Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

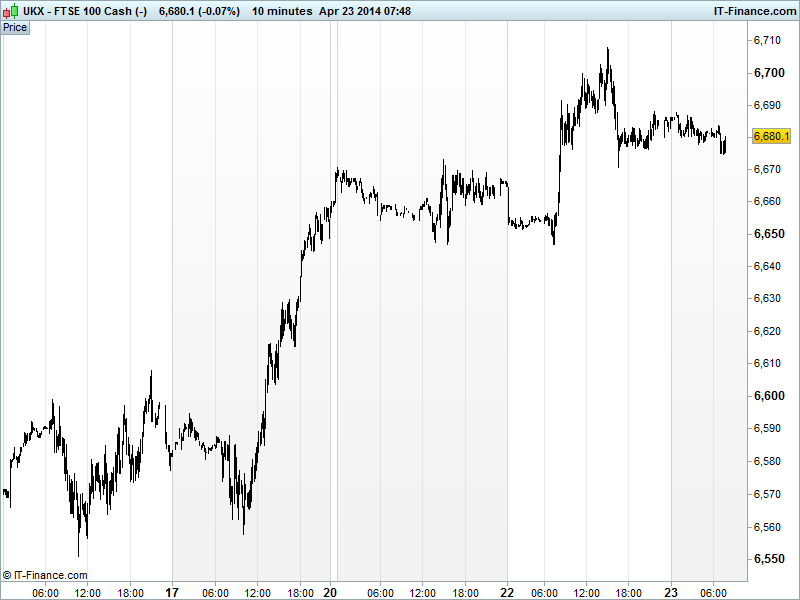

UK 100 called to open -10pts at 6675, holding just above 6670 resistance-turned-support from yesterday, after a brief test of next hurdle 6700 following the US market open as investors welcomed upbeat corporate earnings reports and economic data (Housing and Richmond Fed Manufacturing) which suggested an improved US economic outlook.

US equities closed higher, with Tech benefiting further and the Nasdaq outperforming, and the S&P’s winning streak to the longest since September helped by M&A activity in the healthcare sector. Yum! pleased traders with news of improved sales in China and plans for expansion in the region. AT&T reported rising revenues on better wireless subscriber additions.

Overnight index resilience comes in spite of HSBC China Manufacturing PMI confirming another month of contraction in the world’s #2 economy, however, investors look to be focused on the slight improvement in April and remain content with the fact that any slowing is not getting any worse than already feared.

In Asia overnight, equities mixed with Japan’s Nikkei higher on comments from BoJ Governor Kuroda that the inflation forecast would be revised higher next week and the JPY weakening slightly.

Hong Kong’s Hang Seng lower on the slowing Chinese data, however, Australia’s ASX is higher with weaker-than-expected inflation data denting chances of a rate rise and thus hindering the AUD, overshadowing the weak manufacturing print from biggest export partner China.

In focus today we have preliminary Eurozone PMI Manufacturing and Services with France, Germany and the region as a whole expected to show slight improvements and remaining comfortably above the 50 growth/contraction level. Thereafter, UK CBI Trends are seen showing rises for orders and optimism, but a small pull back in prices.

In the afternoon, US PMI Manufacturing is expected to tick higher as are US New Home Sales, in-line with yesterday’s Existing Home Sales print which helped boost markets to their highs on perceived improved consumer confidence. Q1 results are also scheduled from the likes of P&G, Boeing, Dow Chemical, Delta Airlines, Texas Instruments, Apple and Facebook (the latter two after the US close).

The UK 100 tested 6700 as expected, and we note overnight support at prior resistance 6670. Will this prove supportive enough for another push higher and a more meaningful breakout? Watch out for data and results as potential drivers. Thereafter, our next index hurdle appears around early March highs 6830.

In commodities; Gold still under a lot of pressure. Having left $1300 behind last week, and failed at $1290 on Monday, despite a rebound from $1280 April lows overnight it would now appear to be struggling at prior support $1285 suggesting waning demand for the safehaven. Signs of improved US outlook trumping concerns about slowing and China and tinderbox Ukraine.

In Oil the price of Brent has come under a bit of pressure after hitting highs of $110 despite Ukraine worries with a breach of $109/bl yesterday. Support found at $108.5/bl, but the rebound found resistance at $109.5/bl overnight. US Light Crude/WTI has traded down to and bounced from rising support around $104/bl after China manufacturing data, but resistance holds at last week’s highs $105/bl.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN HSBC PMI Manufacturing In-line but improved

- AU CPI Worse, slowed

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Sports Direct posts 11.5 pct rise in Q4 gross profit

- Petra Diamonds third-quarter revenue jumps 55 pct

- Fenner first-half revenue falls 8 pct

- Fenner profit slumps on weak demand for conveyor belts

- Spirent Communications Q1 revenue up 16 pct

- Hammerson says economic recovery driving tenant demand

- Kentz awarded $125 mln contract in Kuwait by Fluor

- AB Foods profit growth held back by sugar

- Chip designer ARM sees pick up in demand in second half

- Rolls-Royce wins $39 mln engine contract to support US V-22 aircraft

- Moneysupermarket.com confident on meeting expectations

- ABF says Primark to open stores in U.S.

- Drax sues UK government over u-turn on biomass conversion support

- Creston sees results in line with forecasts

- Flybe Group announces new routes exit London