Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

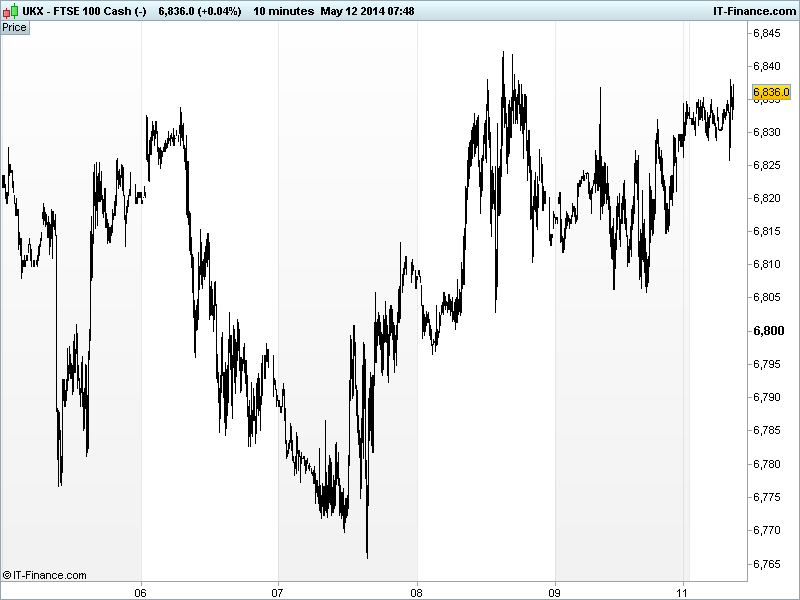

UK 100 called to open +15pts at 6835, after a modestly higher close and rebound by US stocks on Friday helped by momentum stocks reacting positively to macro USWholesale Trade data beating expectations and some positive headlines on the Ukrainian conflict (US-Russia talks, referendum postponed).

While markets wait for ECB President Draghi to pull the trigger on further stimulus (rate cut, QE) , after suggesting last week that the central bank will move next month, risk appetite also helped by the Fed’s Fisher talking dovishly of accommodation so long as inflation sub-target and he expects USQ2 GDP growth to recover sharply. Fed peer Lockhart expects a rate rise in H2 2015 and gradual rate normalisation thereafter.

In Ukraine Over the weekend, Donetsk voted almost 90% in favour of independence and we await results from Luhansk. Pro-Russian groups in the East have increased tensions by hailing a large majority in favour of secession in a referendum condemned illegitimate by a host of countries including the UK. France and Germany have said they would draw the appropriate consequences if the 25 May Ukraine Presidential election does not go ahead as planned.

While an IMF official late Friday warned that the fund maylower their China2014 GDP estimate, ratings agency Moody’s said China may be the world’sbiggest economy by year-end.

Overnight, Asian stocks mixed with Japan and Australia in the red with the former on ‘earnings watch’ and held back by weak data while and latter is hindered by Miners with as spot iron ore prices fell to a 20-month low. On the flip-side, Hong Kong very much positive thanks to mainland China stocks surged on speculation of market reforms (relax limits on foreign investment, expand quotas on capital flows) which could support equities as the country adapts to the new normal slower growth.

In focus today, we have a quiet start to the week with EU Finance Ministers meeting at 8.30, the UK Lloyds Employment Confidence at 9.30 and the US Monthly Budget statement at 19.00.

Note casual retailer FatFace pricing its IPO at 210p-265p/share, implying a market cap of £305-385m and raising it £96-103m. The company expects conditional trading to start on May 23 - the same day as over 50's insurer/holiday group Saga, which has attracted a significant amount of interest.

The UK flagship index remains held back by the 6840 level although we note that the trading range has narrowed and remained close, allowing for the possibility of a breakout as we move into the new trading week. Once above, the coast is clear to 2014 highs of 6886. Note support at 6806 from Friday’s lows, then rising lows at 6780.

In commodities, Gold holding around $1290/oz as the safehaven metal waits for confirmation of which way the Ukraine situation, the global economy and the future of monetary policy is headed. For better or for worse? For more or for less?

US Light Crude is little changed at $100 while Brent Crude is back around $108 having reached $109 on Friday. Global growth and the Ukraine/Russian geopolitics still ruling sentiment.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Current Account Balance Miss, Deteriorated

- JP Bank Lending Stable

- AU Business Confidence Mixed

- AU Credit Card use Stable

- JP Bankruptcies Deteriorated

- JP Sentiment Surveys Mixed

See LiveMacrocalendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Hit by South Africa strike, platinum miner Lonmin earnings plunge

- Diploma posts H1 pretax profit of 24.2 mln stg

- Anite says still investigating potential sale of travel unit

- Inmarsat to provide free tracking service after missing MH370