Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

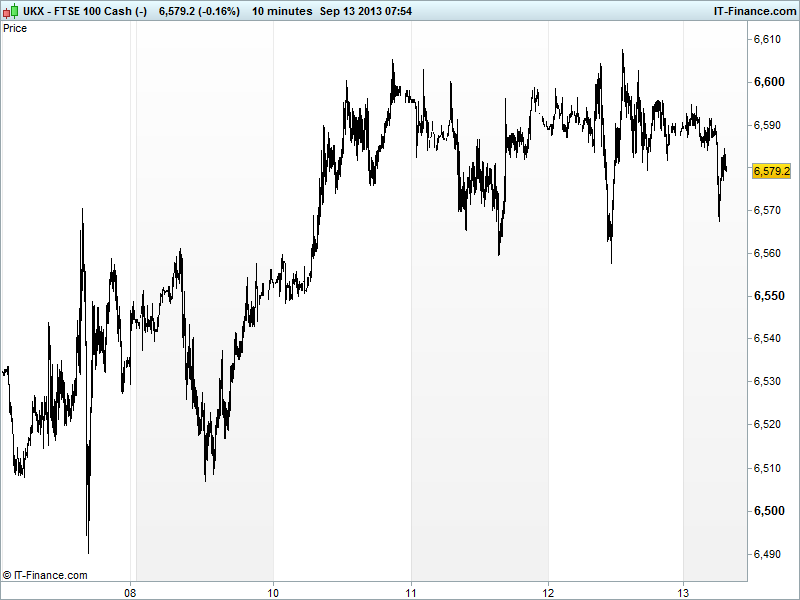

UK 100 called to open -5pts this morning at 6580, trading sideways in its 3-day 6560-6600 range, although we note the absence of an overnight test of the 6600 level as we move into the weekend suggesting some risk being taken off the table ahead of the Fed decision next week and reports from Asia of the more hawkish Larry Summers being chosen as the next Fed Chairman over current vice chairwoman and more accommodative Janet Yellen.

Asia equities in the red with sentiment weighed down by the prospects of tapering replacing worries over Syria (although the situation is still uncertain), with failure to benefit from Japan raising its economic assessment and capex outlook, and accelerating Industrial production data, with focus on the downgrade to consumer spending assessment (key part of recent GDP strength and likely to be hit by sales tax) and exports.

In the US markets closed in the red, but only marginally, with no chance to benefit from Twitter’s late announcement of following Facebook and filing for an IPO. Investors will be hoping for a cleaner debut for this one, with no Nasdaq glitches. Expectations of more aggressive Fed tapering emerged after very low jobless claims, but the impact of some states not filing due to computer problems (that’s it blame IT). USD stronger as a result.

In Europe, France’s President Hollande has announced a 34 project plan to reverse the country’s industrial decline while ECB president said the bank was not out of options and the recovery still very green and inflation likely to be on the low side.

In focus today we have UK Construction Output seen improving markedly in July. US Retail Sales seen improving at the headline, flat ex-Food and Energy and slower ex-Autos. To close the week, Uni of Michigan Consumer confidence seen flat and US Business Inventories ticking up.

With 6600 remaining a hurdle the UK 100 has traded sideways and broken out of the rising wedge from Sept 4 we discussed yesterday. Potential for sideways to persist ahead of Fed update next week (and possibility of Summers beating Yellen) and uncertainty surrounding Middle East (Syria, Egypt extends state of emergency). Still support at 6560, but failure to break 6600 and even test it overnight opens up the possibility of a correction back to 6500.

In FX, USD index ticked back up above 81.5 after exceptionally low (2006 level) jobless claims and increased chances of tapering next week and talk of Summers beating Yellen to the Fed chair. GBP/USD cooled at recent highs of 1.584 but support just below at 1.578 61.8% Fibonacci retrace of 2013 Jan-Mar decline. EUR/USD turned down from 1.33 highs on USD strength and awful Eurozone industrial Production yesterday.

Gold maintains its breakdown from the rising channel from end-June, driven by stronger USD, prospect of Fed tapering and less safehaven seeking on account of cooler (albeit still uncertain situation) in Middle East. The break below $1350 has seen a fall to near $1300 overnight. Watch for $1350 to revert to resistance.

Oil rebound persists but more with Brent than Crude, with the latter pulling back and the former a little jumpy. Brent Crude still near $113 and US Light down 50c at $108.5. What’s up in the Middle East and tapering still the drivers.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Industrial Production Accelerated

- JP Capacity Use Increases

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Vodafone victorious in €7.7bn Kabel bid

- JD Wetherspoon posts 6.3% rise in profit

- Germany's M+W Group will not make offer for Kentz

- Glencore says Zanaga project advances on staged basis