiment Improved

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- FirstGroup says targets unchanged after losing Caledonian Sleeper contract

- Serco wins £800m stg Scottish rail deal

- Weir says Metso rejects revised proposal

- De La Rue posts 43% rise in full-year operating profit

- Telford Homes full-year pretax profit rises