Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

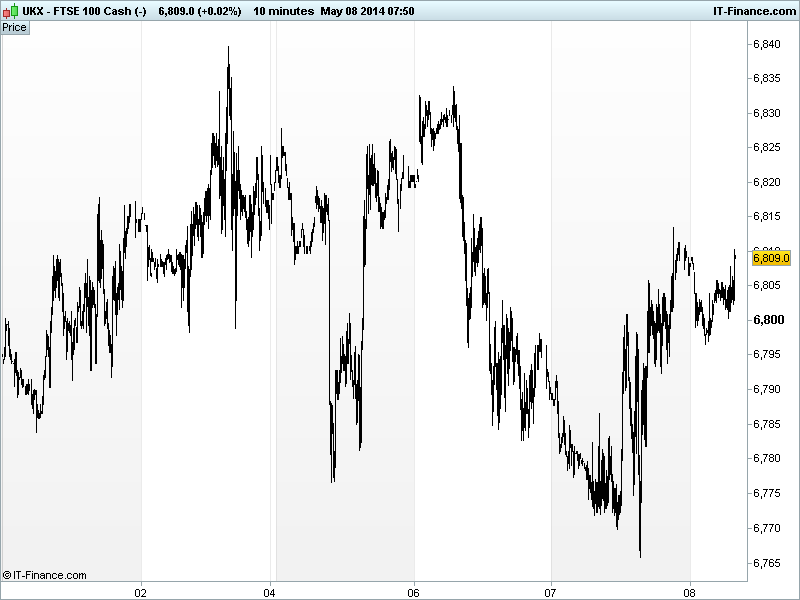

UK 100 called to open +15pts at 6810, supported by better than expected Chinese trade data for April offsetting recent poor China PMI readings earlier in the week, and continued hope of calming between Russia and the Ukraine (Putin calls referendums to be postponed and troops pulled back; no evidence yet; situation still very volatile) which had brought markets back from their lows of yesterday afternoon.

US stocks closed mixed-to-positive (Nasdaq down, tech names still troubled) after Fed Chair Yellen’s dovish testimony to the Senate (economy needs continued help). She suggested rates would stay low for some time after QE3 ends, saw downside risk to housing, sees much slack in labour market but equity market valuations in-line with historical averages. Geopolitical risks were also mentioned.

China’s trade report showed unexpected gains for both imports and exports and a bigger than expected surplus offering the possibility that momentum could grow in the coming months/quarters, offsetting some of the dogged fears that the for the world’s #2 economy’s annual GDP targets will be missed.

Other overnight data included the UK RICS House price balance falling from its recent peak, although prices continue to rise with sales volumes and loan-to-values increasing and inflation more widespread. The Aussie jobs data was much better with more jobs added and the unemployment rate holding.

In Asia, equities started off positive after Yellen’s testimony and the possible de-escalation in Ukraine supported risk appetite, and were further buoyed by the Chinese trade data and Aussie Employment report data released overnight.

Now back above the 6800 level, the question is whether the highs of 6840 can be revisited or whether this is another weak recovery attempt amid a correction. As we have noted recently, after a 5% rally from 6500, a fall back to rising support around 6720/6740 could be justified.

In focus today will be the policy decisions from the BoE and ECB with no surprises expected from either. The BoE is unlikely to move in spite of concerns over a rampant property market. The latter looks to have teed us up for more inaction thanks to improving business surveys despite a strong Euro and evidence of deflation requiring some form of unconventional stimulus or even lower rates. ECB President Draghi’s press conference will garner most attention with his words having spoken louder than the banks actions for almost 2 years now.

In commodities, Gold has fallen back to $1290/oz on news that Russian President Putin could be ready to discuss steps to defuse Ukraine tensions. This saw the metal drop through $1300/oz from its 3-week highs of $1315/oz highs as safehaven seeking cooled. This also despite Fed Chair Yellen’s dovish testimony (more help needed) but optimism on US recovery allowing for continued withdrawal of QE3.

US Light Crude holding above $100/bl and got as high as $101/bl after a surprise drop in US inventories. Brent Crude holding around its $108/bl highs of yesterday despite the possibility of a diffusing of Ukraine/Russian geopolitics reducing the prospect of supply disruptions.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK RICS House Price Balance Miss, deteriorated

- AU Jobs Better

- CN Trade Data Better, rebound

- DE Industrial Production Miss, contraction

- UK Q1 Results: BT, BDEV, MRW, PRU. RSA, STAN, RRS, SGE

- EZ Q1 results: Deutsche Telekom, Repsol

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- StanChart sees Q1 profit decline on Asian currency weakness

- Standard Chartered says group income in Q1 2014 down by low single digit percentage

- UK grocer Morrisons sales continue to slide

- Demand for broadband lifts BT to strong full-year results

- IMI says trading in first four months of 2014 in line with expectations

- Derwent London sees up to 7 pct portfolio rental growth in 2014

- Barclays to axe 19,000 jobs under revival plan

- Poundland sees year profit in line with forecasts

- Centrica agrees further ties with Qatar, lowers outlook

- Beazley Q1 gross written premium drops to $516 mln

- Barratt Developments says total forward sales up 47 pct

- Morgan Sindall says order book rises 9 pct by the end of Q1

- Glencore appoints ex-BP boss Tony Hayward as permanent chairman

- RSA net written premiums down in Q1 as shakeup continues

- Cineworld says box office revenue rises 8.6 pct in 18 week period to May 1

- Randgold Resources says Q1 mining profit rises 14 pct

- Sage Group says Guy Berruyer to retire as chief executive

- Centrica sells stake in Canadian gas business to Qatar

- Supergroup sees full-year profit towards lower end of consensus