Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

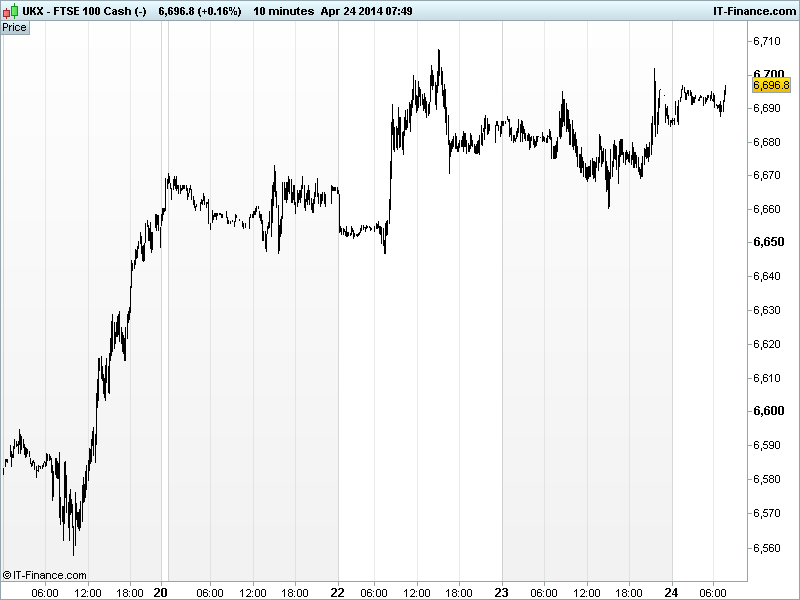

UK 100 called to open +20pts at 6695, recovering from yesterday’s test of 6670 support and after a brief re-test of 6700 thanks to US futures getting a boost after hours from Apple and Facebook earnings reports - investors welcoming a boost to the latter’s payout programme (stock buyback +30%, dividend +8%).

US stocks recovered a little from their lows but still closer a shade lower due to disappointing macro data overshadowing some good earnings reports from the likes of P&G, Boeing and Dow Chemical, with New Home Sales data for March falling to an 8-month low and suggesting the US housing recovery could be losing momentum and April US PMI Manufacturing slipping in contrast to an expected nudge higher.

In Asia, stock again miked with Japan’s Nikkei in the red on expectations that earnings season will disappoint and highlight a poor outlook following the hike in sales tax. China dented by limited PBOC intervention. Hong Kong’s Hang Seng and Australia’s ASX just in positive territory.

In geopolitics, tensions remain high in the Ukraine with Russia confirming it is carrying out military exercises in the region that borders Ukraine and expressing surprise at US and Ukrainian interpretation of the agreement made in Geneva.

Before ECB President Draghi speaks this morning, note colleagues Hansson and Nowotny vocal yesterday saying ECB ready to act if inflation misses target but must not take action before June as no immediate need to act. This followed a strengthening of EUR vs USD after Eurozone PMI Manufacturing and Services data yesterday.

In focus today we have German IFO Surveys at 9am which are expected to hold around the same levels as last month. ECB President Draghi speaks at 10am (watch the EUR).

Watch out for more US results today from the likes of General Motors, Verizon Communications, Caterpillar and UPS. The first two can provide colour on growth in the world’s largest economy (US) while the latter can do the same for raw materials demand (China) and global business levels.

In the afternoon, US Durable Goods at 1.30pm are forecast to show more solid growth in March while the Kansas City Fed manufacturing Index is seen slipping at 4pm. After US markets close, results are published by Amazon Starbucks and Microsoft with all seen showing YoY drops in revenues and earnings. The question is will they beat guidance/consensus?

The UK 100 looks like it wants to keep testing 6700 and a breakout there would open up the possibility of a move to 6800. Should it remain resistance we see support at 6660 lows of yesterday and then 6650.

Gold remains around the $1285/oz level, but continues its bounce from a 10-week low of $1276/oz with the concerns about Russia/Ukraine and weaker US macro data maintaining interest.

Oil: Brent found support again at $108.5/bl as Ukraine tensions persist, but yesterday’s highs may prove resistance again at $109.5/bl. US Light Crude/WTI trading around $101.7 (mid-range of yesterday) after US inventories rose again, reaching an 83-year high, and following the sharp drop from $103-104/bl the prior day.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN Conf Board Leading Econ Index Improved

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- African Barrick Gold core earnings, revenue fall on lower prices

- Tertiary Minerals says recent share price movement "unjustified"

- Premier Foods posts 6.2 pct fall in first-quarter sales

- Travis Perkins Q1 underlying sales up 12.7 pct

- Spirit Pub says interim dividend increased by 6 pct to 0.72 pence

- Senior Q1 adjusted pretax profit in line with board's expectations

- Berendsen says revenue at core growth business rises 4 pct

- Russia's Polyus Gold Q1 sales down 15 pct y-on-y

- Elementis sees FY earnings in line with market expectations

- Lloyds appoints chairman of Scottish Widows

- Chemring Group to dispose off European munition unit for 167.8 mln euros

- Unilever first quarter sales rise despite later Easter

- Cobham sees return to revenue growth in 2015

- Croda pretax profit rises marginally

- AstraZeneca flags cancer advances, silent on Pfizer bid talk

- Anglo copper, iron output rise as strike hits platinum

- Centamin says new Egypt law could see claim against it dismissed