Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to open -5pts at 6845, after a positive finish for US stocks, led by small-caps and internet (NASDAQ outperforming) on one of the slowest trading days of the year given a lack of macro data to provide guidance and more focus on corporate deal-flow.

Asia following suit overnight with gains although Australia underperforming after RBA minutes reiterated current accommodative stance appropriate for some time and S&P warning that its AAA rating could be reviewed without big cuts to the budget in coming years, although clarified no immediate risk.

Japan’s Topix climbing from a 1-month low and Nikkei leading the way, rebounding after losses of almost 3% over the last 4 sessions. Note China’s Commerce Ministry saying the nation faces an arduous task to achieve 7.5% GDP growth this year.

With a lack of data yesterday, all eyes were on Fed speakers Williams and Fisher to spice things up with the former saying the Fed is moving towards normalising policy but reiterating his opinion of it being inappropriate to hike rates before H2 2015 and highlighting the risk of low inflation. Peer Fisher cautioned against inflationary risk and low market volatility due to low rates/QE.

Regarding Ukraine, the White House has said, like NATO, that it has seen on signs of Russian troops moving away from the border despite a statement from the Kremlin which markets had hoped signalled a possible easing of tensions before Ukrainian presidential elections in six days.

Back to the ECB stimulus choices and Nowotny said that banks in countries that introduced negative interest rates accepted these, but in a European context such a step requires discussion.

Overnight data comprised Aussie Conf Board Leading Index which stagnated in March not helping with the ASX’s underperformance this morning. Japan’s business sentiment indices were mixed but beat consensus, however, German Producer Prices show a return to deflation in April versus a hoped for flat performance.

In focus today, amid another light macro calendar, will be UK inflation data as the dominant prints and coming just after dovish rhetoric from BoE Governor Carney last week after the latest quarterly inflation report from the central banks.

UK CPI is seen edging up over the month (0.3% vs 0.2%) and year (1.7% v 1.6%), with the key annual rate coming off its recent lows although still below target and reinforcing the expectation that rates will not rise before next year’s general election. Core seen edging up to 1.8%. Watch the reaction of the GBP vs peers should CPI beat or miss.

UK Producer Prices are expected to show and easing of input price pressure but stability in output prices, while ONS UK house Prices are seen accelerating further towards the double-digit annual gains.

On the corporate activity front, Zoopla is expected to announce its intentions for a £1bn London IPO alongside DMGT results on Thursday, while a refloat of Game Group could be soon on the cards. Results out from Vodafone and Marks & Spencer this morning.

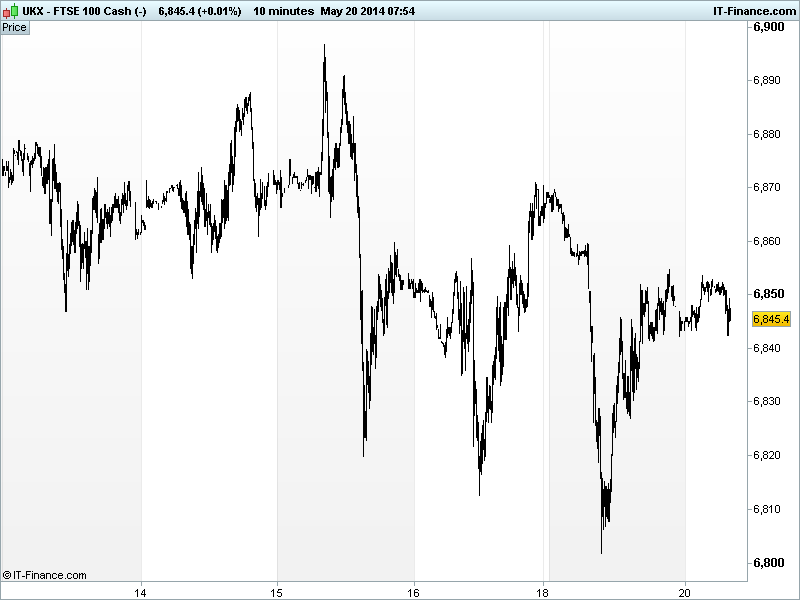

The UK flagship index remains under pressure, finding resistance overnight around the 6850 level which reinforces the trend of falling highs from recent peak of 6897. This in fact gives us a falling channel which as highlight recently could be a pause for breath or the start of a correction after the recent 6500-6900 rally.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Conf Board Leading Index Flat, deteriorated

- JP All Ind Activity Index Miss, improved

- JP Business Sentiment Indices Beat, mixed

- JP N’wide Dept Store Sales Deteriorated

- DE Producer Price Inflation Miss, deteriorated

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Vodafone results in line, 2015 earnings to fall

- M&S profit falls for third straight year

- Topps Tiles H1 sales rise 11.7 pct

- Buy-to-let lender Paragon's first-half profit rises 21 pct

- BTG full-year pretax profit rises 38 pct

- Victrex first-half pretax profit rises

- Pumps maker Spirax-Sarco's organic sales up 4 pct

- Homeserve says confident of further progress for year ahead

- Big Yellow profit buoyed by higher self-storage space demand

- RSA Insurance sells stake in Noraxis for C$500 million

- Afren first-quarter revenue falls