Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

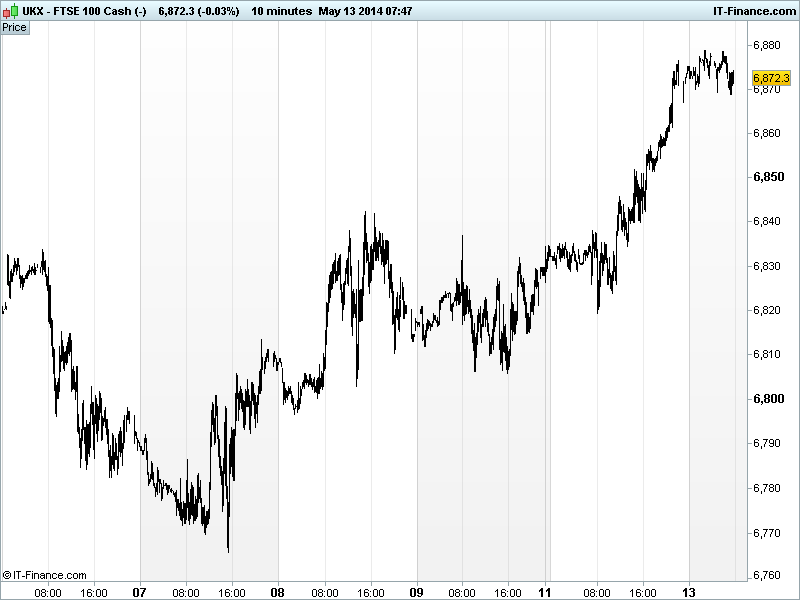

UK 100 called to open +25pts at 6875, teasingly close to Feb highs of 6886 and still headed towards turn-of-the-millennium highs of 6950 as appetite for risk remains strong and peer indices like the DJIA and S&P record fresh record highs while the recently shunned small cap and internet names rebound.

This despite the Russia/Ukraine situation remaining tense (Donetsk declared itself a sovereign state, asking for Russian adoption) with RU accusing UKR of criminal lack of willing for dialogue with Eastern regions while the major of pro-Russian Slavyansk has called for Russian troop presence to provide future stability.

Overnight, stocks in Asia took the lead from US counterparts with Japan’s Nikkei outperforming thanks to a weaker JPY and Australia’s ASX gaining ahead of the budget (later) and despite weak home and house price data. Note the outperformance of dual-listed Australian mining names in London yesterday.

Hong Kong’s HangSeng is the underperformer thanks to Chinese macro datadisappointing with Retail Sales, Industrial Production and Fixed Asset Investment all undershooting consensus. Note the PBOC’s Chen saying Q1 growth within target range of 7.5% and evidence from Q2 needed in order to make next policy move. Market reaction, with equities bid, suggest stimulus hopes still strong.

In focus today, we have May ZEW Surveys for Germany and the Eurozone with a mixed batch expected. US Retail Sales are expected to have cooled in April, although ex-Autos could be more stable, US Import Price growth seen slowing in April and US Business inventories showing stable growth in March.

The UK flagship index has broken above the 6840 level as traders eye 2014 highs of 6886 and indeed all-time intraday highs of 6950 from the turn-of-the-millennium. Still in an uptrend from mid-April lows of 6500, we expect 6840 to revert to support, helping with the move closer to less-charted territory with a lack of pre-vested interest in the levels being traded. Note overnight resistance at 6880.

In commodities, Gold benefited from geopolitical worries from Ukraine sending the yellow metal back up above $1300/oz, however, this was only brief with the safehaven back trading close to the $1290/oz level of around which it had been oscillating since the middle of last week.

US Light Crude still appears to have resistance at $101, but sits in a narrow $100-101 trading range and still in a May uptrend.A US government report due tomorrow show stockpiles dropping for the 14th time in 15 weeks. Brent Crude has been unable to get above $109, but also shows an uptrend from mid-last week supported by geopolitical risk.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Sales Beat, improved

- JP Money Supply In-line, slowed

- AU Home Loans Miss, deteriorated

- AU House Prices Mixed

- CN Fixed Asset Investment Miss, slowed

- CN Retail Sales Miss, slowed

- CN Industrial Production Miss, slowed

- DE Wholesale Price Index Improved

See Live Macro Calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Melrose says orders rise 3 pct

- AstraZeneca to start Phase III trial for diabetes candidate

- easyJet H1 beats forecasts, says on track for growth

- Essar Energy independent committee suggests shareholders accept offer

- TUI Travel says confident on full-year profit target

- Insurer Brit sees written premiums rise 6.5 percent in Q1

- Interserve says trading in line with expectations for 2014

- Sportech trading meets expectations despite harsh U.S winter