Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

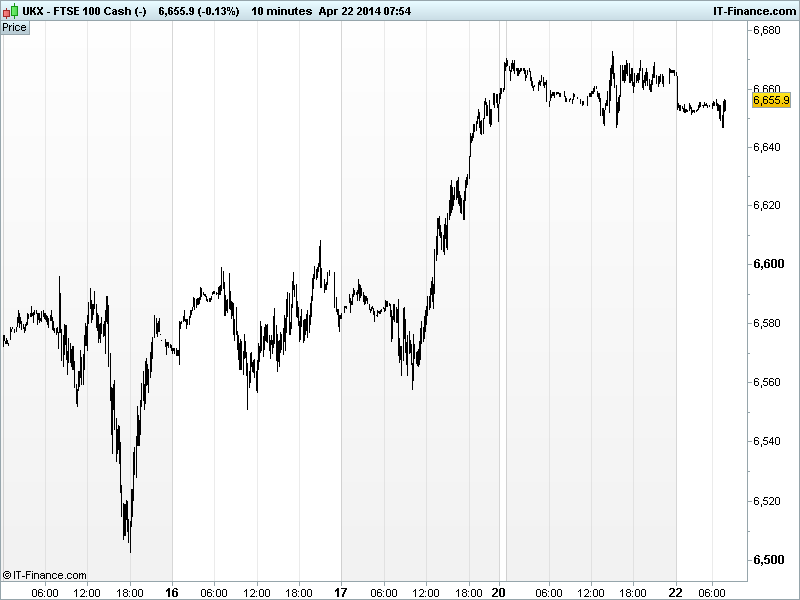

UK 100 called to open -10pts at 6650, trading back from highs of 6670 of late Friday after a breakout above 6600 fuelled by US equities pushing higher with investors taking a positive view on US Q1 corporate earnings, macro-economic data (bad weather behind us), US monetary policy outlook and news from Geneva on Ukraine increasing appetite for risk (technology rebounded) and dampened that for safehavens such as Gold.

Overnight, US extended last week’s gains (longest winning streak for S&P500 since Oct) during Europe’s Easter absence and amid a light day for trading volumes, macro-data, news and corporate results. While the US Conference Board Leading Indicator accelerated more quickly in March, the Chicago Fed Nat. Activity Index pulled back as expected.

In Asia, however equities are mixed on a lack of volume and newsflow with Japan’s Nikkei the underperformer after disappointing trade figures highlighted a bigger than expected widening of the trade deficit while in China the average new home price in 70 major cities rose 7.7% YoY in March, cooling from the 8.7% in Feb, highlighting the catch-22 for authorities in terms of avoiding bubbles but stimulus maintaining growth.

Overnight, note the agreement to ease tensions in Ukraine showing signs of crumbling as the US and Russia trade blame during meetings keeping things just as tense as they have been for weeks.

In focus today, we have a quiet start data-wise to this the shortened week with nothing of note until late morning when Bank of New York Mellon reports Q1 results. Before the US market opens we also have the likes of McDonalds, Xerox, Lockheed Martin, Travelers, Comcast and United Technologies.

In the afternoon, listen out for updates on the US House Price Index for Feb which is seen holding around Jan’s 0.5% growth. The Richmond Fed Manufacturing Index is expected to rebound into positive territory in April (2 vs -7), while US Existing Home sales are forecast to give up a little ground in March. Lastly, Eurozone Consumer Confidence is seen confirming an improvement albeit still negative.

The UK 100 a broke out above 6600 on Friday helped and got as high as 6673 where it encountered falling resistance from 4 Apr. The opening call is seen testing weekend support of 6645. While support moves up to 6600 thanks to the breakout, the next big hurdle is 6700.

In commodities; Gold remains under pressure thanks to signs of an improving US economy and despite geopolitical fears, falling for a sixth day to the lowest in 2 weeks $1280 and now well below the key $1300/oz level.

In Oil the price of Brent remains around 6-week highs of $110/bl as simmering tensions in Ukraine continue to be watched carefully by traders concerned by disruption to supply from harsher Russian sanctions. US Light Crude also has support around $104/bl.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Conference Board Leading index Improved

- JP Leading Index Improved

- JP Coincident Index Deteriorated

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Colt Group announces restructuring; to withdraw from 85 pct of carrier voice unit

- Dragon Oil average oil production rises in first quarter

- Mwana Africa says full-year gold production falls

- Pfizer mulls $100 bln bid for AstraZeneca