Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

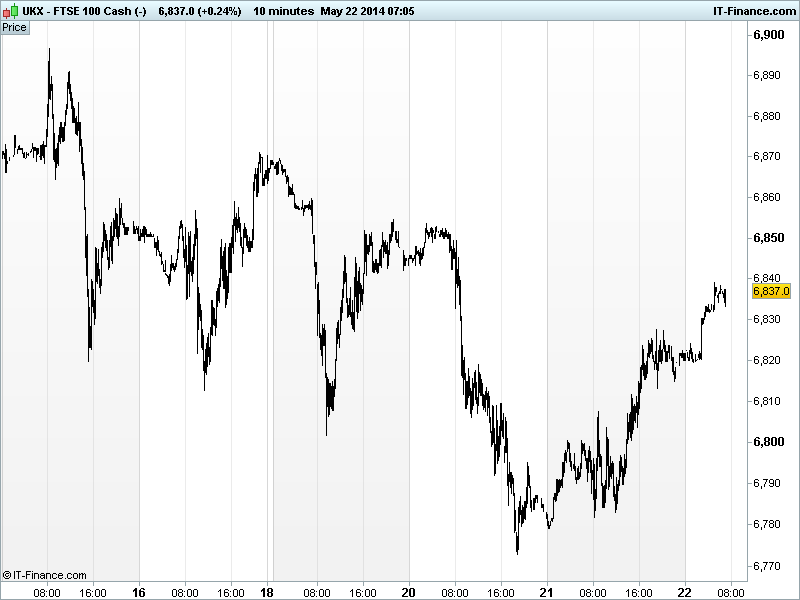

UK 100 called to open +20pts at 6840 after US bourses finished with respectable gains of near 1% after the USD weakened on dovish Fed FOMC minutes highlighting no inflation risks from fuelling job growth and while there was discussion about potential tools for monetary policy normalisation this did not mean it would take place any time soon.

Asian counterparts have followed the US lead overnight, and benefited further from HSBC China PMI Manufacturing (prelim) beating expectations, hitting a 5-month high and getting back up near the 50 level which distinguishes growth from contraction. Could this be a sign of stabilisation?

Japan’s PMI Manufacturing (prelim) also improved to near breakeven after dropping in March and with the Alibaba IPO train now running, note Chinese online retailer JD.com pricing above expectations yesterday ($19/share vs $16-18 expected) as investors nurse wounds form the recent tech sell-off.

The Fed’s Kocherlakota said the Fed was still undershooting on inflation and said it wouldn’t hit its 2.0% target until 2018, while, after Eurozone Consumer Confidence rose to a 6.5yr highs the Bundesbank head Weidmann said an ECB rate cut was not a given at the June meeting.

In focus today we have preliminary European PMI Manufacturing from France, Germany and the region which are seen delivering prints close to the final April readings. UK Q1 GDP is seen unchanged at 0.8% for the second estimate, confirming the strong recovery.

In the afternoon, US Jobless Claims are seen rising again after their drop below 300K, but continuing claims expected to remain near their recent lows. US PMI Manufacturing seen improving a notch, showing continued decent growth. US Existing Home Sales are expected to rebound in April while the Kansas Fed stays stable.

Gold still below $1300, trading as low as $1282 on the Fed’s muted inflation risk message from continued stimulus and assets in the SPDR Gold Trust dropping to their lowest since Dec 2008. The yellow metal is off its worst levels and trading above $1290 after the better Chinese data.

WTI trades near a 1-month high of $104.14, after Chinese PMI data registered the highest reading this year. The USD advanced against the JPY overnight after data signalled an improving outlook for Chinese manufacturing, while the JPY weakened against all 16 major peers as Asian equities extended gains.

The UK flagship index has continued its bounce from lows of 6770 as expected and broken above the trendline of falling highs from 15 May at 6820. This allows for the possibility that consolidation has been had in the form of a pause rather than a correction and that the uptrend resumes. Beware plenty of data to both help or hinder today. The proverbial spanner has habit of getting into the works at the wrong time.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Consumer Inflation expectations Higher

- JP PMI Manufacturing Improved

- CN HSBC PMI Manufacturing Beat, improved

- NZ Inflation expectations Card Spending Higher

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Property website Zoopla to float

- UK retailer Fat Face pulls planned London listing

- Electrocomponents FY headline pretax profit rises

- Royal Mail warns on competition as profits rise

- Unilever sells Ragu & Bertolli pasta sauces for $2.15 bln

- Amlin Q1 gross written premium up 5.1 pct

- Booker Group full-year profit rises

- QinetiQ FY profit lower, says on track for 2014

- SABMiller posts 1 pct earnings rise, sees tough trading enduring

- IG Group says full year revenue to miss expectations

- Carillion preferred bidder on 400 mln stg of MidEast contracts

- United Utilities says confident of delivering 2015 targets

- Mitchells & Butlers HY pretax profit flat

- Cycle sales help Halfords Group's profit edge up

- Dairy Crest's full-year profit jumps 31 pct on property sale